Berkshire Hathaway 2012 Annual Report Download - page 57

Download and view the complete annual report

Please find page 57 of the 2012 Berkshire Hathaway annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

|

|

Notes to Consolidated Financial Statements (Continued)

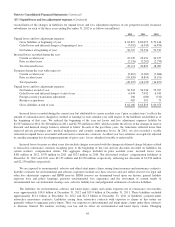

(17) Fair value measurements (Continued)

investments and the reclassification of investment appreciation in earnings, as appropriate in the Consolidated Statements of

Comprehensive Income.

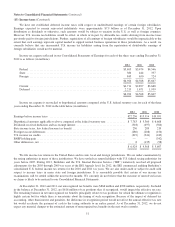

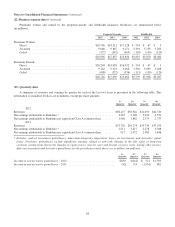

Quantitative information as of December 31, 2012, with respect to assets and liabilities measured and carried at fair value

on a recurring basis with the use of significant unobservable inputs (Level 3) follows (in millions).

Fair

value

Principal valuation

techniques Unobservable Input

Weighted

Average

Other investments:

Preferred stocks ................. $11,860 Discounted cash flow Expected duration 10 years

Discount for transferability

restrictions and subordination 97 basis points

Common stock warrants ........... 3,890 Warrant pricing model Discount for transferability

and hedging restrictions 19%

Net derivative liabilities:

Equity index put options .......... 7,502 Option pricing model Volatility 21%

Credit default-states/municipalities . . 421 Discounted cash flow Credit spreads 85 basis points

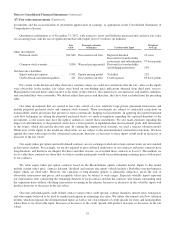

For certain credit default and other derivative contracts where we could not corroborate that the fair values or the inputs

were observable in the market, fair values were based on non-binding price indications obtained from third party sources.

Management reviewed these values relative to the terms of the contracts, the current facts, circumstances and market conditions,

and concluded they were reasonable. We did not adjust these prices and therefore, they have been excluded from the preceding

table.

Our other investments that are carried at fair value consist of a few relatively large private placement transactions and

include perpetual preferred stocks and common stock warrants. These investments are subject to contractual restrictions on

transferability and/or provisions that prevent us from economically hedging our investments. In applying discounted estimated

cash flow techniques in valuing the perpetual preferred stocks, we made assumptions regarding the expected durations of the

investments, as the issuers may have the right to redeem or convert these investments. We also made estimates regarding the

impact of subordination, as the preferred stocks have a lower priority in liquidation than the investment grade debt instruments

of the issuers, which affected the discount rates. In valuing the common stock warrants, we used a warrant valuation model.

While most of the inputs to the model are observable, we are subject to the aforementioned contractual restrictions. We have

applied discounts with respect to the contractual restrictions. Increases or decreases to these inputs would result in decreases or

increases to the fair values.

Our equity index put option and credit default contracts are not exchange traded and certain contract terms are not standard

in derivatives markets. For example, we are not required to post collateral under most of our contracts and many contracts have

long durations, and therefore are illiquid. For these and other reasons, we classified these contracts as Level 3. The methods we

use to value these contracts are those that we believe market participants would use in determining exchange prices with respect

to our contracts.

We value equity index put option contracts based on the Black-Scholes option valuation model. Inputs to this model

include current index price, contract duration, dividend and interest rate inputs (which include a Berkshire non-performance

input) which are observable. However, the valuation of long-duration options is inherently subjective, given the lack of

observable transactions and prices, and acceptable values may be subject to wide ranges. Expected volatility inputs represent

our expectations after considering the remaining duration of each contract and that the contracts will remain outstanding until

the expiration dates without offsetting transactions occurring in the interim. Increases or decreases in the volatility inputs will

produce increases or decreases in the fair values.

Our state and municipality credit default contract values reflect credit spreads, contract durations, interest rates, bond prices

and other inputs believed to be used by market participants in estimating fair value. We utilize discounted cash flow valuation

models, which incorporate the aforementioned inputs as well as our own estimates of credit spreads for states and municipalities

where there is no observable input. Increases or decreases to the credit spreads will produce increases or decreases in the fair

values.

55