Berkshire Hathaway 2012 Annual Report Download - page 5

Download and view the complete annual report

Please find page 5 of the 2012 Berkshire Hathaway annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

2 -

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

|

|

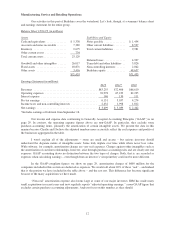

BERKSHIRE HATHAWAY INC.

To the Shareholders of Berkshire Hathaway Inc.:

In 2012, Berkshire achieved a total gain for its shareholders of $24.1 billion. We used $1.3 billion of that

to repurchase our stock, which left us with an increase in net worth of $22.8 billion for the year. The per-share book

value of both our Class A and Class B stock increased by 14.4%. Over the last 48 years (that is, since present

management took over), book value has grown from $19 to $114,214, a rate of 19.7% compounded annually.*

A number of good things happened at Berkshire last year, but let’s first get the bad news out of the way.

ŠWhen the partnership I ran took control of Berkshire in 1965, I could never have dreamed that a year in

which we had a gain of $24.1 billion would be subpar, in terms of the comparison we present on the facing

page.

But subpar it was. For the ninth time in 48 years, Berkshire’s percentage increase in book value was less

than the S&P’s percentage gain (a calculation that includes dividends as well as price appreciation). In

eight of those nine years, it should be noted, the S&P had a gain of 15% or more. We do better when the

wind is in our face.

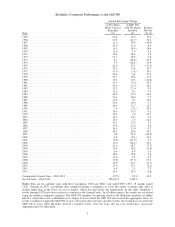

To date, we’ve never had a five-year period of underperformance, having managed 43 times to surpass the

S&P over such a stretch. (The record is on page 103.) But the S&P has now had gains in each of the last

four years, outpacing us over that period. If the market continues to advance in 2013, our streak of five-

year wins will end.

One thing of which you can be certain: Whatever Berkshire’s results, my partner Charlie Munger, the

company’s Vice Chairman, and I will not change yardsticks. It’s our job to increase intrinsic business

value – for which we use book value as a significantly understated proxy – at a faster rate than the market

gains of the S&P. If we do so, Berkshire’s share price, though unpredictable from year to year, will itself

outpace the S&P over time. If we fail, however, our management will bring no value to our investors, who

themselves can earn S&P returns by buying a low-cost index fund.

Charlie and I believe the gain in Berkshire’s intrinsic value will over time likely surpass the S&P returns by

a small margin. We’re confident of that because we have some outstanding businesses, a cadre of terrific

operating managers and a shareholder-oriented culture. Our relative performance, however, is almost

certain to be better when the market is down or flat. In years when the market is particularly strong, expect

us to fall short.

ŠThe second disappointment in 2012 was my inability to make a major acquisition. I pursued a couple of

elephants, but came up empty-handed.

* All per-share figures used in this report apply to Berkshire’s A shares. Figures for the B shares are

1/1500th of those shown for A.

3