Wells Fargo 2012 Annual Report Download - page 95

Download and view the complete annual report

Please find page 95 of the 2012 Wells Fargo annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

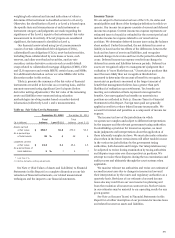

|

|

Regulatory Reform

The past three years have witnessed a significant increase in

regulation and regulatory oversight initiatives that may

substantially change how most U.S. financial services companies

conduct business. The following highlights the more significant

regulations and regulatory oversight initiatives that have

affected or may affect our business. For additional information

about the regulatory reform matters discussed below and other

regulations and regulatory oversight matters, see Part I, Item 1

“Regulation and Supervision” of our 2012 Form 10-K, and the

“Capital Management,” “Forward-Looking Statements” and

“Risk Factors” sections and Note 26 (Regulatory and Agency

Capital Requirements) to Financial Statements in this Report.

Dodd-Frank Act

The Dodd-Frank Act is the most significant financial reform

legislation since the 1930s and is driving much of the current

U.S. regulatory reform efforts. The Dodd-Frank Act and many of

its provisions became effective in July 2010 and July 2011.

However, a number of its provisions still require extensive

rulemaking, guidance, and interpretation by regulatory

authorities, and many of the rules that have been proposed to

implement its requirements either remain open for public

comment or have not otherwise been finalized. Where possible,

the Company may, from time to time, estimate the impact to the

Company’s financial results or business operations as a result of

particular Dodd-Frank Act regulations. However, due to the

uncertainty of pending regulations, the Company may be unable

to make any such estimates. Accordingly, in many respects the

ultimate impact of the Dodd-Frank Act and its effects on the U.S.

financial system and the Company remain uncertain. The

following provides additional information on the Dodd-Frank

Act, including the current status of certain of its rulemaking

initiatives.

x Regulation of swaps and other derivatives activities. The

Dodd-Frank Act establishes a comprehensive framework for

regulating over-the-counter derivatives. Included in this

framework are certain “push-out” provisions affecting U.S.

banks acting as dealers in commodity swaps, equity swaps

and certain credit default swaps, which will require that

these activities be conducted through an affiliate. The

“push-out” provision has an effective date of July 21, 2013,

but the Dodd-Frank Act granted the OCC the discretion to

provide a transition period of up to two years for banks to

come into compliance with the requirements. On

January 3, 2013, the OCC issued guidance that it would

consider transition period requests and favorably act on

such requests subject to the requesting bank meeting

specified requirements. Wells Fargo Bank, N.A. prepared

and filed a transition period request with the OCC on

January 31, 2013.

The Dodd-Frank Act authorizes the Commodities

Futures Trading Commission (CFTC) and SEC (collectively,

the “Commissions”) to regulate swaps and security-based

swaps, respectively. The Commissions jointly adopted new

rules and interpretations that established the compliance

dates for many of the Commissions’ rules implementing the

new regulatory framework for the regulation of swaps and

other derivative activities, including provisional registration

of Wells Fargo Bank as a swap dealer, which occurred at the

end of 2012.

x Volcker Rule. The Volcker Rule will substantially restrict

banking entities from engaging in proprietary trading or

owning any interest in or sponsoring a hedge fund or a

private equity fund. In October 2011, federal banking

agencies and the SEC issued for public comment proposed

regulations to implement the Volcker Rule. The Volcker

Rule became effective in July 2012, but the proposed

implementing regulations have not yet been finalized.

Although the Volcker Rule is now effective, it provides

banking entities with a two year period from its effective

date to come into compliance, with the possibility of limited

further extensions of the compliance period by the FRB. In

April 2012, the FRB issued guidance confirming that

banking entities will have the full two-year compliance

period to conform fully their activities and investments. The

FRB’s guidance also states that banking entities are

expected to engage in “good-faith” planning efforts,

appropriate for their activities and investments, to enable

them to conform all of their activities and investments by no

later than the end of the compliance period. Although

proprietary trading is not significant to our financial results,

and we have reduced or exited certain businesses in

anticipation of the effective date of the Volcker Rule, at this

time and in the absence of final implementing regulations,

the Company cannot predict the ultimate impact of the

Volcker Rule on our trading and investment activities or

financial results.

x Changes to asset-backed securities markets. The Dodd-

Frank Act will generally require sponsors of asset-backed

securities (ABS) to hold at least a 5% ownership stake in the

ABS. Exemptions from the requirement include qualified

residential mortgages and FHA/VA loans. Federal

regulatory authorities proposed joint rules in 2011 to

implement this credit risk retention requirement, which

included an exemption for the GSE’s mortgage-backed

securities. The proposed rules have been subject to

extensive public comment, and the agencies have yet to

issue final rules. As a result, the Company cannot predict

the financial impact of the credit risk retention requirement

on our business.

x The Collins Amendment. This provision of the Dodd-Frank

Act will phase out the benefit of issuing trust preferred

securities by eliminating them from Tier 1 capital over three

years beginning January 2013. For additional information

see the “Capital Management” section of this Report.

x Enhanced supervision and regulation of systemically

significant firms. The Dodd-Frank Act grants broad

authority to banking regulators to establish enhanced

supervisory and regulatory requirements for systemically

important firms. In December 2011, the FRB published

proposed rules that would establish enhanced risk-based

93