Wells Fargo 2012 Annual Report Download - page 64

Download and view the complete annual report

Please find page 64 of the 2012 Wells Fargo annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

|

|

Risk Management – Credit Risk Management (continued)

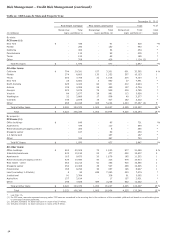

HOME EQUITY PORTFOLIOS Our home equity portfolios consist

of real estate 1-4 family junior lien mortgages and first and

junior lines of credit secured by real estate. Our first lien lines of

credit represent 21% of our home equity portfolio and are

included in real estate 1-4 family first mortgages. The majority of

our junior lien loan products are amortizing payment loans with

fixed interest rates and repayment periods between 5 to 30

years. Junior lien loans with balloon payments at the end of the

repayment term represent a small portion of our junior lien

loans.

Our first and junior lien lines of credit products generally

have a draw period of 10 years with variable interest rates and

payment options during the draw period of (1) interest only or

(2) 1.5% of total outstanding balance. During the draw period,

the borrower has the option of converting all or a portion of the

line from a variable interest rate to a fixed rate with terms

including interest-only payments for a fixed period between

three to seven years or a fully amortizing payment with a fixed

period between five to 30 years. At the end of the draw period, a

line of credit generally converts to an amortizing payment loan

with repayment terms of up to 30 years based on the balance at

time of conversion. At December 31, 2012, our lines of credit

portfolio had an outstanding balance of $84.6 billion, of which

$2.1 billion (2% of our total outstanding balance) is in its

amortization period, another $8.2 billion (10%) will reach their

end of draw period during 2013 through 2014, $29.4 billion

(35%) during 2015 through 2017, and $44.9 billion (53%) will

convert in subsequent years. This portfolio had unfunded credit

commitments of $77.8 billion at December 31, 2012. The lines

that enter their amortization period may experience higher

delinquencies and higher loss rates than the ones in their draw

period. At December 31, 2012, $223 million, or 11% of

outstanding lines of credit that are amortizing, primarily due to

reaching the end of draw period, were 30 or more days past due,

compared with $1.9 billion, or 2% for lines in their draw period.

In anticipation of our customers reaching their contractual end

of draw we have created a process to help borrowers effectively

make the transition from interest-only to fully-amortizing

payments.

We continuously monitor the credit performance of our

junior lien mortgage portfolio for trends and factors that

influence the frequency and severity of loss. We have observed

that the severity of loss for junior lien mortgages is high and

generally not affected by whether we or a third party own or

service the related first mortgage, but that the frequency of loss

has historically been lower when we own or service the first

mortgage. In general, we have limited information available on

the delinquency status of the third party owned or serviced

senior lien where we also hold a junior lien. To capture this

inherent loss content, we use the experience of our junior lien

mortgages behind delinquent first liens that are owned or

serviced by us adjusted for observed higher delinquency rates

associated with junior lien mortgages behind third party first

mortgages. We incorporate this inherent loss content into our

allowance for loan losses. Our allowance process for junior liens

ensures appropriate consideration of the relative difference in

loss experience for junior liens behind first lien mortgage loans

we own or service, compared with those behind first lien

mortgage loans owned or serviced by third parties. In addition,

our allowance process for junior liens that are current, but are in

their revolving period, appropriately reflects the inherent loss

where the borrower is delinquent on the corresponding first lien

mortgage loans.

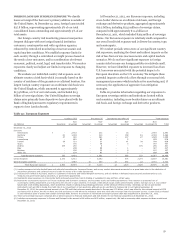

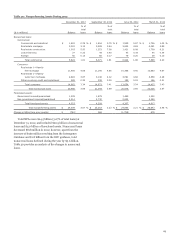

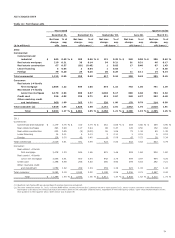

Table 26 summarizes delinquency and loss rates by the

holder of the lien. For additional information regarding current

junior liens behind delinquent first lien loans, see the “Risk

Management – Credit Risk Management – Real Estate 1-4

Family First and Junior Lien Mortgage Loans” section in this

Report.

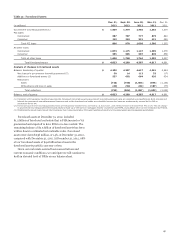

Table 26: Home Equity Portfolios Performance by Holder of 1st Lien (1)

% of loans

two payments

Outstanding balance (2) or more past due Loss rate (annualized) quarter ended

December 31, December 31, Dec. 31, Sept. 30, June 30, Mar. 31, Dec. 31,

(in millions) 2012 2011 2012 2011 2012 (3) 2012 (3) 2012 2012 2011

First lien lines $ 19,744 20,786 3.08 % 3.10 1.00 0.95 0.88 1.35 0.95

Junior lien mortgages and lines behind:

Wells Fargo owned or

serviced first lien 37,913 42,810 2.65 2.91 3.81 4.96 3.34 3.54 3.48

Third party first lien 37,417 42,996 2.86 3.59 3.15 5.40 3.44 3.72 3.83

Total $ 95,074 106,592 2.82 3.22 2.97 4.32 2.89 3.18 3.13

(1)

Excludes PCI loans and real estate 1-4 family first lien line reverse mortgages added to the consumer portfolio in fourth quarter 2011 as a result of consolidating reverse

mortgage loans previously sold. These reverse mortgage loans are predominantly insured by the FHA.

(2) Includes $1.3 billion and $1.5 billion at December 31, 2012 and 2011, respectively, associated with the Pick-a-Pay portfolio.

(3) Reflects the OCC guidance issued in third quarter 2012, which requires consumer loans discharged in bankruptcy to be written down to net realizable collateral value, regardless

of their delinquency status. The junior lien loss rates for third quarter 2012 reflect losses based on estimates of collateral value to implement the OCC guidance, which were then

adjusted in the fourth quarter to reflect actual appraisals. Fourth quarter 2012 losses on the junior liens where Wells Fargo own or services first lien remained elevated primarily

due to the OCC guidance.

62