Wells Fargo 2012 Annual Report Download - page 192

Download and view the complete annual report

Please find page 192 of the 2012 Wells Fargo annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

182 -

183

183 -

184

184 -

185

185 -

186

186 -

187

187 -

188

188 -

189

189 -

190

190 -

191

191 -

192

192 -

193

193 -

194

194 -

195

195 -

196

196 -

197

197 -

198

198 -

199

199 -

200

200 -

201

201 -

202

202 -

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

|

|

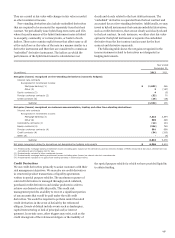

Note 15: Legal Actions

Wells Fargo and certain of our subsidiaries are involved in a

number of judicial, regulatory and arbitration proceedings

concerning matters arising from the conduct of our business

activities. These proceedings include actions brought against

Wells Fargo and/or our subsidiaries with respect to corporate

related matters and transactions in which Wells Fargo and/or

our subsidiaries were involved. In addition, Wells Fargo and our

subsidiaries may be requested to provide information or

otherwise cooperate with government authorities in the conduct

of investigations of other persons or industry groups.

Although there can be no assurance as to the ultimate

outcome, Wells Fargo and/or our subsidiaries have generally

denied, or believe we have a meritorious defense and will deny,

liability in all significant litigation pending against us, including

the matters described below, and we intend to defend vigorously

each case, other than matters we describe as having settled.

Reserves are established for legal claims when payments

associated with the claims become probable and the costs can be

reasonably estimated. The actual costs of resolving legal claims

may be substantially higher or lower than the amounts reserved

for those claims.

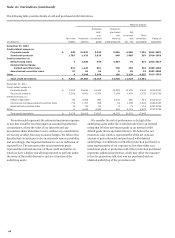

FHA INSURANCE LITIGATION On October 9, 2012, the United

States filed a complaint, captioned United States of America v.

Wells Fargo Bank, N.A., in the U.S. District Court for the

Southern District of New York. The complaint makes claims with

respect to Wells Fargo’s Federal Housing Administration (FHA)

lending program for the period 2001 to 2010. The complaint

alleges, among other allegations, that Wells Fargo improperly

certified certain FHA mortgage loans for United States

Department of Housing and Urban Development (HUD)

insurance that did not qualify for the program, and therefore

Wells Fargo should not have received insurance proceeds from

HUD when some of the loans later defaulted. The complaint

further alleges Wells Fargo knew some of the mortgages did not

qualify for insurance and did not disclose the deficiencies to

HUD before making insurance claims. On December 1, 2012,

Wells Fargo filed a motion in the U.S. District Court for the

District of Columbia seeking to enforce a release of Wells Fargo

given by the United States, which was denied on

February 12, 2013. On December 14, 2012, the United States

filed an amended complaint. On January 16, 2013, Wells Fargo

filed a motion in the Southern District of New York to dismiss

the amended complaint.

INTERCHANGE LITIGATION Wells Fargo Bank, N.A., Wells

Fargo & Company, Wachovia Bank, N.A. and Wachovia

Corporation are named as defendants, separately or in

combination, in putative class actions filed on behalf of a

plaintiff class of merchants and in individual actions brought by

individual merchants with regard to the interchange fees

associated with Visa and MasterCard payment card transactions.

These actions have been consolidated in the U.S. District Court

for the Eastern District of New York. Visa, MasterCard and

several banks and bank holding companies are named as

defendants in various of these actions. The amended and

consolidated complaint asserts claims against defendants based

on alleged violations of federal and state antitrust laws and seeks

damages, as well as injunctive relief. Plaintiff merchants allege

that Visa, MasterCard and payment card issuing banks

unlawfully colluded to set interchange rates. Plaintiffs also allege

that enforcement of certain Visa and MasterCard rules and

alleged tying and bundling of services offered to merchants are

anticompetitive. Wells Fargo and Wachovia, along with other

defendants and entities, are parties to Loss and Judgment

Sharing Agreements, which provide that they, along with other

entities, will share, based on a formula, in any losses from the

Interchange Litigation. On July 13, 2012, Visa, MasterCard and

the financial institution defendants, including Wells Fargo,

signed a memorandum of understanding with plaintiff

merchants to resolve the consolidated class actions and reached

a separate settlement in principle of the consolidated individual

actions. The proposed settlement payments by all defendants in

the consolidated class and individual actions total approximately

$6.6 billion. The class settlement also provides for the

distribution to class merchants of 10 basis points of default

interchange across all credit rate categories for a period of eight

consecutive months. The Court has granted preliminary

approval of the settlements. The settlements are subject to

further review and approval by the Court.

MEDICAL CAPITAL CORPORATION LITIGATION Wells Fargo

Bank, N.A. served as indenture trustee for debt issued by

affiliates of Medical Capital Corporation, which was placed in

receivership at the request of the Securities and Exchange

Commission (SEC) in August 2009. Since September 2009,

Wells Fargo has been named as a defendant in various class and

mass actions brought by holders of Medical Capital

Corporation’s debt, alleging that Wells Fargo breached

contractual and other legal obligations owed to them and seeking

unspecified damages. The actions have been consolidated in the

U.S. District Court for the Central District of California. On

July 26, 2011, the District Court certified a class consisting of

holders of notes issued by affiliates of Medical Capital

Corporation and, on October 18, 2011, the Ninth Circuit Court of

Appeals denied a petition seeking to appeal the class certification

order. A previously disclosed potential settlement of the case was

not consummated and the case is in discovery.

MARYLAND MORTGAGE LENDING LITIGATION On December

26, 2007, a class action complaint captioned Denise Minter, et

al., v. Wells Fargo Bank, N.A., et al., was filed in the U.S.

District Court for the District of Maryland. The complaint alleges

that Wells Fargo and others violated provisions of the Real

Estate Settlement Procedures Act and other laws by conducting

mortgage lending business improperly through a general

partnership, Prosperity Mortgage Company. The complaint

asserts that Prosperity Mortgage Company was not a legitimate

affiliated business and instead operated to conceal Wells Fargo

Bank, N.A.’s role in the loans at issue. A plaintiff class of

borrowers who received a mortgage loan from Prosperity that

was funded by Prosperity’s line of credit with Wells Fargo Bank,

190