Wells Fargo 2012 Annual Report Download - page 230

Download and view the complete annual report

Please find page 230 of the 2012 Wells Fargo annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

220 -

221

221 -

222

222 -

223

223 -

224

224 -

225

225 -

226

226 -

227

227 -

228

228 -

229

229 -

230

230 -

231

231 -

232

232 -

233

233 -

234

234 -

235

235 -

236

236 -

237

237 -

238

238 -

239

239 -

240

240 -

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

|

|

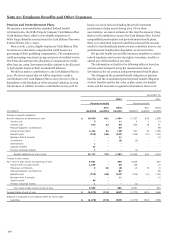

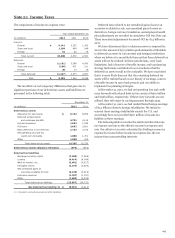

Note 20: Employee Benefits and Other Expenses (continued)

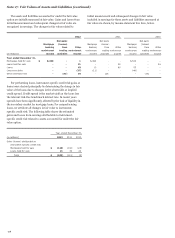

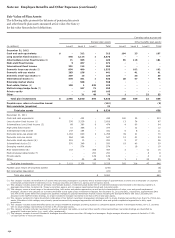

Amounts recognized in accumulated OCI (pre tax) consist of:

December 31,

2012 2011

Pension benefits Pension benefits

Non- Other Non- Other

(in millions) Qualified qualified benefits Qualified qualified benefits

Net actuarial loss $ 3,323 184 19 2,699 137 61

Net prior service credit (2) - (25) - - (27)

Net transition obligation - - 1 - - 1

Total $ 3,321 184 (5) 2,699 137 35

The net actuarial loss for the defined benefit pension plans

and other post retirement plans that will be amortized from

accumulated OCI into net periodic benefit cost in 2013 is

$182 million. The net prior service credit for the defined benefit

pension plans and other post retirement plans that will be

amortized from accumulated OCI into net periodic benefit cost

in 2013 is $2 million.

Plan Assumptions

For the years ended December 31, 2012 and 2011, the weighted-

average discount rate used to estimate the projected benefit

obligation for pension benefits (qualified and nonqualified) was

4.00% and 5.00%, respectively, and for other postretirement

benefits was 3.75% and 4.75%, respectively. For additional

information on our pension accounting assumptions, see Note 1.

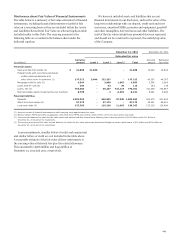

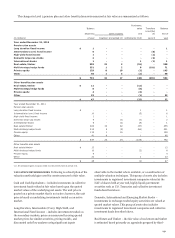

The weighted-average assumptions used to determine the net periodic benefit cost were:

December 31,

2012 2011 2010

Pension Other Pension Other Pension Other

benefits (1) benefits benefits (1) benefits benefits (1) benefits

Discount rate 5.00 % 4.75 5.25 5.25 5.75 5.75

Expected return on plan assets 7.50 6.00 8.25 6.00 8.25 8.25

(1) Includes both qualified and nonqualified pension benefits.

To account for postretirement health care plans we use

health care cost trend rates to recognize the effect of expected

changes in future health care costs due to medical inflation,

utilization changes, new technology, regulatory requirements

and Medicare cost shifting. In determining the end of year

benefit obligation we assume a range of average annual increases

of approximately 7.00% and 8.75%, dependent on plan type, for

health care costs in 2013. These rates are assumed to trend down

0.25% per year until the trend rate reaches an ultimate rate of

5.00% in 2020 through 2028, dependent on plan type. The 2012

periodic benefit cost was determined using initial annual trend

rates of 7.75%. These rates were assumed to decrease 0.25% per

year until they reached ultimate rates of 5.00% in 2023.

Increasing the assumed health care trend by one percentage

point in each year would increase the benefit obligation as of

December 31, 2012, by $58 million and the total of the interest

cost and service cost components of the net periodic benefit cost

for 2012 by $3 million. Decreasing the assumed health care

trend by one percentage point in each year would decrease the

benefit obligation as of December 31, 2012, by $52 million and

the total of the interest cost and service cost components of the

net periodic benefit cost for 2012 by $2 million.

Investment Strategy and Asset Allocation

We seek to achieve the expected long-term rate of return with a

prudent level of risk given the benefit obligations of the pension

plans and their funded status. Our overall investment strategy is

designed to provide our Cash Balance Plan with a balance of

long-term growth opportunities and short-term benefit

strategies while ensuring that risk is mitigated through

diversification across numerous asset classes and various

investment strategies. We target the asset allocation for our Cash

Balance Plan at a target mix range of 35-55% equities, 35-55%

fixed income, and approximately 10% in real estate, venture

capital, private equity and other investments. The Employee

Benefit Review Committee (EBRC), which includes several

members of senior management, formally reviews the

investment risk and performance of our Cash Balance Plan on a

quarterly basis. Annual Plan liability analysis and periodic

asset/liability evaluations are also conducted.

Other benefit plan assets include (1) assets held in a 401(h)

trust, which are invested with a target mix of 40-60% for both

equities and fixed income, and (2) assets held in the Retiree

Medical Plan Voluntary Employees' Beneficiary Association

(VEBA) trust, which are invested with a general target asset mix

of 20-40% equities and 60-80% fixed income. In addition, the

strategy for the VEBA trust assets considers the effect of income

228