TCF Bank 2010 Annual Report Download - page 99

Download and view the complete annual report

Please find page 99 of the 2010 TCF Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

|

|

• 83 •

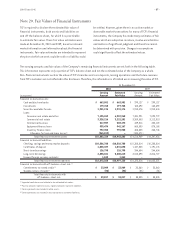

2010 Form 10-K

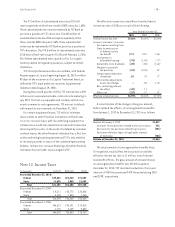

At December 31, 2010

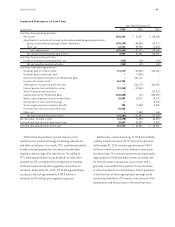

Receivables Payables

Not Not

Notional Designated Designated Designated Designated

(In thousands) Amount as Hedges as Hedges Total as Hedges as Hedges Total

Forward foreign exchange contracts $185,540 $ 12 $ 3 $ 15 $198 $1,659 $1,857

Netting adjustments (1) (12) (3) (15) (12) (3) (15)

Carrying value of contracts $ – $ – $ – $186 $1,656 $1,842

(1) Foreign exchange contract receivables and payables, and the related cash collateral received and paid are netted when a legally enforceable master netting agreement

exists between TCF and a counterparty.

The value of forward foreign exchange contracts will

vary over their contractual lives as the related currency

exchange rates fluctuate. The accounting for changes in the

fair value of a forward foreign exchange contract depends

on whether or not the contract has been designated and

qualifies as a hedge. To qualify as a hedge, a contract must

be highly effective at reducing the risk associated with the

exposure being hedged. In addition, for a contract to be

designated as a hedge, the risk management objective and

strategy must be documented. Hedge documentation must

also identify the hedging instrument, the asset or liability

and type of risk to be hedged and how the effectiveness of

the contract is assessed prospectively and retrospectively.

To assess effectiveness, TCF uses statistical methods such

as regression analysis. The extent to which a contract

has been, and is expected to continue to be effective

at offsetting changes in cash flows or the net investment

must be assessed and documented at least quarterly. If

it is determined that a contract is not highly effective at

hedging the designated exposure, hedge accounting

is discontinued.

Upon origination of a forward foreign exchange contract,

the contract is designated either as a hedge of a forecasted

transaction or the variability of cash flows to be paid related

to a recognized asset or liability (“cash flow hedge”); or a

hedge of the volatility of an investment in foreign operations

driven by changes in foreign currency exchange rates (“net

investment hedge”). To the extent that a hedge is effective,

changes in fair value are recorded within accumulated other

comprehensive income (loss), with any ineffectiveness

recorded in non-interest expense. Changes in cash flow

hedges recorded within other comprehensive income (loss)

are subsequently reclassified to non-interest expense

upon completion of the sale. Changes in net investment

hedges recorded within other comprehensive income

(loss) are subsequently reclassified to non-interest

expense during the period in which the foreign investment

is substantially liquidated or when other elements of the

currency translation adjustment are reclassified to income.

If a hedged forecasted transaction is no longer probable,

hedge accounting is ceased and any gain or loss included in

other comprehensive income (loss) is reported in earnings

immediately. Changes in the values of forward foreign

exchange contracts that are not designated as hedges are

reflected in non-interest expense.

Cash Flow Hedges Foreign exchange contracts, which

include forward contracts, are used to manage the foreign

exchange risk associated with the TCF’s minimum lease

payment stream. These foreign exchange contracts are

hedges of the forecasted cash flows from the underlying

lease agreement expected through June 30, 2011. At

December 31, 2010, the Company had $1 thousand of

unrealized losses on derivatives classified as cash flow

hedges recorded in other comprehensive income (loss).

The estimated amount to be reclassified from other

comprehensive income (loss) into earnings during the next

12 months is a loss of $1 thousand.

Net Investment Hedges Foreign exchange contracts,

which include forward contracts and currency options, are

used to manage the foreign exchange risk associated with

the Company’s net investment in TCF Commercial Finance

Canada, Inc., a wholly-owned Canadian subsidiary,

along with certain assets, liabilities and forecasted

transactions of that subsidiary. The net amount of related

gains or losses included in the cumulative translation

adjustment for the year ended December 31, 2010 was a

loss of $195 thousand.