TCF Bank 2010 Annual Report Download - page 22

Download and view the complete annual report

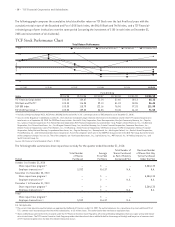

Please find page 22 of the 2010 TCF Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

|

|

• 6 • TCF Financial Corporation and Subsidiaries

be subject to certain nationwide and statewide insured

deposit maximum concentration levels or other limitations.

Insurance of Accounts On November 9, 2010, the FDIC

issued a Final Rule implementing section 343 of the Dodd-

Frank Act that provides for unlimited insurance coverage

of certain non-interest bearing accounts. Beginning

December 31, 2010, through December 31, 2012, all non-

interest bearing transaction accounts are fully insured,

regardless of the balance of the account, at all FDIC-

insured institutions. The unlimited insurance coverage is

available to all depositors, including consumers, businesses,

and government entities. This unlimited insurance coverage

is separate from, and in addition to, the insurance coverage

provided to a depositor’s other deposit accounts held at an

FDIC-insured institution.

The FDIC has set a designated reserve ratio of 1.35%

($1.35 for each $100 of insured deposits) for the Deposit

Insurance Fund (“DIF”). The Federal Deposit Insurance Act

of 2005 (“FDIC Act”) provides the FDIC Board of Directors

the authority to set the designated reserve ratio between

1.15% and 1.50%. The FDIC must adopt a restoration plan

when the reserve ratio falls below 1.15% and begin paying

dividends when the reserve ratio exceeds 1.35%. There is

no requirement to achieve a specific ratio within a given

timeframe. The DIF reserve ratio calculated by the FDIC

at September 30, 2010 was a negative .15% and therefore,

the FDIC needs to increase premiums charged to banks.

In 2010, the annual insurance premiums on bank

deposits insured by the DIF varied between $.07 per $100

of deposits for banks classified in the highest capital

and supervisory evaluation categories to $.78 per $100

of deposits for banks classified in the lowest capital and

supervisory evaluation categories.

On November 12, 2009, the FDIC adopted a final rule

requiring depository institutions to prepay their estimated

quarterly insurance premium for fourth quarter 2009 and

all of 2010, 2011 and 2012. TCF Bank prepaid $77.6 million

of such premium on December 30, 2009 and $50.5 million

remained as a prepaid balance at December 31, 2010.

The expense related to this prepayment is anticipated to

be recognized over the next two years based on actual

calculations of quarterly premiums.

The Dodd-Frank Act requires changes to a number of

components of the FDIC insurance assessment, with an

implementation date of April 1, 2011. The changes amend

the current methodology used to determine the assess-

ments paid by institutions with assets greater than $10

billion, including changing the assessment base from

deposits to total average assets less tier one capital.

Additionally, the FDIC has developed a scorecard approach

to determine a separate assessment rate for each institution

with assets greater than $10 billion. As a result of these

changes, TCF’s FDIC insurance expense is expected to increase

by approximately $15 million in 2011.

In addition to risk-based deposit insurance premiums,

additional assessments may be imposed by the Financing

Corporation, a separate U.S. government agency affiliated

with the FDIC, on insured deposits to pay for the interest

cost of Financing Corporation bonds. Financing Corporation

assessment rates for 2010 ranged from $.0102 to $.0104 for

each $100 of deposits. Financing Corporation assessments

of $1.2 million, $1.2 million and $1.1 million were paid by

TCF Bank for 2010, 2009 and 2008, respectively.

Under federal law, deposits and certain claims for

administrative expenses and employee compensation

against an insured depository institution are afforded a

priority over other general unsecured claims against such

an institution, including federal funds and letters of credit,

in the liquidation or other resolution of such an institution

by any receiver appointed by regulatory authorities. Such

priority creditors would include the FDIC.

Examinations and Regulatory Sanctions TCF is

subject to periodic examination by the Federal Reserve,

OCC and the FDIC. Bank regulatory authorities may impose

a number of restrictions or new requirements on institu-

tions, including, but not limited to, growth limitations,

dividend restrictions, individual increased regulatory

capital requirements, increased loan, lease and real estate

loss reserve requirements, increased supervisory assess-

ments, activity limitations or other restrictions that could

have an adverse effect on such institutions, their holding

companies or holders of their debt and equity securities.

Certain enforcement actions may not be publicly disclosed

by TCF or its regulatory authorities. Various enforcement

remedies, including civil money penalties, may be assessed

against an institution or an institution’s directors, officers,

employees, agents or independent contractors. Under the

Bank Secrecy Act (“BSA”), the OCC is obligated to take

enforcement action where it finds a statutory or regulatory

violation that would constitute a program violation.

In its 2009 examinations of TCF’s compliance with

the BSA, the OCC identified instances of non-compliance

that constitute a program violation. On July 20, 2010,

TCF National Bank agreed to the issuance of a