TCF Bank 2010 Annual Report Download - page 5

Download and view the complete annual report

Please find page 5 of the 2010 TCF Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

2 -

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

|

|

At year-end, TCF reported its 63rd consecutive quarter of protability.

value the overdraft services provided

by TCF. Since implementation, we have

seen a decline in overall fees and

service charges, but this decline has

been less significant than that of most

of our competitors. Our success with

opt-in, as well as our implementation

of new account maintenance fees,

demonstrates our willingness and ability

to meet regulatory challenges head-on.

Dodd-Frank Act, particularly the Durbin

Amendment TCF senior management,

with the assistance of third party

experts, extensively researched the

legality of provisions of the Dodd-Frank

Act known as the Durbin Amendment,

that limit the ability of banks to receive

debit card interchange fees. On October

12, 2010, TCF filed a lawsuit challenging

the constitutionality of the Durbin

Amendment. We believe the provisions

of the Durbin Amendment clearly

violate multiple constitutional rights of

TCF and similarly situated banks. More

specifically, the rights that have been

compromised deal with our ability to

earn a fair rate of return on our invested

capital and to compete on even ground

with banks exempted by the law. In

December 2010, the Federal Reserve

Board issued a proposed regulation

based on the Durbin Amendment

creating proposed caps on interchange

fees that, if implemented, will result

in a significant revenue loss for banks

like TCF. Since the Fed announced its

proposal, we have seen more and more

parties express increased concern

about the potential implications of the

Durbin Amendment. Our lawsuit has

certainly been the right thing to do for

our customers and stockholders and

we remain confident that a favorable

outcome can be achieved.

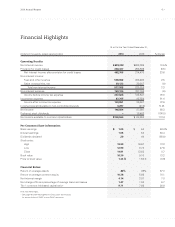

• Despite the lingering economic crisis,

TCF earned $146.6 million in 2010, up

68 percent from the previous year.

Diluted earnings per common share

was $1.05, up 94 percent from 2009.

• TCF’s net interest margin was 4.14

percent for the full year of 2010 and

4.04 percent in the fourth quarter of

2010. Our industry leading deposit

strategies and continued reduction of

high interest-rate certificates of deposit

balances contributed significantly to net

interest margin. During 2010, we took

certain actions to increase the asset

sensitivity of the balance sheet in

anticipation of rising interest rates,

which included changing the mix of

fixed- and variable-rate loans. This has

limited expansion of the net interest

margin in the short-term, but is in the

best long-term interest of the company.

Overall, TCF’s net interest margin

continues to be better than the

average of the Top 50 Banks by

approximately 68 basis points.

• 3 •

2010 Annual Report