Xerox 2003 Annual Report Download - page 50

Download and view the complete annual report

Please find page 50 of the 2003 Xerox annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

|

|

48

healthcare costs, the rate of future compensation

increases, and mortality, among others. Actual returns

on plan assets are not immediately recognized in our

income statement, due to the delayed recognition

requirement. In calculating the expected return on the

plan asset component of our net periodic pension

cost, we apply our estimate of the long term rate of

return to the plan assets that support our pension obli-

gations, after deducting assets that are specifically

allocated to Transitional Retirement Accounts (which

are accounted for based on specific plan terms).

For purposes of determining the expected return

on plan assets, we utilize a calculated value approach

in determining the value of the pension plan assets, as

opposed to a fair market value approach. The primary

difference between the two methods relates to system-

atic recognition of changes in fair value over time

(generally two years) versus immediate recognition of

changes in fair value. Our expected rate of return on

plan assets is then applied to the calculated asset value

to determine the amount of the expected return on

plan assets to be used in the determination of the net

periodic pension cost. The calculated value approach

reduces the volatility in net periodic pension cost that

results from using the fair market value approach.

The difference between the actual return on plan

assets and the expected return on plan assets is added

to, or subtracted from, any cumulative differences that

arose in prior years. This amount is a component of

the unrecognized net actuarial (gain) loss and is sub-

ject to amortization to net periodic pension cost over

the remaining service lives of the employees partici-

pating in the pension plan.

Another significant assumption affecting our pen-

sion and post-retirement benefit obligations and the

net periodic pension and other post-retirement benefit

cost is the rate that we use to discount our future antic-

ipated benefit obligations. In estimating this rate, we

consider rates of return on high quality fixed-income

investments over the period to expected payment of

the pension and other post-retirement benefits.

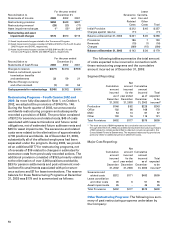

Stock-Based Compensation: We do not recognize

compensation expense relating to employee stock

options because the exercise price is equal to the mar-

ket price at the date of grant. If we had elected to rec-

ognize compensation expense using a fair value

approach, and therefore determined the compensa-

tion based on the value as determined by the modified

Black-Scholes option pricing model, our pro forma

income (loss) and income (loss) per share would have

been as follows:

Land, Buildings and Equipment and Equipment on

Operating Leases: Land, buildings and equipment are

recorded at cost. Buildings and equipment are depreci-

ated over their estimated useful lives. Leasehold

improvements are depreciated over the shorter of the

lease term or the estimated useful life. Equipment on

operating leases is depreciated to estimated residual

value over the lease term. Depreciation is computed

using the straight-line method. Significant improve-

ments are capitalized and maintenance and repairs are

expensed. Refer to Notes 5 and 6 for further discussion.

Impairment of Long-Lived Assets: We review the

recoverability of our long-lived assets, including build-

ings, equipment, internal-use software and other

intangible assets, when events or changes in circum-

stances occur that indicate that the carrying value of

the asset may not be recoverable. The assessment of

possible impairment is based on our ability to recover

the carrying value of the asset from the expected

future pre-tax cash flows (undiscounted and without

interest charges) of the related operations. If these

cash flows are less than the carrying value of such

asset, an impairment loss is recognized for the differ-

ence between estimated fair value and carrying value.

Our primary measure of fair value is based on dis-

counted cash flows. The measurement of impairment

requires management to make estimates of these cash

flows related to long-lived assets, as well as other fair

value determinations.

Research and Development Expenses: Research and

development costs are expensed as incurred.

Pension and Post-Retirement Benefit Obligations: We

sponsor pension plans in various forms in several

countries covering substantially all employees who

meet eligibility requirements. Post-retirement benefit

plans cover primarily U.S. employees for retirement

medical costs. As required by existing accounting

rules, we employ a delayed recognition feature in

measuring the costs and obligations of pension and

post-retirement benefit plans. This requires changes in

the benefit obligations and changes in the value of

assets set aside to meet those obligations, to be rec-

ognized, not as they occur, but systematically and

gradually over subsequent periods. All changes are

ultimately recognized, except to the extent they may

be offset by subsequent changes. At any point,

changes that have been identified and quantified

await subsequent accounting recognition as net cost

components and as liabilities or assets.

Several statistical and other factors that attempt to

anticipate future events are used in calculating the

expense, liability and asset values related to our pen-

sion and post-retirement benefit plans. These factors

include assumptions we make about the discount rate,

expected return on plan assets, rate of increase in