Xerox 2003 Annual Report Download - page 33

Download and view the complete annual report

Please find page 33 of the 2003 Xerox annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

|

|

31

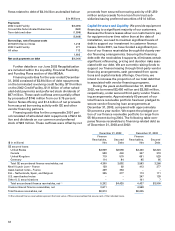

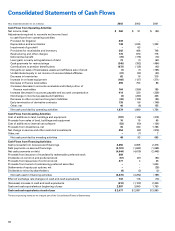

This trend is expected to moderate as our equipment

sales continue to increase. These cash flows were par-

tially offset by pension plan contributions of $672 mil-

lion related to our decision to accelerate and increase

the 2003 funding level of our U.S. plans and increase

the 2003 funding level of our U.K. plans, restructuring

related cash payments of $345 million, income tax

payments of $207 million and $166 million of cash out-

flow supporting our on-lease equipment investment.

The $101 million decline in operating cash flow

versus 2002 primarily reflects increased pension plan

contributions of $534 million, lower finance receivable

reductions of $258 million reflecting the increase in

equipment sale revenue in 2003, and increased on-lease

equipment investment of $39 million. These items

were partially offset by increased pre-tax income of

$332 million, lower tax payments of $235 million and

increased cash proceeds from the early termination

of interest rate swaps of $80 million. The lower tax

payments reflect the absence of the $346 million tax

payment associated with the 2001 sale of a portion of

our ownership interest in Fuji Xerox.

For the year ended December 31, 2002, operating

cash flows of $2.0 billion reflect pre-tax income of

$104 million and the following non-cash items: depre-

ciation and amortization of $1,035 million, provisions

for receivables and inventory of $468 million and

impairment of goodwill of $63 million. Cash flows

were also enhanced by finance receivable reductions

of $754 million due to collection of receivables from

prior year’s sales without an offsetting receivables

increase due to lower equipment sales in 2002, togeth-

er with a transition to third-party vendor financing

arrangements in the Nordic countries, Italy, Brazil and

Mexico. In addition, a restructuring charge of $670 mil-

lion was recorded during the period. These items were

partially offset by $442 million of tax payments,

including $346 million related to the 2001 sale of half

of our interest in Fuji Xerox, $392 million of restructur-

ing payments, $127 million of on-lease equipment

expenditures and a $138 million cash contribution to

our pension plans.

The $226 million improvement in operating cash

flow as compared to 2001 reflects increased finance

receivable collections of $666 million, an improvement

in cash flows from the early termination of derivative

contracts of $204 million, lower on-lease equipment

spending of $144 million and lower restructuring pay-

ments of $92 million. The decline in 2002 on-lease

equipment spending reflected declining rental place-

ment activity and populations, particularly in our

older-generation light-lens products. These items were

partially offset by higher cash taxes of $385 million,

higher pension contributions of $96 million and

increased working capital uses of over $400 million,

much of which was caused by the termination of an

accounts receivable sales facility. In addition, cash

flow generated by reducing inventory during 2002

occurred at a much slower rate than in 2001 as inven-

tory reductions were offset by increased requirements

for new product launches.

We expect operating cash flows to approximate

$1.5 billion in 2004, as compared to $1.9 billion in

2003. The reduction contemplates finance receivables

growth as a result of continued expected equipment

sales expansion as well as the absence of early deriva-

tive contract termination cash flow, partially offset by

reduced restructuring payments and lower pension

contributions.

Investing: Investing cash flows for the year ended

December 31, 2003 consisted primarily of $235 million

released from restricted cash related to former rein-

surance obligations associated with our discontinued

operations, $35 million of aggregate cash proceeds

from the divestiture of our investment in Xerox South

Africa, XES France and Germany and other minor

investments, partially offset by capital and internal use

software spending of $250 million. We expect 2004

capital expenditures to approximate $250 million.

Investing cash flows for the year ended December

31, 2002 consisted primarily of proceeds of $200 mil-

lion from the sale of our Italian leasing business, $53

million related to the sale of certain manufacturing

locations to Flextronics, $67 million related to the sale

of our interest in Katun and $19 million from the sale

of our investment in Prudential common stock. These

inflows were partially offset by capital and internal use

software spending of $196 million and increased

requirements of $63 million for restricted cash sup-

porting our vendor financing activities.

Investing cash flows in 2001 largely consisted of

the $1,768 million of cash received from sales of busi-

nesses, including one half of our interest in Fuji Xerox,

our leasing businesses in the Nordic countries and

certain manufacturing assets to Flextronics. These

cash proceeds were offset by capital and internal use

software spending of $343 million, a $255 million pay-

ment related to our funding of trusts to replace letters

of credit within our insurance discontinued operations,

$115 million of payments for the funding of escrow

requirements related to lease contracts transferred to

GE, $229 million of payments for the funding of

escrow requirements related to pre-funded interest

payments required to support our liabilities to trusts

issuing preferred securities and $217 million of pay-

ments for other contractual requirements.

Financing: Financing activities for the year ended

December 31, 2003 consisted of net proceeds from

secured borrowing activity with GE and other vendor

financing partners of $269 million, net proceeds from

the June 2003 convertible preferred stock offering of

$889 million, net proceeds from the June 2003 com-

mon stock offering of $451 million, offset by preferred

stock dividends of $57 million and other net cash out-