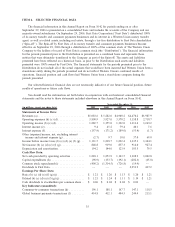

Western Union 2009 Annual Report Download - page 45

Download and view the complete annual report

Please find page 45 of the 2009 Western Union annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

|

|

Risks Relating to the Spin-Off

We were incorporated in Delaware as a wholly-owned subsidiary of First Data on February 17, 2006. On

September 29, 2006, First Data distributed 100% of its money transfer and consumer payments businesses and

its interest in a Western Union money transfer agent, as well as related assets, including real estate, through a

tax-free distribution to First Data shareholders (“Spin-off ”) through this previously owned subsidiary.

If the Spin-off does not qualify as a tax-free transaction, First Data and its stockholders could be subject to

material amounts of taxes and, in certain circumstances, we could be required to indemnify First Data for

material taxes pursuant to indemnification obligations under the tax allocation agreement.

First Data received a private letter ruling from the IRS to the effect that, the Spin-off (including certain

related transactions) qualifies as tax-free to First Data, us and First Data stockholders for United States federal

income tax purposes under sections 355, 368 and related provisions of the Internal Revenue Code, assuming,

among other things, the accuracy of the representations made by First Data with respect to certain matters on

which the IRS did not rule. If the factual assumptions or representations made in the private letter ruling

request were determined to be untrue or incomplete, then First Data and ourselves would not be able to rely

on the ruling.

The Spin-off was conditioned upon First Data’s receipt of an opinion of Sidley Austin LLP, counsel to

First Data, to the effect that, with respect to requirements on which the IRS did not rule, those requirements

would be satisfied. The opinion was based on, among other things, certain assumptions and representations as

to factual matters made by First Data and us which, if untrue or incomplete, would jeopardize the conclusions

reached by counsel in its opinion. The opinion is not binding on the IRS or the courts, and the IRS or the

courts may not agree with the opinion.

If, notwithstanding receipt of the private letter ruling and opinion of tax counsel, the Spin-off were

determined to be a taxable transaction, each holder of First Data common stock who received shares of our

common stock in connection with the Spin-off would generally be treated as receiving a taxable distribution in

an amount equal to the fair value of our common stock received. First Data would recognize taxable gain

equal to the excess of the fair value of the consideration received by First Data in the contribution over First

Data’s tax basis in the assets contributed to us in the contribution. If First Data were unable to pay any taxes

for which it is responsible under the tax allocation agreement, the IRS might seek to collect such taxes from

Western Union.

Even if the Spin-off otherwise qualified as a tax-free distribution under section 355 of the Internal

Revenue Code, the Spin-off may result in significant United States federal income tax liabilities to First Data

if 50% or more of First Data’s stock or our stock (in each case, by vote or value) is treated as having been

acquired, directly or indirectly, by one or more persons as part of a plan (or series of related transactions) that

includes the Spin-off. For purposes of this test, any acquisitions, or any understanding, arrangement or

substantial negotiations regarding an acquisition, within two years before or after the Spin-off are subject to

special scrutiny.

With respect to taxes and other liabilities that could be imposed as a result of a final determination that is

inconsistent with the anticipated tax consequences of the Spin-off (as set forth in the private letter ruling and

relevant tax opinion) (“Spin-off Related Taxes”), we, one of our affiliates or any person that, after the Spin-

off, is an affiliate thereof, will be liable to First Data for any such Spin-off Related Taxes attributable solely to

actions taken by or with respect to us. In addition, we will also be liable for 50% of any Spin-off Related

Taxes (i) that would not have been imposed but for the existence of both an action by us and an action by

First Data or (ii) where we and First Data each take actions that, standing alone, would have resulted in the

imposition of such Spin-off Related Taxes. We may be similarly liable if we breach certain representations or

covenants set forth in the tax allocation agreement. If we are required to indemnify First Data for taxes

incurred as a result of the Spin-off being taxable to First Data, it likely would have an adverse effect on our

business, financial position, results of operations and cash flows.

31