Travelers 2014 Annual Report Download - page 98

Download and view the complete annual report

Please find page 98 of the 2014 Travelers annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

|

|

Table of Contents

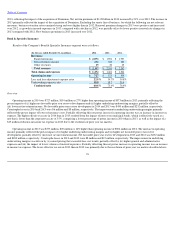

Operating income in 2013 was $838 million, $621 million higher than operating income of $217 million in 2012. The increase in operating income

primarily reflected the pretax impact of (i) lower catastrophe losses, (ii) higher underlying underwriting margins, (iii) an increase in other revenues

and (iv) higher net favorable prior year reserve development, partially offset by (v) lower net investment income. Catastrophe losses in 2013 and

2012 were $250 million and $1.02 billion, respectively. Net favorable prior year reserve development in 2013 and 2012 was $209 million and

$175 million, respectively. The improvement in underlying underwriting margins resulted from the impact of earned pricing that exceeded loss cost

trends and lower non

-

catastrophe weather

-

related losses. Partially offsetting this net pretax increase in operating income was an increase in income

tax expense. The higher effective tax rate in 2013 than in 2012 primarily resulted from interest on municipal bonds, which is effectively taxed at a rate

that is lower than the corporate tax rate of 35%, comprising a lower percentage of pretax income in 2013 than in 2012.

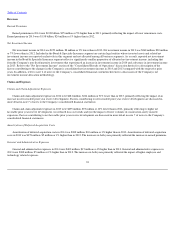

Revenues

Earned Premiums

Earned premiums in 2014 were $7.13 billion, $199 million or 3% lower than in 2013. Earned premiums in 2013 were $7.32 billion, $297 million or 4%

lower than in 2012. The declines in both years reflected reductions in net written premiums over the preceding twelve months.

Net Investment Income

Net investment income in 2014 was $379 million, $10 million or 3% higher than in 2013. Net investment income in 2013 was $369 million,

$35 million or 9% lower than in 2012. Refer to the "Net Investment Income" section of "Consolidated Results of Operations" herein for a discussion

of the changes in the Company's net investment income in 2014 and 2013 as compared with the respective prior year. In addition, refer to note 2 of

notes to the Company's consolidated financial statements herein for a discussion of the Company's net investment income allocation methodology.

Other Revenues

Other revenues in all years presented primarily consisted of installment premium charges. Other revenues in 2013 also included a $20 million

gain from the sale of renewal rights related to the Company's National Flood Insurance Program (NFIP) business. The Company was a participant in

the NFIP Write Your Own Program administered by the Federal Emergency Management Agency (FEMA) and the Federal Insurance & Mitigation

Administration.

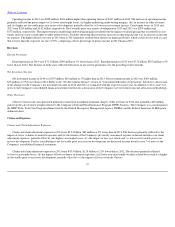

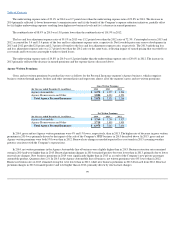

Claims and Expenses

Claims and Claim Adjustment Expenses

Claims and claim adjustment expenses in 2014 were $4.24 billion, $83 million or 2% lower than in 2013. The decrease primarily reflected (i) the

impact of lower volumes of insured exposures and (ii) the benefit of the Company's previously announced expense reduction initiatives on claim

adjustment expenses, partially offset by (iii) higher catastrophe losses, (iv) the impact of loss cost trends and (v) lower net favorable prior year

reserve development. Factors contributing to net favorable prior year reserve development are discussed in more detail in note 7 of notes to the

Company's consolidated financial statements.

Claims and claim adjustment expenses in 2013 were $4.33 billion, $1.18 billion or 21% lower than in 2012. The decrease primarily reflected

(i) lower catastrophe losses, (ii) the impact of lower volumes of insured exposures, (iii) lower non

-

catastrophe weather

-

related losses and (iv) higher

net favorable prior year reserve development, partially offset by (v) the impact of loss cost trends. Factors

97