Travelers 2014 Annual Report Download - page 123

Download and view the complete annual report

Please find page 123 of the 2014 Travelers annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

|

|

Table of Contents

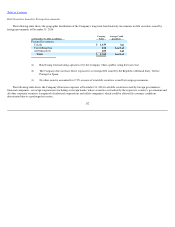

need for state regulatory approval for changes to personal property and casualty insurance prices, as well as competitive market conditions, may

impact the timing and extent of renewal premium changes.

Property and casualty insurance market conditions are expected to remain competitive during 2015 for new business, not only in Business and

International Insurance and Bond & Specialty Insurance, but especially in Personal Insurance, where price comparison technology used by agents

and brokers, sometimes referred to as "comparative raters," has facilitated the process of generating multiple quotes, thereby increasing price

comparison on new business and, increasingly, on renewal business. The Company anticipates that its new Quantum Auto 2.0 product in the

Personal Insurance segment's Agency Automobile line of business, as discussed below, will continue to increase new business premiums during

2015. The Company also anticipates that, as a result of strong business retentions and increases in new business, policies in force in the Personal

Insurance segment's Agency Automobile line of business will continue to increase in 2015. In each of the Company's business segments, new

business generally has less of an impact on underwriting profitability than renewal business. However, in periods of meaningful increases in new

business, the impact of a higher mix of new business versus renewal business may negatively impact underwriting profitability.

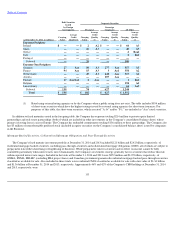

In recent years, the federal government, particularly the Federal Reserve, has taken extraordinary steps to stabilize financial markets, encourage

economic growth and keep interest rates low. During this time, the United States has experienced a slow rate of economic growth. Even if economic

growth continues in the United States, or other regions in which we do business, it may be at a slow or slower rate for an extended period of time.

Further, general uncertainty regarding a variety of domestic and international matters, such as the U.S. Federal budget and taxes, implementation of

the Affordable Care Act, the regulatory environment and geopolitical instability in various parts of the world, has added to the uncertainty

regarding economic conditions generally. If economic conditions deteriorate, the resulting low levels of economic activity could impact exposure

changes at renewal and the Company's ability to write business at acceptable rates. Additionally, low levels of economic activity could adversely

impact audit premium adjustments, policy endorsements and mid

-

term cancellations after policies are written. All of the foregoing, in turn, could

adversely impact net written premiums during 2015, and because earned premiums are a function of net written premiums, earned premiums could

be adversely impacted in 2015.

Underwriting Gain/Loss. The Company's underwriting gain/loss can be significantly impacted by catastrophe losses and net favorable or

unfavorable prior year reserve development, as well as underlying underwriting margins.

Catastrophe and other weather

-

related losses are inherently unpredictable from period to period. The Company experienced significant

catastrophe and other weather

-

related losses in a number of recent periods, which adversely impacted its results of operations. The Company's

results of operations could be adversely impacted if significant catastrophe and other weather

-

related losses were to occur during 2015.

For the last several years, the Company's results have included significant amounts of net favorable prior year reserve development, although

at lower levels in some recent periods, driven by better than expected loss experience in all of the Company's segments. The lower level of net

favorable prior year reserve development in a number of recent periods may have been in part due to the Company's reserve estimation process

incorporating those factors that led to the higher levels of net favorable prior year reserve development in previous years. If that trend continues,

the better than expected loss experience may continue at these recent lower levels, or even lower levels. However, given the inherent uncertainty in

estimating claims and claim adjustment expense reserves, loss experience could develop such that the Company recognizes higher or lower levels

of favorable prior year reserve development, no favorable prior year reserve development or unfavorable prior year reserve development in future

periods. In addition, the ongoing review of prior year claims and claim adjustment expense reserves, or

122