Travelers 2014 Annual Report Download - page 97

Download and view the complete annual report

Please find page 97 of the 2014 Travelers annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

|

|

Table of Contents

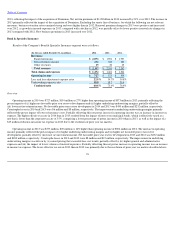

Net written premiums in 2014 were $2.10 billion, $73 million or 4% higher than in 2013, primarily driven by lower reinsurance costs that resulted

from the Company's decision to eliminate a management liability excess

-

of

-

loss reinsurance treaty and higher contract surety premium volume.

Excluding the surety line of business, for which the following are not relevant measures, business retention rates in 2014 remained strong and were

slightly higher than in 2013. Renewal premium changes in 2014 remained positive, although lower than in 2013, driven by renewal rate changes. New

business premiums in 2014 decreased from 2013.

Net written premiums in 2013 were $2.03 billion, $106 million or 6% higher than in 2012, primarily driven by higher contract surety volume, rate

increases in the management liability business and lower reinsurance costs primarily resulting from a change in a reinsurance treaty. Excluding the

surety line of business, for which the following are not relevant measures, business retention rates in 2013 remained strong but were lower than in

2012. Renewal premium changes in 2013 remained positive and were higher than in 2012, as increases in renewal rate changes were largely offset by

a decline in insured exposures. Renewal rate changes exceeded expected loss cost trends in 2013. New business premiums in 2013 decreased from

2012.

Personal Insurance

Results of the Company's Personal Insurance segment were as follows:

Overview

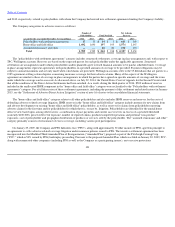

Operating income in 2014 was $824 million, $14 million or 2% lower than operating income of $838 million in 2013. The decrease in operating

income primarily reflected the pretax impacts of (i) an increase in catastrophe losses, (ii) lower net favorable prior year reserve development and

(iii) a decline in other revenues, partially offset by (iv) higher underlying underwriting margins and (v) higher net investment income. Catastrophe

losses in 2014 and 2013 were $336 million and $250 million, respectively. Net favorable prior year reserve development in 2014 and 2013 was

$169 million and $209 million, respectively. The improvement in underlying underwriting margins primarily reflected (i) earned pricing that exceeded

loss cost trends and (ii) the benefit of the Company's previously announced expense reduction initiatives, partially offset by (iii) the impact of a

higher mix of new business versus renewal business. Income tax expense in 2014 was level with 2013. The higher effective tax rate in 2014 than in

2013 primarily resulted from the impact of a $5 million reduction in income tax expense in 2013 due to the resolution of prior year tax matters.

96

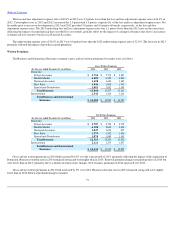

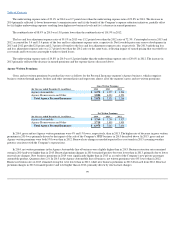

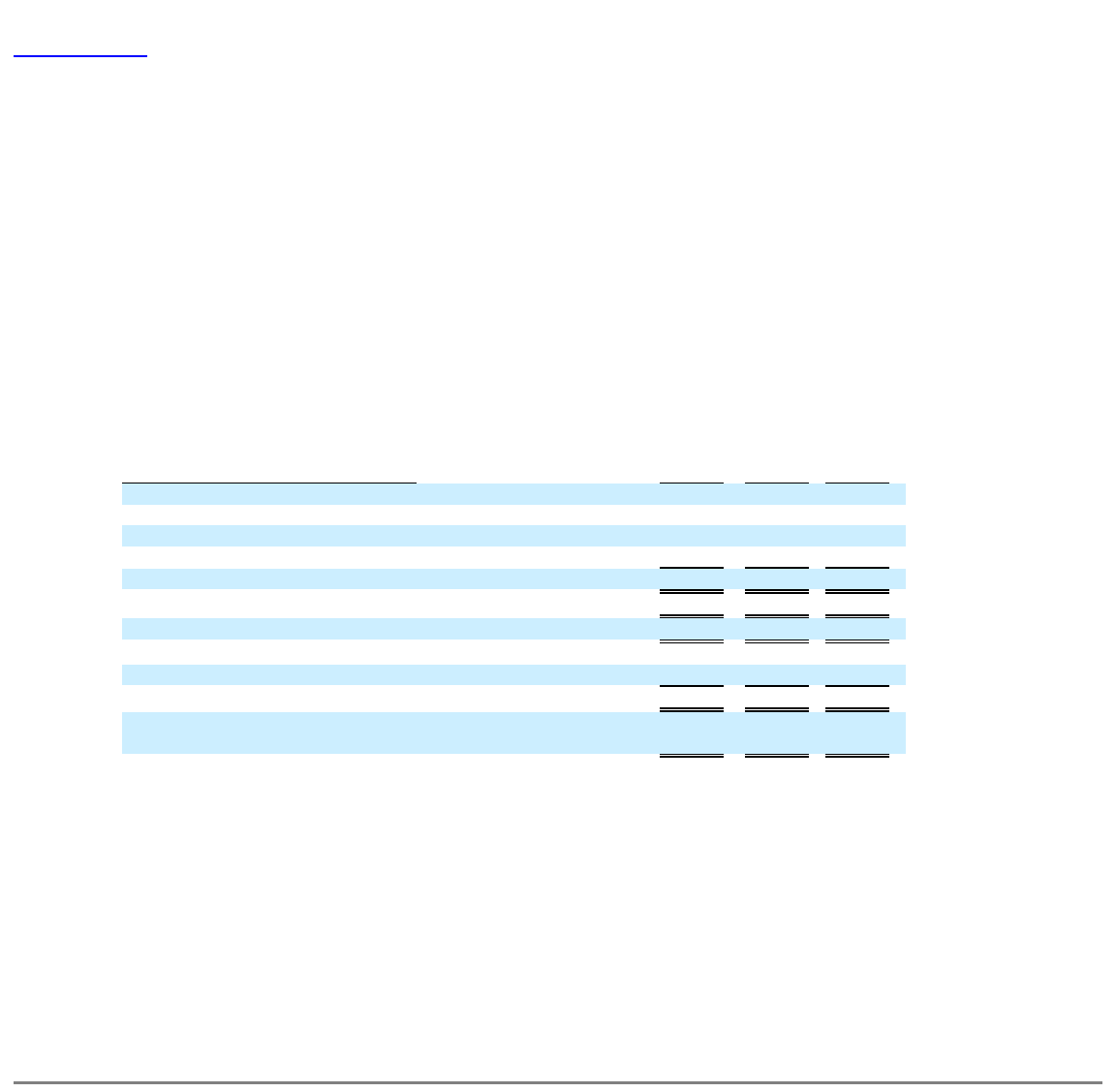

(for the year ended December 31, in millions)

2014

2013

2012

Revenues:

Earned premiums

$

7,125

$

7,324

$

7,621

Net investment income

379

369

404

Other revenues

80

103

66

Total revenues

$

7,584

$

7,796

$

8,091

Total claims and expenses

$

6,394

$

6,592

$

7,842

Operating income

$

824

$

838

$

217

Loss and loss adjustment expense ratio

59.6

%

59.1

%

72.3

%

Underwriting expense ratio

29.1

29.8

29.6

Combined ratio

88.7

%

88.9

%

101.9

%

Incremental impact of direct to consumer initiative on combined

ratio

1.7

%

1.8

%

2.3

%