Travelers 2014 Annual Report Download - page 120

Download and view the complete annual report

Please find page 120 of the 2014 Travelers annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

|

|

Table of Contents

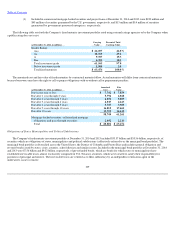

reductions in arctic sea ice may contribute to rising sea levels that could impact flooding in coastal areas. Accordingly, the Company may be

subject to increased losses from catastrophes and other weather

-

related events. Additionally, the Company's catastrophe models may be less

reliable due to the increased unpredictability, frequency and severity of severe weather events or a delay in the recognition of recent changes in

climate conditions.

The Company discusses how potentially changing climate conditions may present other issues for its business under "Risk Factors" in

Item 1A of this report and under "—Outlook" herein. For example, among other things:

•

Increasingly unpredictable and severe weather conditions could result in increased frequency and severity of claims under policies

issued by the Company. See "Risk Factors—Catastrophe losses could materially and adversely affect our results of operations, our

financial position and/or liquidity, and could adversely impact our ratings, our ability to raise capital and the availability and cost of

reinsurance" and "—Outlook—Underwriting Gain/Loss."

•

Changing climate conditions could also impact the creditworthiness of issuers of securities in which the Company invests. For

example, water supply adequacy could impact the creditworthiness of bond issuers in the Southwestern United States, and more

frequent and/or severe hurricanes could impact the creditworthiness of issuers in the Southeastern United States, among other

areas. See "Risk Factors—Our investment portfolio may suffer reduced returns or material realized or unrealized losses."

•

Increased regulation adopted in response to potential changes in climate conditions may impact the Company and its customers.

For example, state insurance regulation could impact the Company's ability to manage property exposures in areas vulnerable to

significant climate driven losses. If the Company is unable to implement risk based pricing, modify policy terms or reduce exposures

to the extent necessary to address rising losses related to catastrophes and smaller scale weather events (should those increased

losses occur), its business may be adversely affected. See "Risk Factors—Catastrophe losses could materially and adversely affect

our results of operations, our financial position and/or liquidity, and could adversely impact our ratings, our ability to raise capital

and the availability and cost of reinsurance."

•

The full range of potential liability exposures related to climate change continues to evolve. Through the Company's Emerging

Issues Committee and its Committee on Climate, Energy and the Environment, the Company works with its business units and

corporate groups, as appropriate, to identify and try to assess climate change

-

related liability issues, which are continually evolving

and often hard to fully evaluate. See "Risk Factors—The effects of emerging claim and coverage issues on our business are

uncertain."

Climate change regulation also could increase the Company's customers' costs of doing business. For example, insureds faced with carbon

management regulatory requirements may have less available capital for investment in loss prevention and safety features which may, over time,

increase loss exposures. Also, increased regulation may result in reduced economic activity, which would decrease the amount of insurable assets

and businesses.

The Company regularly reviews emerging issues, such as changing climate conditions, to consider potential changes to its modeling and the

use of such modeling, as well as to help determine the need for new underwriting strategies, coverage modifications or new products.

REINSURANCE RECOVERABLES

The Company reinsures a portion of the risks it underwrites in order to control its exposure to losses. For additional discussion regarding the

Company's reinsurance coverage, see "Part I—

Item 1

—Reinsurance."

119