Travelers 2014 Annual Report Download - page 208

Download and view the complete annual report

Please find page 208 of the 2014 Travelers annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

198 -

199

199 -

200

200 -

201

201 -

202

202 -

203

203 -

204

204 -

205

205 -

206

206 -

207

207 -

208

208 -

209

209 -

210

210 -

211

211 -

212

212 -

213

213 -

214

214 -

215

215 -

216

216 -

217

217 -

218

218 -

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

|

|

Table of Contents

THE TRAVELERS COMPANIES, INC. AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS (Continued)

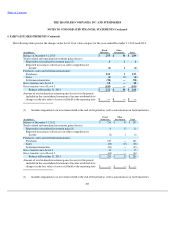

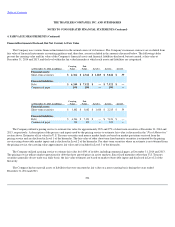

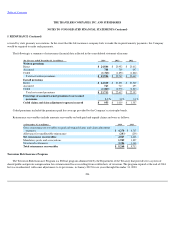

5. REINSURANCE (Continued)

In order for a loss to be covered under the program (subject losses), the loss must meet certain aggregate industry loss minimums and must be

the result of an event that is certified as an act of terrorism by the U.S. Secretary of the Treasury, in consultation with the Secretary of Homeland

Security and the Attorney General of the United States. The annual aggregate industry loss minimum under the reauthorized program is initially

$100 million for 2015, but will increase over the six

-

year life of the program to $200 million by December 31, 2020. The program excludes from

participation the following types of insurance: Federal crop insurance, private mortgage insurance, financial guaranty insurance, medical

malpractice insurance, health or life insurance, flood insurance, reinsurance, commercial automobile, professional liability (other than directors and

officers'), surety, burglary and theft, and farm

-

owners multi

-

peril. In the case of a war declared by Congress, only workers' compensation losses are

covered by the program. All commercial property and casualty insurers licensed in the United States are generally required to participate in the

program. Under the reauthorized program, a participating insurer, in exchange for making terrorism insurance available, is initially entitled to be

reimbursed by the Federal Government for 85% of subject losses, after an insurer deductible, subject to an annual cap. This reimbursement

percentage will decrease over the six

-

year life of the program to 80% of subject losses by December 31, 2020.

The deductible for any calendar year is equal to 20% of the insurer's direct earned premiums for covered lines for the preceding calendar year.

The Company's estimated deductible under the program is $2.38 billion for 2015. The annual cap limits the amount of aggregate subject losses for

all participating insurers to $100 billion. Once subject losses have reached the $100 billion aggregate during a program year, participating insurers

will not be liable under the program for additional covered terrorism losses for that program year. There have been no terrorism

-

related losses that

have triggered program coverage since the program was established. Since the law is untested, there is substantial uncertainty as to how it will be

applied if an act of terrorism is certified under the program. It is also possible that future legislative action could change or eliminate the program.

Further, given the unpredictable frequency and severity of terrorism losses, as well as the limited terrorism coverage in the Company's own

reinsurance program, future losses from acts of terrorism, particularly involving nuclear, biological, chemical or radiological events, could be

material to the Company's operating results, financial position and/or liquidity in future periods. In addition, the Company may not have sufficient

resources to respond to claims arising from a high frequency of high severity natural catastrophes and/or of man

-

made catastrophic events

involving conventional means. While the Company seeks to manage its exposure to man

-

made catastrophic events involving conventional means,

the Company may not have sufficient resources to respond to claims arising out of one or more man

-

made catastrophic events involving nuclear,

biological, chemical or radiological means.

207