Travelers 2014 Annual Report Download - page 144

Download and view the complete annual report

Please find page 144 of the 2014 Travelers annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

148 -

149

149 -

150

150 -

151

151 -

152

152 -

153

153 -

154

154 -

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

|

|

Table of Contents

•

Changes in settlement patterns

General liability book of business risk factors

•

Changes in policy provisions (e.g., deductibles, policy limits, endorsements)

•

Changes in underwriting standards

•

Product mix (e.g., size of account, industries insured, jurisdiction mix)

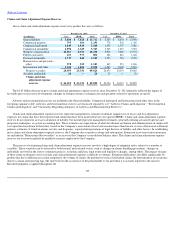

Unanticipated changes in risk factors can affect reserves. As an indicator of the causal effect that a change in one or more risk factors could

have on reserves for general liability (excluding asbestos and environmental), a 1% increase (decrease) in incremental paid loss development for

each future calendar year could result in a 1.5% increase (decrease) in claims and claim adjustment expense reserves.

Historically, the one

-

year change in the reserve estimate for this product line, excluding estimated asbestos and environmental amounts, over

the last nine years has varied from –8% to 2% (averaging –4%) for the Company, and from –5% to 2% (averaging –3%) for the industry overall. The

Company's year

-

to

-

year changes are driven by, and are based on, observed events during the year. The Company believes that its range of

historical outcomes is illustrative of reasonably possible one

-

year changes in reserve estimates for this product line. General liability reserves

(excluding asbestos and environmental) represent approximately 23% of the Company's total claims and claim adjustment expense reserves.

The Company's change in reserve estimate for this product line, excluding estimated asbestos and environmental amounts, was –

5% for 2014,

–4% for 2013 and –3% for 2012. The 2014 change was primarily concentrated in excess coverages for accident years 2008 through 2012, reflecting

more favorable legal and judicial environments than what the Company previously expected. The 2013 change was primarily concentrated in excess

coverages for accident years 2010 and prior, reflecting more favorable legal and judicial environments than what the Company previously expected.

The 2012 change was primarily concentrated in excess coverages for accident years 2009 and prior, reflecting more favorable legal and judicial

environments than what the Company previously expected. Also contributing to the 2012 change was better than expected results for management

liability business, primarily for the errors & omissions and fiduciary products for accident years 2007 and prior.

Commercial Property

Commercial property is generally considered a short tail line with a simpler and faster claim reporting and adjustment process than liability

coverages, and less uncertainty in the reserve setting process (except for more complex business interruption claims). It is generally viewed as a

moderate frequency, low to moderate severity line, except for catastrophes and coverage related to large properties. The claim reporting and

settlement process for property coverage claim reserves is generally restricted to the insured and the insurer. Overall, the claim liabilities for this

line create a low estimation risk, except possibly for catastrophes and business interruption claims.

Commercial property reserves are typically analyzed in two components, one for catastrophic or other large single events, and another for all

other events. Examples of common risk factors, or perceptions thereof, that could change and, thus, affect the required property reserves (beyond

those included in the general discussion section) include:

Commercial property risk factors

•

Physical concentration of policyholders

•

Availability and cost of local contractors

143