Travelers 2014 Annual Report Download - page 100

Download and view the complete annual report

Please find page 100 of the 2014 Travelers annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

|

|

Table of Contents

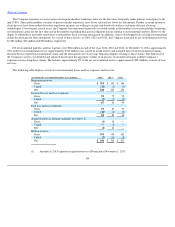

The underwriting expense ratio of 29.1% in 2014 was 0.7 points lower than the underwriting expense ratio of 29.8% in 2013. The decrease in

2014 primarily reflected (i) lower homeowners' commission rates and (ii) the benefit of the Company's expense reduction initiatives, partially offset

by (iii) higher underwriting expenses resulting from higher new business levels and (iv) a decrease in earned premiums.

The combined ratio of 88.9% in 2013 was 13.0 points lower than the combined ratio of 101.9% in 2012.

The loss and loss adjustment expense ratio of 59.1% in 2013 was 13.2 points lower than the 2012 ratio of 72.3%. Catastrophe losses in 2013 and

2012 accounted for 3.4 and 13.4 points of the loss and loss adjustment expense ratio, respectively. Net favorable prior year reserve development in

2013 and 2012 provided 2.8 points and 2.3 points of benefit to the loss and loss adjustment expense ratio, respectively. The 2013 underlying loss

and loss adjustment expense ratio was 2.7 points lower than the 2012 ratio on the same basis, reflecting impact of earned pricing that exceeded loss

cost trends and lower non

-

catastrophe weather

-

related losses.

The underwriting expense ratio of 29.8% in 2013 was 0.2 points higher than the underwriting expense ratio of 29.6% in 2012. The increase in

2013 primarily reflected the decrease in earned premiums and the expense factors discussed above.

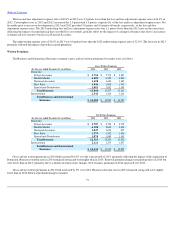

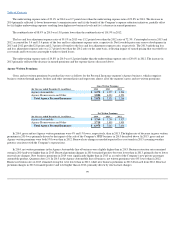

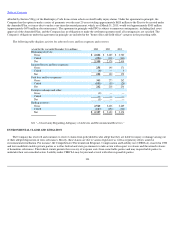

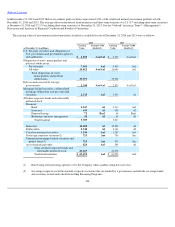

Agency Written Premiums

Gross and net written premiums by product line were as follows for the Personal Insurance segment's Agency business, which comprises

business written through agents, brokers and other intermediaries and represents almost all of the segment's gross and net written premiums:

In 2014, gross and net Agency written premiums were 4% and 1% lower, respectively, than in 2013. The higher rate of decrease in gross written

premiums in 2014 was primarily driven by the impact of the sale of the Company's NFIP business in 2013 described above. In 2013, gross and net

Agency written premiums were both 5% lower than in 2012. Renewal rate changes exceeded expected loss cost trends in 2013 assuming weather

patterns consistent with the Company's expectations.

In 2014, net written premiums in the Agency Automobile line of business were slightly higher than in 2013. Business retention rates remained

strong in 2014 and were higher than in 2013. Renewal premium changes in 2014 remained positive but were lower than in 2013, primarily due to lower

renewal rate changes. New business premiums in 2014 were significantly higher than in 2013 as a result of the Company's new private passenger

automobile product, Quantum Auto 2.0. In 2013 in the Agency Automobile line of business, net written premiums were 8% lower than in 2012.

Business retention rates in 2013 remained strong but were lower than in 2012, while new business premiums in 2013 decreased from 2012. Renewal

premium changes in 2013 remained positive and were higher than in 2012, primarily driven by renewal rate changes.

99

Gross Written Premiums

(for the year ended December 31, in millions)

2014

2013

2012

Agency Automobile

$

3,278

$

3,277

$

3,544

Agency Homeowners and Other

3,800

4,094

4,220

Total Agency Personal Insurance

$

7,078

$

7,371

$

7,764

Net Written Premiums

(for the year ended December 31, in millions)

2014

2013

2012

Agency Automobile

$

3,260

$

3,258

$

3,527

Agency Homeowners and Other

3,718

3,805

3,909

Total Agency Personal Insurance

$

6,978

$

7,063

$

7,436