Travelers 2014 Annual Report Download - page 118

Download and view the complete annual report

Please find page 118 of the 2014 Travelers annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

|

|

Table of Contents

achieve its primary investment goals of assuring the Company's ability to meet policyholder obligations as well as to optimize investment returns,

given these obligations.

CATASTROPHE MODELING

The Company uses various analyses and methods, including proprietary and third

-

party computer modeling processes, to analyze

catastrophic events and the risks associated with them. The Company uses these analyses and methods to make underwriting and reinsurance

decisions designed to manage its exposure to catastrophic events. There are no industry

-

standard methodologies or assumptions for projecting

catastrophe exposure. Accordingly, catastrophe estimates provided by different insurers may not be comparable.

The Company actively monitors and evaluates changes in third

-

party models and, when necessary, calibrates the catastrophe risk model

estimates delivered via its own proprietary modeling processes. The Company considers historical loss experience, recent events, underwriting

practices, market share analyses, external scientific analysis and various other factors to account for non

-

modeled losses to refine its proprietary

view of catastrophe risk. These proprietary models are continually updated as new information emerges.

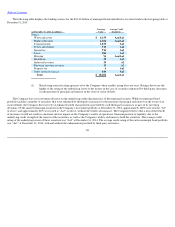

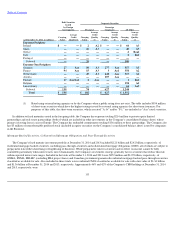

The tables below set forth the probabilities that estimated losses, comprising claims and allocated claim adjustment expenses (but excluding

unallocated claim adjustment expenses), from a single event occurring in a one

-

year timeframe will equal or exceed the indicated loss amounts

(expressed in dollars and as a percentage of the Company's common equity), based on the current version of the proprietary and third

-

party

computer models utilized by the Company at December 31, 2014. For example, on the basis described below the tables, the Company estimates that

there is a one percent chance that the Company's loss from a single U.S. hurricane in a one

-

year timeframe would equal or exceed $1.3 billion, or 6%

of the Company's common equity at December 31, 2014.

117

Dollars (in billions)

Likelihood of Exceedance(1)

Single U.S.

Hurricane

Single U.S.

and Canadian

Earthquake

2.0% (1

-

in

-

50)

$

1.0

$

0.5

1.0% (1

-

in

-

100)

$

1.3

$

0.6

0.4% (1

-

in

-

250)

$

1.9

$

0.9

0.1% (1

-

in

-

1,000)

$

3.6

$

1.5

Percentage of

Common Equity(2)

Likelihood of Exceedance

Single U.S.

Hurricane

Single U.S.

and Canadian

Earthquake

2.0% (1

-

in

-

50)

5

%

2

%

1.0% (1

-

in

-

100)

6

%

2

%

0.4% (1

-

in

-

250)

8

%

4

%

0.1% (1

-

in

-

1,000)

16

%

7

%

(1)

An event that has, for example, a 2% likelihood of exceedance is sometimes described as a "1

-

in

-

50 year event." As

noted above, however, the probabilities in the table represent the likelihood of losses from a single event equaling or

exceeding the indicated threshold loss amount in a one

-

year timeframe, not over a multi

-

year timeframe. Also, because

the probabilities relate to a single event, the probabilities do not address the likelihood of more than one event

occurring in a particular period, and, therefore, the amounts do not address potential aggregate catastrophe losses

occurring in a one

-

year timeframe.