Travelers 2014 Annual Report Download - page 47

Download and view the complete annual report

Please find page 47 of the 2014 Travelers annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

|

|

Table of Contents

46

A given accident year's cumulative losses are then projected to ultimate by multiplying

current cumulative losses by successive age

-

to

-

age link ratios up to that future age where

growth is expected to end. For example, if growth is expected to end at 60 months, then the

ultimate indication for an accident year with cumulative losses at 12 months equals those

losses times a 12 to 24 month link ratio, times a 24 to 36 month link ratio, times a

36 to 48 month link ratio, times a 48 to 60 month link ratio.

Advanced applications of the method include adjustments for changing conditions during

the historical period and anticipated changes in the future.

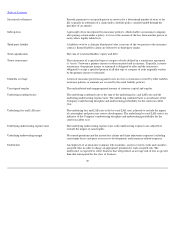

Pool

An organization of insurers or reinsurers through which particular types of risks are

underwritten with premiums, losses and expenses being shared in agreed

-

upon percentages.

Premiums

The amount charged during the year on policies and contracts issued, renewed or reinsured

by an insurance company.

Property insurance

Insurance that provides coverage to a person or business with an insurable interest in

tangible property for that person's or business's property loss, damage or loss of use.

Quota share reinsurance

Reinsurance wherein the insurer cedes an agreed

-

upon fixed percentage of liabilities,

premiums and losses for each policy covered on a pro rata basis.

Rates

Amounts charged per unit of insurance.

Redundancy

With regard to reserves for a given liability, a redundancy exists when it is estimated or

determined that the reserves are greater than what will be needed to pay the ultimate

settlement value of the related liabilities. Where the redundancy is the result of an estimate,

the estimated amount of redundancy (or even the finding of whether or not a redundancy

exists) may change as new information becomes available.

Reinstatement premiums

Additional premiums payable to reinsurers to restore coverage limits that have been

exhausted as a result of reinsured losses under certain excess

-

of

-

loss reinsurance treaties.

Reinsurance

The practice whereby one insurer, called the reinsurer, in consideration of a premium paid to

that insurer, agrees to indemnify another insurer, called the ceding company, for part or all of

the liability of the ceding company under one or more policies or contracts of insurance

which it has issued.

Reinsurance agreement

A contract specifying the terms of a reinsurance transaction.

Renewal premium change

The estimated change in average premium on policies that renew, including rate and

exposure changes. Such statistics are subject to change based on a number of factors,

including changes in actuarial estimates.