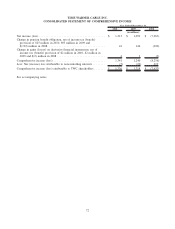

Time Warner Cable 2010 Annual Report Download - page 86

Download and view the complete annual report

Please find page 86 of the 2010 Time Warner Cable annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

|

|

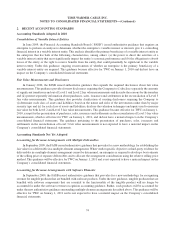

2. RECENT ACCOUNTING STANDARDS

Accounting Standards Adopted in 2010

Consolidation of Variable Interest Entities

In June 2009, the Financial Accounting Standards Board (“FASB”) issued authoritative guidance that requires an

enterprise to perform an analysis to determine whether the enterprise’s variable interest or interests give it a controlling

financial interest in a variable interest entity. This analysis identifies the primary beneficiary of a variable interest entity as

the enterprise that has both of the following characteristics, among others: (a) the power to direct the activities of a

variable interest entity that most significantly impact the entity’s economic performance and (b) the obligation to absorb

losses of the entity, or the right to receive benefits from the entity, that could potentially be significant to the variable

interest entity. Under this guidance, ongoing reassessments of whether an enterprise is the primary beneficiary of a

variable interest entity are required. This guidance became effective for TWC on January 1, 2010 and did not have an

impact on the Company’s consolidated financial statements.

Fair Value Measurements and Disclosures

In January 2010, the FASB issued authoritative guidance that expands the required disclosures about fair value

measurements. This guidance provides for new disclosures requiring the Company to (i) disclose separately the amounts

of significant transfers in and out of Level 1 and Level 2 fair value measurements and describe the reasons for the transfers

and (ii) present separately information about purchases, sales, issuances and settlements in the reconciliation of Level 3

fair value measurements. This guidance also provides clarification of existing disclosures requiring the Company to

(i) determine each class of assets and liabilities based on the nature and risks of the investments rather than by major

security type and (ii) for each class of assets and liabilities, disclose the valuation techniques and inputs used to measure

fair value for both Level 2 and Level 3 fair value measurements. This guidance became effective for TWC on January 1,

2010, except for the presentation of purchases, sales, issuances and settlements in the reconciliation of Level 3 fair value

measurements, which is effective for TWC on January 1, 2011, and did not have a material impact on the Company’s

consolidated financial statements. The guidance pertaining to the presentation of purchases, sales, issuances and

settlements in the reconciliation of Level 3 fair value measurements is not expected to have a material impact on the

Company’s consolidated financial statements.

Accounting Standards Not Yet Adopted

Accounting for Revenue Arrangements with Multiple Deliverables

In September 2009, the FASB issued authoritative guidance that provides for a new methodology for establishing the

fair value for a deliverable in a multiple-element arrangement. When vendor specific objective or third-party evidence for

deliverables in a multiple-element arrangement cannot be determined, an enterprise is required to develop a best estimate

of the selling price of separate deliverables and to allocate the arrangement consideration using the relative selling price

method. This guidance will be effective for TWC on January 1, 2011 and is not expected to have a material impact on the

Company’s consolidated financial statements.

Accounting for Revenue Arrangements with Software Elements

In September 2009, the FASB issued authoritative guidance that provides for a new methodology for recognizing

revenue for tangible products that are bundled with software products. Under the new guidance, tangible products that are

bundled with software components that are essential to the functionality of the tangible product will no longer be

accounted for under the software revenue recognition accounting guidance. Rather, such products will be accounted for

under the new authoritative guidance surrounding multiple-element arrangements described above. This guidance will be

effective for TWC on January 1, 2011 and is not expected to have a material impact on the Company’s consolidated

financial statements.

74

TIME WARNER CABLE INC.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS—(Continued)