Time Warner Cable 2010 Annual Report Download - page 72

Download and view the complete annual report

Please find page 72 of the 2010 Time Warner Cable annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

|

|

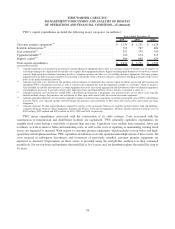

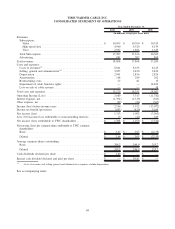

Free Cash Flow increased from $1.739 billion in 2008 to $1.917 billion in 2009, primarily as a result of a decrease in

capital expenditures, partially offset by a decrease in cash provided by operating activities, as discussed above.

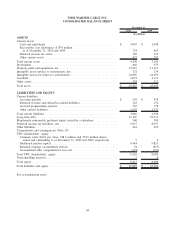

Outstanding Debt and Mandatorily Redeemable Preferred Equity and Available Financial Capacity

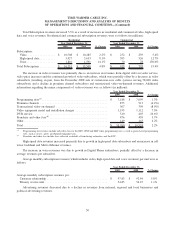

Debt and mandatorily redeemable preferred equity as of December 31, 2010 and 2009 were as follows:

Maturity

Interest

Rate 2010 2009

Outstanding Balance as of

December 31,

(in millions)

TWC notes and debentures .............................. 2012-2040 6.059%

(a)

$ 20,418 $ 18,357

TWE notes and debentures

(b)

............................. 2012-2033 7.530%

(a)

2,700 2,702

Revolving credit facility

(c)

............................... 2013 — —

Commercial paper program

(d)

............................ 2013 — 1,261

Capital leases and other ................................. 3 11

Total debt ........................................... 23,121 22,331

TW NY Cable Preferred Membership Units .................. 2013 8.210% 300 300

Total debt and mandatorily redeemable preferred equity ......... $ 23,421 $ 22,631

(a)

Rate represents a weighted-average effective interest rate as of December 31, 2010 and includes the effects of interest rate swap contracts.

(b)

Outstanding balance of TWE notes and debentures as of December 31, 2010 and 2009 includes an unamortized fair value adjustment of

$91 million and $102 million, respectively, which includes the fair value adjustment recognized as a result of the 2001 merger of America Online,

Inc. (now known as AOL Inc.) and Time Warner Inc. (now known as Historic TW Inc.). TWE is a consolidated subsidiary of the Company.

(c)

TWC’s unused committed financial capacity was $6.891 billion as of December 31, 2010, reflecting $3.047 billion of cash and equivalents and

$3.844 billion of available borrowing capacity under the $4.0 billion Revolving Credit Facility (which reflects a reduction of $156 million for

outstanding letters of credit backed by the $4.0 billion Revolving Credit Facility).

(d)

Outstanding balance as of December 31, 2009 excludes an unamortized discount on commercial paper of $1 million (none as of December 31,

2010).

See “Overview—Recent Developments—2010 Bond Offering and $4.0 Billion Revolving Credit Facility” and

Notes 9 and 10 to the accompanying consolidated financial statements for further details regarding the Company’s

outstanding debt and mandatorily redeemable preferred equity and other financing arrangements, including certain

information about maturities, covenants and rating triggers related to such debt and financing arrangements. At

December 31, 2010, TWC was in compliance with the leverage ratio covenant of the $4.0 billion Revolving Credit

Facility, with a ratio of consolidated total debt as of December 31, 2010 to consolidated EBITDA for 2010 of

approximately 2.9 times. In accordance with the $4.0 billion Revolving Credit Facility agreement, consolidated total

debt as of December 31, 2010 was calculated as (a) total debt per the accompanying consolidated balance sheet less the

TWE unamortized fair value adjustment (discussed above) and the fair value of debt subject to interest rate swap

contracts, less (b) total cash per the accompanying consolidated balance sheet in excess of $25 million. In accordance with

the $4.0 billion Revolving Credit Facility agreement, consolidated EBITDA for 2010 was calculated as OIBDA plus

equity-based compensation expense.

Contractual and Other Obligations

Contractual Obligations

The Company has obligations to make future payments for goods and services under certain contractual

arrangements. These contractual obligations secure the future rights to various assets and services to be used in the

normal course of the Company’s operations. For example, the Company is contractually committed to make certain

minimum lease payments for the use of property under operating lease agreements. In accordance with applicable

accounting rules, the future rights and obligations pertaining to firm commitments, such as operating lease obligations and

certain purchase obligations under contracts, are not reflected as assets or liabilities in the accompanying consolidated

balance sheet.

60

TIME WARNER CABLE INC.

MANAGEMENT’S DISCUSSION AND ANALYSIS OF RESULTS

OF OPERATIONS AND FINANCIAL CONDITION—(Continued)