MoneyGram 2005 Annual Report Download - page 86

Download and view the complete annual report

Please find page 86 of the 2005 MoneyGram annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

|

|

Table of Contents

MONEYGRAM INTERNATIONAL, INC. AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS — (Continued)

Supplemental Executive Retirement Plan (SERP) — In connection with the spin-off, the Company assumed responsibility for all but a portion of the Viad

SERP. Viad retained the benefit obligation related to two of its subsidiaries, which represented 13 percent of Viad's benefit obligation at December 31, 2003.

Another SERP, the MoneyGram International, Inc. SERP, is a nonqualified defined benefit pension plan, which provides postretirement income to eligible

employees selected by the Board of Directors. It is our policy to fund the supplemental executive retirement plan as benefits are paid.

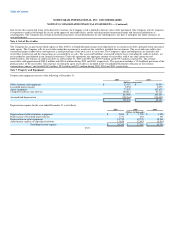

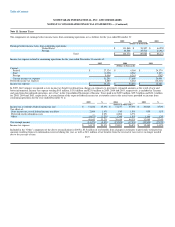

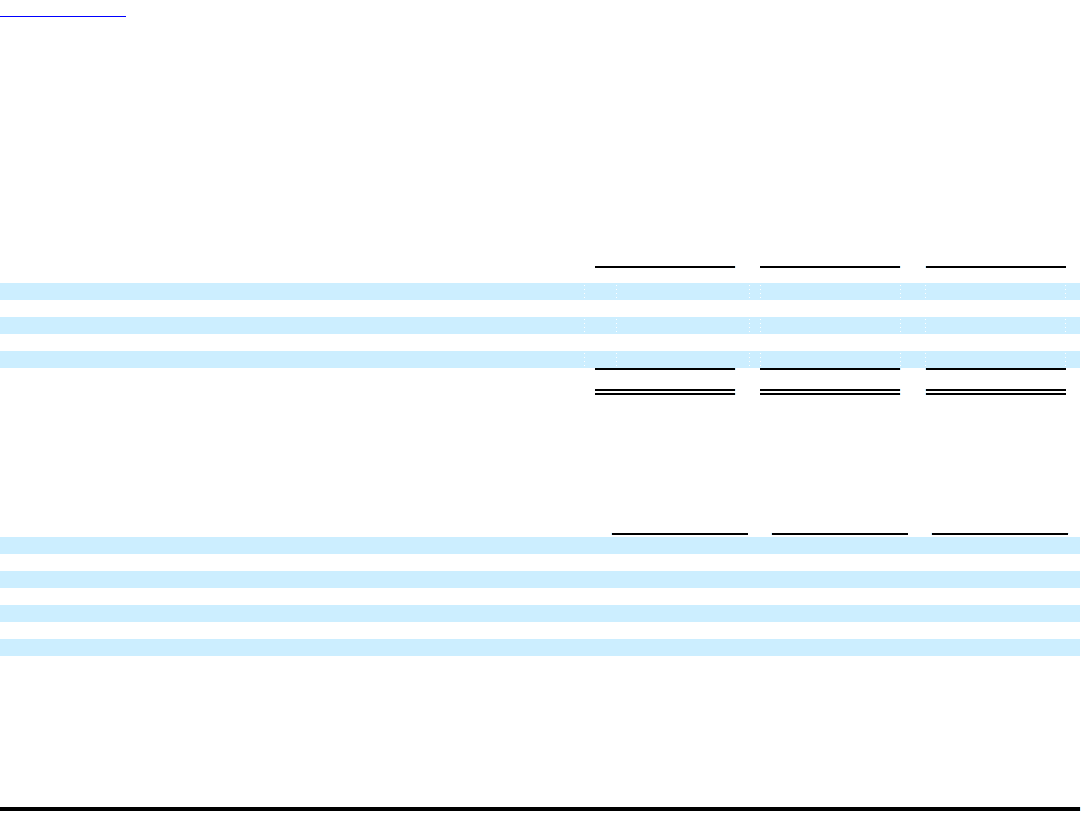

Net periodic pension cost for the defined benefit pension plan and combined SERPs includes the following components for the year ended December 31:

2005 2004 2003

(Dollars in thousands)

Service cost $ 1,893 $ 1,717 $ 2,912

Interest cost 11,320 11,333 11,260

Expected return on plan assets (8,604) (8,804) (9,627)

Amortization of prior service cost 714 768 516

Recognized net actuarial loss 4,092 3,990 1,854

Net periodic pension cost $ 9,415 $ 9,004 $ 6,915

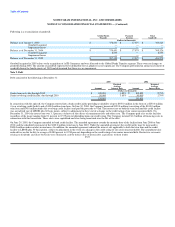

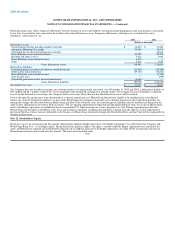

Benefits expected to be paid through the defined benefit pension plan and combined SERPS are $12.4 million, $12.5 million, $12.6 million, $13.0 million,

$13.1 million and $67.7 million for 2006, 2007, 2008, 2009, 2010 and for the combined five years starting 2011, respectively. Contributions to the defined

benefit pension plan and combined SERPS are expected to be $13.5 million in 2006.

The actuarial valuation date for the defined benefit pension plan and SERPs is November 30. Following are the weighted average actuarial assumptions used

in calculating the benefit obligation and net benefit cost as of and for the years ended December 31:

2005 2004 2003

Net periodic benefit cost:

Discount rate 6.00% 6.25% 6.75%

Expected return on plan assets 8.50% 8.75% 8.75%

Rate of compensation increase 4.50% 4.50% 4.50%

Projected benefit obligation:

Discount rate 5.90% 6.00% 6.25%

Rate of compensation increase 5.75% 4.50% 4.50%

The Company utilizes a building-block approach in determining the long-term expected rate of return on plan assets. Historical markets are studied and long-

term historical relationships between equity securities and fixed income securities are preserved consistent with the widely accepted capital market principle

that assets with higher volatility generate a greater return over the long run. Current market factors such as inflation and interest rates are evaluated before

long-term capital market assumptions are determined. The long-term portfolio return also takes proper consideration of diversification and rebalancing. Peer

data and historical returns are reviewed for reasonableness and appropriateness.

F-32