MoneyGram 2005 Annual Report Download - page 23

Download and view the complete annual report

Please find page 23 of the 2005 MoneyGram annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

|

|

Table of Contents

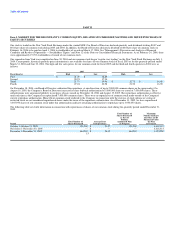

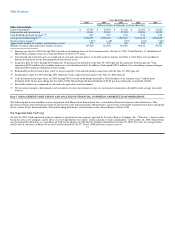

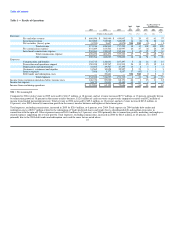

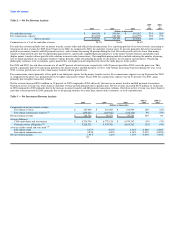

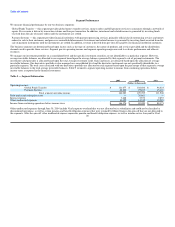

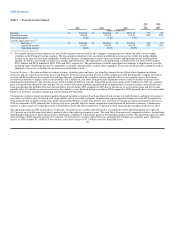

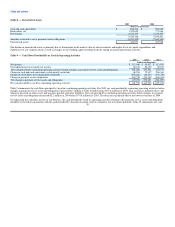

currency exchange spreads on international money transfer transactions. Other revenue consists of processing fees on rebate checks and controlled

disbursements, service charges on aged outstanding money orders, money order dispenser fees and other miscellaneous charges.

Investment revenue consists of interest and dividends generated through the investment of cash balances received from the sale of official checks, money

orders and other payment instruments. These cash balances are available to us for investment until the payment instrument is presented for payment.

Investment revenue varies depending on the level of investment balances and the yield on our investments. Investment balances vary based on the number of

payment instruments sold, the average face amount of those payment instruments and the average length of time that passes until the instruments are

presented for payment. Net securities gains and losses consist of realized gains and losses on the sale of investments, as well as other-than-temporary

impairments of investments.

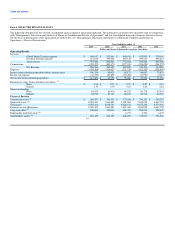

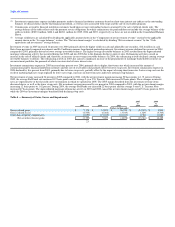

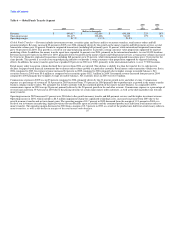

We incur commission expense on our money transfer products and our investments. We pay fee commissions to our third-party agents for money transfer

services. In a money transfer transaction, both the agent initiating the transaction and the agent disbursing the funds receive a commission. The commission

amount generally is based on a percentage of the fee charged to the consumers. We generally do not pay commissions to agents on the sale of money orders.

Fee commissions also include the amortization of capitalized incentive payments to agents.

Investment commissions are amounts paid to financial institution customers based on the average outstanding cash balances generated by the sale of official

checks, as well as costs associated with swaps and the sale of receivables program. In connection with our interest rate swaps, we pay a fixed amount to a

counterparty and receive a variable rate payment in return. To the extent that the fixed rate exceeds the variable rate, we incur an expense related to the swap;

conversely, if the variable rate exceeds the fixed rate, we receive income related to the swap. Under our receivables program, we sell our receivables at a

discount to accelerate our cash flow; this discount is recorded as an expense. Commissions paid to financial institution customers generally are variable based

on short-term interest rates. We utilize interest rate swaps, as described above, to convert a portion of our variable rate commission payments to fixed rate

payments. These swaps assist us in managing the interest rate risk associated with the variable rate commissions paid to our financial institution customers.

20