MoneyGram 2005 Annual Report Download - page 42

Download and view the complete annual report

Please find page 42 of the 2005 MoneyGram annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

|

|

Table of Contents

value of investments are other than temporary. The risks and uncertainties include changes in general economic conditions, the issuer's financial condition or

near term recovery prospects, the effects of changes in interest rates, the length of time and the extent to which the market value of the investment has been

less than cost and the Company's intent and ability to hold the investment for a period of time sufficient to allow for any anticipated recovery in market value.

In addition, for securitized financial assets with contractual cash flows (e.g. asset-backed securities), projections of expected future cash flows may change

based upon new information regarding the performance of the underlying collateral.

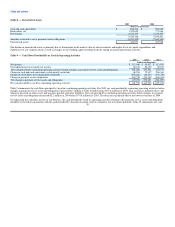

We recorded $6.6 million, $15.9 million and $27.9 million of other-than-temporary impairment losses in 2005, 2004 and 2003, respectively, primarily related

to other asset-backed securities, collateralized mortgage obligations and structured notes held in our investment portfolio. During 2005 and 2004, we received

$12.6 million and $1.9 million in cash recoveries on previously impaired securities. No recoveries were received in 2003. Adverse changes in estimated cash

flows in the future could result in impairment losses to the extent that the recorded value of such investments exceeds fair value.

Derivative financial instruments — Derivative financial instruments are used as part of our risk management strategy to manage exposure to fluctuations in

interest and foreign currency rates. We do not enter into derivatives for speculative purposes. Derivatives are accounted for in accordance with SFAS No. 133,

Accounting for Derivative Instruments and Hedging Activities, and its related amendments and interpretations. The derivatives are recorded as either assets or

liabilities on the balance sheet at fair value, with the change in fair value recognized in earnings or in other comprehensive income depending on the use of the

derivative and whether it qualifies for hedge accounting. A derivative that does not qualify, or is not designated, as a hedge will be reflected at fair value, with

changes in value recognized through earnings. The estimated fair value of derivative financial instruments has been determined using available market

information and certain valuation methodologies. However, considerable judgment is required in interpreting market data to develop the estimates of fair

value. Accordingly, the estimates determined may not be indicative of the amounts that could be realized in a current market exchange. The use of different

market assumptions or valuation methodologies may have a material effect on the estimated fair value amounts. While MoneyGram intends to continue to

meet the conditions to qualify for hedge accounting treatment under SFAS No. 133, if hedges did not qualify as highly effective or if forecasted transactions

are no longer probable of occurring or did not occur, the changes in the fair value of the derivatives used as hedges would be reflected in earnings.

MoneyGram does not believe it is exposed to more than a nominal amount of credit risk in its hedging activities as the counterparties are generally well-

established, well-capitalized financial institutions.

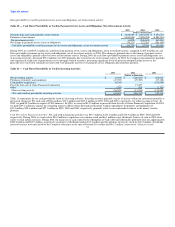

Goodwill — SFAS No. 142, Goodwill and Other Intangible Assets, requires annual impairment testing of goodwill based on the estimated fair value of

MoneyGram's reporting units. The fair value of MoneyGram's reporting units is estimated based on discounted expected future cash flows using a weighted

average cost of capital rate. Additionally, an assumed terminal value is used to project future cash flows beyond base years. The estimates and assumptions

regarding expected cash flows, terminal values and the discount rate require considerable judgment and are based on historical experience, financial forecasts,

and industry trends and conditions. During the third quarter of 2004, MoneyGram recorded a charge of $2.1 million related to certain intangible assets.

Pension obligations — MoneyGram has trusteed, noncontributory pension plans that cover certain employees of MoneyGram, as well as former employees of

Viad and of sold operations of Viad. Through December 31, 2000, the principal retirement plan was structured using a traditional defined benefit formula

based primarily on final average pay and years of service. Benefits earned under this formula ceased accruing at December 31, 2000, with no change to

retirement benefits earned through that date. Effective January 1, 2001, benefits began accruing under a cash accumulation account formula based upon a

percentage of pay plus interest. Benefits under the cash accumulation formula ceased accruing at December 31, 2003, with no change in benefits earned

through that date. Funding policies provide that payments to defined benefit pension trusts shall be at least equal to the minimum funding required by

applicable regulations. Certain defined pension benefits, primarily those in excess of benefit levels permitted under qualified pension plans, are unfunded.

MoneyGram's discount rate used in determining future pension obligations is measured on November 30 and is based on rates determined by actuarial

analysis 39