MoneyGram 2005 Annual Report Download - page 76

Download and view the complete annual report

Please find page 76 of the 2005 MoneyGram annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

|

|

Table of Contents

MONEYGRAM INTERNATIONAL, INC. AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS — (Continued)

currency forwards as cash flow hedges. If the forecasted transaction underlying the hedge is no longer probable of occurring, any gain or loss recorded in

equity is reclassified into earnings.

The Company has also entered into swap agreements to mitigate the effects on cash flows of interest rate fluctuations on variable rate debt and commissions

paid to financial institution customers of our Payment Systems segment. The agreements involve varying degrees of credit and market risk in addition to

amounts recognized in the financial statements. These swaps are designated as cash flow hedges. The swap agreements are contracts to pay fixed and receive

floating payments periodically over the lives of the agreements without the exchange of the underlying notional amounts. The notional amounts of such

agreements are used to measure amounts to be paid or received and do not represent the amount of the exposure to credit loss. The amounts to be paid or

received under the swap agreements are accrued in accordance with the terms of the agreements and market interest rates.

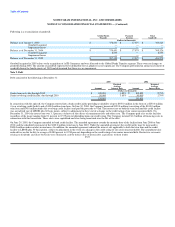

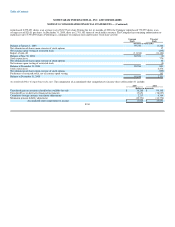

The notional amount of the swap agreements totaled $2.7 billion and $3.4 billion at December 31, 2005 and 2004, respectively, with an average fixed pay rate

of 4.2% and 4.8% and an average variable receive rate 4.1% and 2.1% at December 31, 2005 and 2004, respectively. The variable rate portion of the swaps is

generally based on Treasury bill, federal funds, or 6 month LIBOR. As the swap payments are settled, the net difference between the fixed amount the

Company pays and the variable amount the Company receives is reflected in the Consolidated Statements of Income in "Investment commissions expense."

The amount recognized in earnings due to ineffectiveness of the cash flow hedges is not material for any year presented. The Company estimates that

approximately $5.3 million (net of tax) of the unrealized loss reflected in the "Accumulated other comprehensive income (loss)" component in the

Consolidated Balance Sheet as of December 31, 2005, will be reflected in the Consolidated Statement of Income in "Investment commissions expense" within

the next 12 months as the swap payments are settled. The agreements expire as follows:

Notional Amount

(Dollars in thousands)

2006 $ 630,000

2007 1,200,000

2008 100,000

2009 450,000

Thereafter 317,000

$ 2,697,000

Fair value hedges use derivatives to mitigate the risk of changes in the fair values of assets, liabilities and certain types of firm commitments. The Company

uses fair value hedges to manage the impact of changes in fluctuating interest rates on certain available-for-sale securities. Interest rate swaps are used to

modify exposure to interest rate risk by converting fixed rate assets to a floating rate. All amounts have been included in earnings along with the hedged

transaction in the Consolidated Statement of Income in "Investment revenue." Realized gains of $0.1 million and $2.1 million were recognized on fair value

hedges discontinued during 2004 and 2003, respectively. No gain or loss was recognized in connection with the discontinued fair value hedges in 2005.

The Company uses derivatives to hedge exposures for economic reasons, including circumstances in which the hedging relationship does not qualify for

hedge accounting. The Company is exposed to foreign currency exchange risk and utilizes forward contracts to hedge assets and liabilities denominated in

foreign currencies. While these contracts economically hedge foreign currency risk, they are not designated as hedges for accounting purposes under

SFAS No. 133, Accounting for Derivative Instruments and Hedging Activities. The effect of changes in foreign exchange rates on the foreign-denominated

receivables and payables, net of the effect of the related forward contracts, recorded in the Consolidated Statement of Income is not significant.

The Company is exposed to credit loss in the event of nonperformance by counterparties to its derivative contracts. Collateral generally is not required of the

counterparties or of the Company. In the unlikely event a counterparty F-22