MasterCard 2009 Annual Report Download - page 97

Download and view the complete annual report

Please find page 97 of the 2009 MasterCard annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

|

|

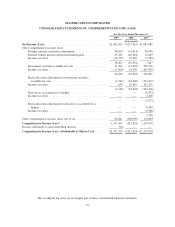

MASTERCARD INCORPORATED

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS—(Continued)

(In thousands, except percent and per share data)

Earnings (loss) per share—A new accounting standard related to instruments granted in share-based

payment transactions became effective for the Company on January 1, 2009, resulting in the retrospective

adjustment of earnings per share (“EPS”) for prior periods. See Note 2 (Earnings (Loss) Per Share) for further

detail.

Recent accounting pronouncements

Transfers of financial assets—In June 2009, the accounting standard for transfers and servicing of financial

assets and extinguishments of liabilities was amended. The change eliminates the qualifying special purpose

entity concept, establishes a new unit of account definition that must be met for the transfer of portions of

financial assets to be eligible for sale accounting, clarifies and changes the derecognition criteria for a transfer to

be accounted for as a sale, changes the amount of gain or loss on a transfer of financial assets accounted for as a

sale when beneficial interests are received by the transferor, and requires additional new disclosures. The

Company will adopt the new standard upon its effective date of January 1, 2010 and does not expect the impact

of the adoption to be material to the Company’s financial position or results of operations.

Variable interest entities—In June 2009, there was a revision to the accounting standard for the

consolidation of variable interest entities. The revision eliminates the exemption for qualifying special purpose

entities, requires a new qualitative approach for determining whether a reporting entity should consolidate a

variable interest entity, and changes the requirement of when to reassess whether a reporting entity should

consolidate a variable interest entity. During February 2010, the scope of the revised standard was modified to

indefinitely exclude certain entities from the requirement to be assessed for consolidation. The standard is

effective beginning on January 1, 2010 and the Company does not expect the impact of the adoption to be

material to the Company’s financial position or results of operations.

Revenue arrangements with multiple deliverables—In September 2009, the accounting standard for the

allocation of revenue in arrangements involving multiple deliverables was amended. Current accounting

standards require companies to allocate revenue based on the fair value of each deliverable, even though such

deliverables may not be sold separately either by the company itself or other vendors. The new accounting

standard eliminates (i) the residual method of revenue allocation and (ii) the requirement that all undelivered

elements must have objective and reliable evidence of fair value before a company can recognize the portion of

the overall arrangement fee that is attributable to items that already have been delivered. The Company will

adopt the revised accounting standard effective January 1, 2011 via prospective adoption. The Company is

currently evaluating the requirements of the standard to determine the impact on the Company’s financial

position or results of operations.

Improving fair value disclosures—In January 2010, fair value disclosure requirements were amended such

that MasterCard will be required to present detailed disclosures about transfers to and from Level 1 and 2 of the

Valuation Hierarchy effective January 1, 2010 and MasterCard will also be required to present purchases, sales,

issuances, and settlements on a “gross” basis within the Level 3 (of the Valuation Hierarchy) reconciliation

effective January 1, 2011. The Company will adopt the guidance during 2010 and 2011, as required, and the

adoption will have no impact on the Company’s financial position or results of operations.

Note 2. Earnings (Loss) Per Share (“EPS”)

On January 1, 2009, a new accounting standard related to the EPS effects of instruments granted in share-

based payment transactions became effective for the Company resulting in the retrospective adjustment of EPS

for prior periods. In accordance with this new accounting standard, unvested share-based payment awards which

receive non-forfeitable dividend rights, or dividend equivalents, are considered participating securities and are

87