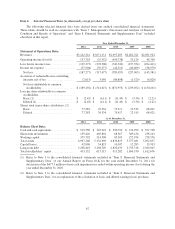

Cricket Wireless 2012 Annual Report Download - page 65

Download and view the complete annual report

Please find page 65 of the 2012 Cricket Wireless annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

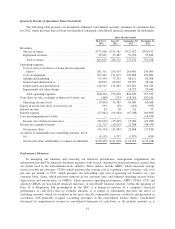

|

|

The closing price of Leap common stock was $6.65 on December 31, 2012 and Leap’s market capitalization

was above our book value as of such date. Since that time, the closing price of Leap common stock has ranged

from a high of $7.05 per share to a low of $5.51 per share. If the price of Leap common stock continues to trade

at or near current levels or certain triggering events were to occur, we may be required to perform the second step

of our goodwill impairment test on an interim basis to determine the fair value of our net assets, which may

require us to recognize a non-cash impairment charge for some or all of the $31.9 million carrying value of our

goodwill.

Based upon our annual impairment test conducted during the third quarter of 2011, we determined that no

impairment condition existed because the book value of our net assets as of August 31, 2011 was $676.1 million

and the fair value of our company, based upon our average market capitalization during the month of August and

an assumed control premium of 30%, was $848.4 million.

Based upon on our annual impairment test conducted during the third quarter of 2010, the book value of our

net assets exceeded the fair value of our company, determined based upon our average market capitalization

during the month of August 2010 and an assumed control premium of 30%. We therefore performed the second

step of the assessment to measure the amount of any impairment. Under step two of the assessment, we

performed a hypothetical purchase price allocation as if our company was being acquired in a business

combination and estimated the fair value of our identifiable assets and liabilities. This step of the assessment

indicated that the implied fair value of our goodwill was zero, as the fair value of our identifiable assets and

liabilities as of August 31, 2010 exceeded the fair value of our company. As a result, we recorded a non-cash

impairment charge of $430.1 million in the third quarter of 2010, reducing the carrying amount of our goodwill

at that time to zero.

Income Taxes

We calculate income taxes in each of the jurisdictions in which we operate. This process involves

calculating the current tax expense or benefit and any deferred income tax expense or benefit resulting from

temporary differences arising from differing treatments of items for tax and accounting purposes. These

temporary differences result in deferred tax assets and liabilities. Deferred tax assets are also established for the

expected future tax benefits to be derived from our NOL carryforwards, capital loss carryforwards and income

tax credits.

We periodically assess the likelihood that our deferred tax assets will be recoverable from future taxable

income. To the extent we believe it is more likely than not that our deferred tax assets will not be recovered, we

must establish a valuation allowance. As part of this periodic assessment for the year ended December 31, 2012,

we weighed the positive and negative factors and, at this time, we do not believe there is sufficient positive

evidence to support a conclusion that it is more likely than not that all or a portion of our deferred tax assets will

be realized, except with respect to the realization of a $1.9 million Texas Margins Tax, or TMT, credit.

Accordingly, at December 31, 2012 and 2011, we recorded a valuation allowance offsetting substantially all of

our deferred tax assets. We will continue to monitor the positive and negative factors to assess whether we are

required to continue to maintain a valuation allowance. At such time as we determine that it is more likely than

not that all or a portion of the deferred tax assets are realizable, the valuation allowance will be reduced or

released in its entirety, with the corresponding benefit reflected in our tax provision. Deferred tax liabilities

associated with wireless licenses and investments in certain joint ventures cannot be considered a source of

taxable income to support the realization of deferred tax assets because these deferred tax liabilities will not

reverse until some indefinite future period when these assets are either sold or impaired for book purposes.

We have substantial federal and state NOLs for income tax purposes. Subject to certain requirements, we

may “carry forward” our federal NOLs for up to 20 years to offset future taxable income and reduce our income

tax liability. For state income tax purposes, the NOL carryforward period ranges from five to 20 years. As of

December 31, 2012, we had federal and state NOLs of approximately $2.6 billion and $2.0 billion, respectively,

51