Avon 2012 Annual Report Download - page 52

Download and view the complete annual report

Please find page 52 of the 2012 Avon annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

|

|

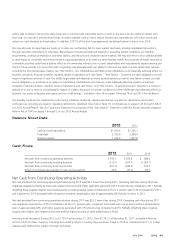

(1) Amounts represent expected future benefit payments for our unfunded pension and postretirement benefit plans, as well as expected contributions for 2013

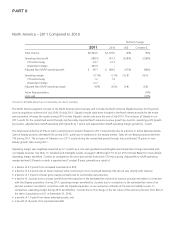

to our funded pension benefit plans. We are not able to estimate our contributions to our funded pension and postretirement plans beyond 2013.

(2) The amount of debt and contractual financial obligations and commitments excludes amounts due under derivative transactions. The table also excludes

information on non-binding purchase orders of inventory. The table does not include any reserves for income taxes because we are unable to reasonably

predict the ultimate amount or timing of settlement of our reserves for income taxes. At December 31, 2012, our reserves for income taxes, including interest

and penalties, totaled $32.6.

(3) At December 31, 2012, long-term debt due in 2013 excluded $535.0 of private notes, of which $142.0 were contractually due in 2015, $290.0 were

contractually due in 2020, and $103.0 were contractually due in 2022, and are therefore included in those respective maturity categories above. In February

2013, we issued a notice of prepayment of the entire $535 outstanding principal amount of our Private Notes (plus the make-whole premium and accrued

interest), which, pursuant to the notice, is required to be prepaid on March 29, 2013. See the “Capital Resources – Private Notes” section below for more

details.

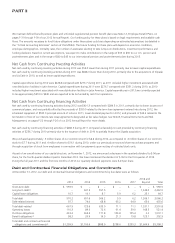

See Note 5, Debt and Other Financing, and Note 14, Leases and Commitments, on pages F-15 through F-19, and on page F-42, respectively,

of our 2012 Annual Report for further information on our debt and contractual financial obligations and commitments. Additionally, as

disclosed in Note 15, Restructuring Initiatives on pages F-42 through F-46 of our 2012 Annual Report, we have a remaining liability of $21.0

at December 31, 2012, associated with the restructuring charges recorded to date under the 2005 and 2009 Restructuring Programs. We

also have a remaining liability of $29.4 associated with other restructuring initiatives approved during 2012, and $43.0 associated with our

$400M Cost Savings Initiative, at December 31, 2012. The majority of future cash payments associated with these liabilities are expected to

be made during 2013.

Off Balance Sheet Arrangements

At December 31, 2012, we had no material off-balance-sheet arrangements.

Capital Resources

Revolving Credit Facility

We maintain a $1 billion revolving credit facility (the “revolving credit facility”), which expires in November 2013. As discussed below, the

$1 billion available under the revolving credit facility is effectively reduced by the principal amount of any commercial paper outstanding.

Borrowings under the revolving credit facility bear interest, at our option, at a rate per annum equal to the floating base rate or LIBOR, plus

an applicable margin which varies within a specified band based upon our credit ratings. As of December 31, 2012, there were no amounts

outstanding under the revolving credit facility.

The revolving credit facility contains covenants limiting our ability to, among other things, incur liens and enter into mergers and

consolidations or sales of substantially all our assets, and a financial covenant which requires our interest coverage ratio at the end of each

fiscal quarter to equal or exceed 4:1. In addition, the revolving credit facility contains customary events of default and cross-default

provisions. The interest coverage ratio is determined by dividing our consolidated pre-tax income by our consolidated interest expense, in

each case for the period of four fiscal quarters ending on the date of determination. On July 31, 2012, we obtained a waiver from the

lenders under our revolving credit facility that allowed us to exclude the non-cash impairment charge associated with the Silpada business

recorded during the fourth quarter of 2011 from the interest coverage ratio calculation pursuant to our revolving credit facility for the four

fiscal quarters ended September 30, 2012. On December 21, 2012, we entered into an amendment to the revolving credit facility, primarily

relating to the calculation of components of the interest coverage ratio that allows us, subject to certain conditions and limitations, to add

back to our consolidated net income: (i) extraordinary and other non-cash losses and expenses, (ii) one-time fees, cash charges and other

cash expenses, premiums or penalties incurred in connection with any asset sale, equity issuance or incurrence or repayment of debt or

refinancing or amendment of any debt instrument and (iii) cash charges and other cash expenses, premiums or penalties incurred in

connection with any restructuring or relating to any legal or regulatory action, settlement, judgment or ruling, in an aggregate amount not

to exceed $400.0 for the period from October 1, 2012 until the termination of commitments under the revolving credit facility. As of

December 31, 2012, and based on then interest rates, approximately $250 of the $1 billion revolving credit facility, less the principal amount

of commercial paper outstanding (which was zero at December 31, 2012), could have been drawn down without violating any covenant. If

not for the more restrictive interest coverage ratio calculation under our Private Notes (which, pursuant to a notice, is required to be prepaid

on March 29, 2013, see below), we would have been able to draw down on the entire $1 billion under our revolving credit facility at

December 31, 2012 without violating any covenant. The interest coverage ratio, under our revolving credit facility, for the four fiscal quarters

ended December 31, 2012 was 6.64:1 and excludes certain cash and non-cash charges pursuant to the December 2012 amendment.

A V O N 2012 45