Avon 2012 Annual Report Download - page 114

Download and view the complete annual report

Please find page 114 of the 2012 Avon annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121

|

|

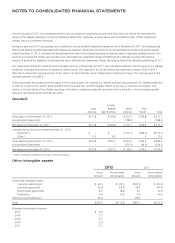

implied fair value of the reporting unit’s goodwill. The second step of the impairment analysis requires a valuation of a reporting unit’s

tangible and intangible assets and liabilities in a manner similar to the allocation of purchase price in a business combination. If the resulting

implied fair value of the reporting unit’s goodwill is less than its carrying value, that difference represents an impairment.

The impairment analyses performed for goodwill and intangible assets require several estimates in computing the estimated fair value of a

reporting unit, an indefinite-lived intangible asset, and a finite-lived intangible asset. We use a DCF approach to estimate the fair value of a

reporting unit, which we believe is the most reliable indicator of fair value of a business, and is most consistent with the approach a

marketplace participant would use. The estimation of fair value utilizing a DCF approach includes numerous uncertainties which require our

significant judgment when making assumptions of expected growth rates and the selection of discount rates, as well as assumptions

regarding general economic and business conditions, and the structure that would yield the highest economic value, among other factors.

Key assumptions used in measuring the fair values of Silpada and China included the discount rate (based on the weighted-average cost of

capital) and revenue growth, as well as silver prices and Representative growth and activity rates for Silpada. The fair value of Silpada’s

indefinite-lived trademark was determined using a risk-adjusted DCF model under the relief-from-royalty method. The royalty rate used was

based on a consideration of market rates. The fair value of the Silpada finite-lived customer relationships was determined using a DCF model

under the multi-period excess earnings method. A significant decline in expected future cash flows and growth rates or a change in the

discount rate used to fair value expected future cash flows may result in future impairment charges.

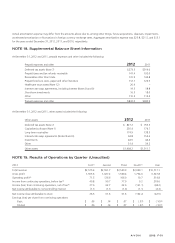

2012 Silpada Impairment Assessment

During our year-end 2012 close process, we completed our annual goodwill impairment assessment as of November 30, 2012 and

subsequently determined that the goodwill associated with Silpada was impaired. Specifically, the results of our annual impairment testing

during the quarter ended December 31, 2012, indicated that the estimated fair value of our Silpada reporting unit was less than its

respective carrying amount. This was primarily the result of the weaker than expected performance in the fourth quarter of 2012, largely

due to lower Representative counts and activity rates, and as a result we lowered our revenue and earnings projections for Silpada. The

decline in the fair values of the Silpada reporting unit, the trademark, and customer relationships was driven by the reduction in the

forecasted growth rates and cash flows used to estimate fair value. As a result of our impairment testing, we recorded a non-cash before tax

impairment charge of $72.1 ($45.6 after tax) to reduce the carrying amount of goodwill for Silpada to its estimated fair value. Following the

impairment charge, the carrying value of the Silpada goodwill was $44.6.

Our impairment testing for indefinite-lived intangible assets as of November 30, 2012, also indicated a decline in the fair value of our Silpada

trademark intangible asset below its respective carrying value. This resulted in a non-cash before tax impairment charge of $45.0 ($28.5

after tax) to reduce the carrying amount of this asset to its estimated fair value. Following the impairment charge, the carrying value of the

Silpada trademark was $40.0.

We also performed an impairment test for our Silpada finite-lived intangible assets as of November 30, 2012, which indicated the carrying

value of our Silpada customer relationships asset exceeded estimated future undiscounted cash flows of the business. This resulted in a non-

cash before tax impairment charge of $91.9 ($58.1 after tax) to reduce the carrying amount of this asset to its estimated fair value.

Following the impairment charge, the carrying value of the Silpada customer relationships was $40.0.

2012 China Impairment Assessment

Based on the continued decline in revenue performance in China during the third quarter of 2012 and a corresponding lowering of our

long-term growth estimates in China, we completed an interim impairment assessment of the fair value of goodwill related to our

operations in China. The changes to our long-term growth estimates were based on the state of our China business, which was

predominantly retail at that time. We are still analyzing our long-term strategic plan for China and any changes to our long-term strategic

plan may impact our expectations of future financial performance. Based upon this interim analysis, we determined that the goodwill related

to our operations in China was impaired. Specifically, the results of our interim impairment test indicated the estimated fair value of our

China reporting unit was less than its respective carrying amount. As a result of our impairment testing, we recorded a non-cash impairment

charge of $44.0 ($44.0 after tax) to reduce the carrying amount of goodwill for China to its estimated fair value. Following the impairment

charge, the carrying value of the China goodwill was approximately $37.3.

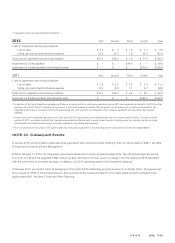

2011 Silpada Impairment Assessment

In the second quarter of 2011, due to the impact of rising silver prices and declines in revenues relative to our internal forecasts, we

completed an interim impairment assessment of the fair value of goodwill and an indefinite-lived intangible asset related to Silpada. Based

upon this interim analysis, the estimated fair value of the Silpada reporting unit and its trademark exceeded their respective carrying value. In

A V O N 2012 F-49