Avon 2012 Annual Report Download - page 34

Download and view the complete annual report

Please find page 34 of the 2012 Avon annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

|

|

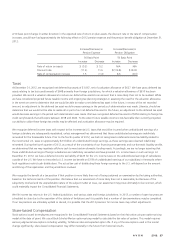

A 50 basis point change (in either direction) in the expected rate of return on plan assets, the discount rate or the rate of compensation

increases, would have had approximately the following effect on 2012 pension expense and the pension benefit obligation at December 31,

2012:

Increase/(Decrease) in

Pension Expense

Increase/(Decrease) in

Pension Obligation

50 Basis Point 50 Basis Point

Increase Decrease Increase Decrease

Rate of return on assets $ (5.2) $ 5.2 N/A N/A

Discount rate (11.2) 11.6 $(114.8) $123.8

Rate of compensation increase 1.5 (1.4) 8.6 (8.3)

Taxes

At December 31, 2012, we recognized net deferred tax assets of $1,067, net of a valuation allowance of $627. We have gross deferred tax

assets relating to tax loss carryforwards of $648 primarily from foreign jurisdictions, for which a valuation allowance of $610 has been

provided. We record a valuation allowance to reduce our deferred tax assets to an amount that is more likely than not to be realized. While

we have considered projected future taxable income and ongoing tax planning strategies in assessing the need for the valuation allowance,

in the event we were to determine that we would be able to realize a net deferred tax asset in the future, in excess of the net recorded

amount, an adjustment to the deferred tax asset would increase earnings in the period such determination was made. Likewise, should we

determine that we would not be able to realize all or part of our net deferred tax asset in the future, an adjustment to the deferred tax asset

would decrease earnings in the period such determination was made. We have recognized deferred tax assets of $356 relating to foreign tax

credit carryforwards that will expire between 2018 and 2022. To the extent future taxable income is less favorable than currently projected,

our ability to utilize these foreign tax credits may be affected and a valuation allowance may be required.

We recognize deferred income taxes with respect to the incremental U.S. taxes that would be incurred when undistributed earnings of a

foreign subsidiary are subsequently repatriated, unless management has determined that those undistributed earnings are indefinitely

reinvested for the foreseeable future. Prior to the fourth quarter of 2012, we had not recognized a deferred income tax liability related to

the incremental U.S. taxes on approximately $2.5 billion of undistributed foreign earnings, as these earnings were deemed indefinitely

reinvested. During the fourth quarter of 2012, as a result of the uncertainty of our financing arrangements and our domestic liquidity profile,

we determined that we may repatriate offshore cash to meet certain domestic funding needs. Accordingly, we are no longer asserting that

these undistributed earnings of foreign subsidiaries are indefinitely reinvested and have provided U.S. income taxes on such earnings. At

December 31, 2012, we have a deferred income tax liability of $225 for the U.S. income taxes on the undistributed earnings of subsidiaries

outside of the U.S. We have not recorded a U.S. income tax benefit on $159 of undistributed earnings of our subsidiary in Venezuela where

local regulations restrict cash distributions. The actual tax cost of distributing these foreign earnings to the U.S. will depend on the amount

and timing of the repatriation and the jurisdictions involved.

We recognize the benefit of a tax position if that position is more likely than not of being sustained on examination by the taxing authorities,

based on the technical merits of the position. We believe that our assessment of more likely than not is reasonable, but because of the

subjectivity involved and the unpredictable nature of the subject matter at issue, our assessment may prove ultimately to be incorrect, which

could materially impact the Consolidated Financial Statements.

We file income tax returns in the U.S. federal jurisdiction, and various state and foreign jurisdictions. In 2013, a number of open tax years are

scheduled to close due to the expiration of the statute of limitations and it is possible that a number of tax examinations may be completed.

If our tax positions are ultimately upheld or denied, it is possible that the 2013 provision for income taxes may reflect adjustments.

Share-based Compensation

Stock options issued to employees are recognized in the Consolidated Financial Statements based on their fair value using an option-pricing

model at the date of grant. We use a Black-Scholes-Merton option-pricing model to calculate the fair value of options. This model requires

various judgmental assumptions including volatility, forfeiture rates and expected option life. If any of the assumptions used in the model

change significantly, share-based compensation may differ materially in the future from historical results.

A V O N 2012 27