Asus 2012 Annual Report Download - page 184

Download and view the complete annual report

Please find page 184 of the 2012 Asus annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

174 -

175

175 -

176

176 -

177

177 -

178

178 -

179

179 -

180

180 -

181

181 -

182

182 -

183

183 -

184

184 -

185

185 -

186

186 -

187

187 -

188

188 -

189

189 -

190

190 -

191

191 -

192

192 -

193

193 -

194

194 -

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

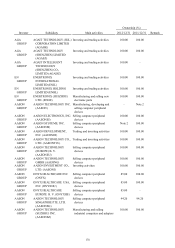

|

|

180

(16) Treasury stock

A. When the Company acquires its outstanding shares as treasury stock, the acquisition cost

should be debited to the treasury stock account (a contra account under stockholders’ equity).

B. When the Company’s treasury stock is retired, the treasury stock account should be credited,

and the capital surplus-premium on stock account and capital stock account should be debited

proportionately according to the share ratio. An excess of the carrying value of treasury stock

over the sum of its par value and premium on stock should first be offset against capital

surplus from the same class of treasury stock transactions, and the remainder, if any, debited to

retained earnings. An excess of the sum of the par value and premium on stock of treasury

stock over its carrying value should be credited to additional paid-in capital from the same

class of treasury stock transactions.

C. The cost of treasury stock is accounted for on a weighted-average basis.

(17) Employees’ bonuses and directors’ and supervisors’ remuneration and share-based payment

Pursuant to Interpretation (96) 052 issued by the ARDF, the costs of employees’ bonuses and

directors’ and supervisors’ remuneration of the Company and domestic subsidiaries are accounted

for as expenses (costs) and liabilities, provided that such recognition is required under legal or

constructive obligation and the amounts can be estimated reasonably. However, if the accrued

amounts for employees’ bonuses and directors’ and supervisors’ remuneration are significantly

different from the distributed amounts resolved by the Board of Directors, then the differences

shall be adjusted in current year’s gain or loss (the year of recognition) and, if the accrued amounts

for employees’ bonus and directors’ and supervisors’ remuneration are significantly different from

the actual distributed amounts resolved by the stockholders at their annual stockholders’ meeting

subsequently, the differences shall be recognized as gain or loss in the following year. In addition,

according to Interpretation (97) 127 issued by the ARDF, the Company calculates the number of

shares of employees’ stock bonus based on the closing price of the Company’s common stock at

the previous day of the stockholders’ meeting held in the year following the financial reporting

year, and after taking into account the effects of ex-rights and ex-dividends. The Group adopts

SFAS No. 39 to account for the transfer of equity instruments from shareholders to the Group’s

employees.

(18) Earnings per share

A. Earnings per share of common stock is computed based on the weighted-average number of

common shares outstanding during the period. Earnings per share for prior period is

retroactively adjusted to reflect the effects of new shares issued from the capitalization of

additional paid-in capital or retained earnings.

B. The convertible bonds and employee stock bonuses which have not yet been approved in the

stockholders’ meeting are potential common shares. Only basic earnings per share is disclosed

if there is no dilutive effect. Otherwise, both basic and diluted earnings per share are disclosed.

For the purpose of calculating diluted earnings per share, the potential common shares are

deemed to have been converted into common stock at the beginning of the period, and the

effect on net income of the additional common shares outstanding is considered accordingly.