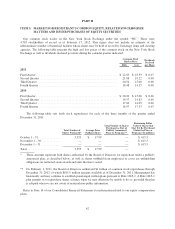

Western Union 2011 Annual Report Download - page 40

Download and view the complete annual report

Please find page 40 of the 2011 Western Union annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

|

|

well as the regulations required by that Act and the creation of the Consumer Financial Protection Bureau could

adversely affect us and the scope of our activities, and could adversely affect our operations, results of

operations and financial condition.” Recently proposed and enacted legislation related to financial services

providers and consumer protection in various jurisdictions around the world and at the federal and state level in

the United States may subject us to additional regulatory oversight, mandate additional consumer disclosures and

remedies, including refunds to consumers, mandate additional taxes or fees to be imposed upon consumers, or

otherwise impact the manner in which we provide our services. If governments implement new laws or

regulations that limit our right to set fees and/or foreign exchange spreads, then our business, financial condition

and results of operations could be adversely affected. In addition, changes in regulatory expectations,

interpretations or practices could increase the risk of regulatory enforcement actions, fines and penalties.

For example, our business is currently being affected by on-going changes to our compliance procedures

related to our agreement and settlement with the State of Arizona. See risk factor “Western Union is the subject

of governmental investigations and consent agreements with or enforcement actions by regulators.” Due to

regulatory initiatives, we will continue to evolve our business model and practices along the United States and

Mexico border, including in the southwestern region of the United States. Such changes will likely have an

adverse effect on our revenues, profits, and business operations.

In addition, one state has passed a law imposing a fee on certain money transfer transactions, and certain other

states have proposed similar legislation. At least two foreign countries have enacted rules imposing taxes or fees

on certain money transfer transactions, as well. Although money transfer services themselves are not generally

subject to sales tax on money transfer services elsewhere in the United States, the current budget shortfalls in

many jurisdictions, combined with continued federal inaction on comprehensive immigration reform, may lead

other states or localities to impose similar taxes or fees. Similar circumstances in foreign countries could invoke

similar consequences. A tax or fee exclusively on money transfer services like Western Union could put us at a

competitive disadvantage to other means of remittance which are not subject to the same taxes or fees.

Other examples of changes to our financial environment include the possibility of regulatory initiatives that

focus on lowering international remittance costs. For example, Pakistan subsidizes certain remittances into the

country from Pakistanis working abroad. We do not participate in this program, but remittance companies

accepting the subsidy are prohibited from charging fees to the sender or receiver. Such initiatives may have an

adverse impact on our business, financial condition and results of operations.

Regulators around the world increasingly look at each other’s approaches to the regulation of the payments

and other industries. Consequently, a development in any one country, state or region may influence regulatory

approaches in other countries, states or regions. This includes the interpretation of the Dodd-Frank Wall Street

Reform and Consumer Protection Act (the “Act”). Similarly, new laws and regulations in a country, state or

region involving one service may cause lawmakers there to extend the regulations to another service. As a result,

the risks created by any one new law or regulation are magnified by the potential they have to be replicated,

affecting our business in another place or involving another service. Conversely, if widely varying regulations

come into existence worldwide, we may have difficulty adjusting our services, fees and other important aspects

of our business, with the same effect. Either of these eventualities could materially and adversely affect our

business, financial condition and results of operations.

Our agents’ or subagents’ failure to comply with federal and laws and regulations as well as laws and

regulations outside the United States could have an adverse effect on our business, financial condition and

results of operations.

Any determination that our agents or subagents have violated laws and regulations could seriously damage our

reputation and brands, resulting in diminished revenue and profit and increased operating costs. In some cases,

we could be liable for the failure of our agents or subagents to comply with laws which also could have an

adverse effect on our business, financial condition and results of operations.

33