Time Warner Cable 2012 Annual Report Download - page 74

Download and view the complete annual report

Please find page 74 of the 2012 Time Warner Cable annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

|

|

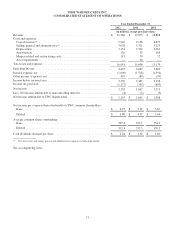

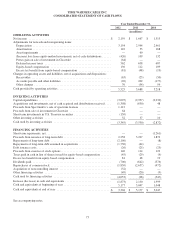

TIME WARNER CABLE INC.

MANAGEMENT’S DISCUSSION AND ANALYSIS OF RESULTS

OF OPERATIONS AND FINANCIAL CONDITION—(Continued)

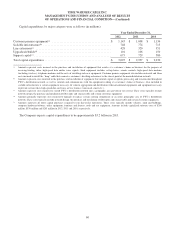

insurance premiums. Such surety bonds and letters of credit as of December 31, 2012 and 2011 totaled $353 million and

$335 million, respectively. Payments under these arrangements are required only in the event of nonperformance. TWC does

not expect that these contingent commitments will result in any amounts being paid in the foreseeable future.

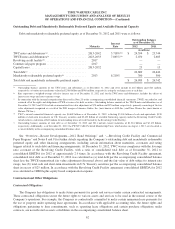

MARKET RISK MANAGEMENT

Market risk is the potential gain/loss arising from changes in market rates and prices, such as interest rates.

Interest Rate Risk

Fixed-rate Debt and TW NY Cable Preferred Membership Units

As of December 31, 2012, TWC had fixed-rate debt and TW NY Cable Preferred Membership Units with an

outstanding balance of $26.670 billion and an estimated fair value of $32.069 billion. As discussed below, TWC has entered

into interest rate swaps to effectively convert a portion of its fixed-rate debt to variable-rate debt. Based on TWC’s fixed-rate

debt obligations outstanding at December 31, 2012, a 25 basis point increase or decrease in the level of interest rates would,

respectively, decrease or increase the fair value of the fixed-rate debt by approximately $675 million (excluding the impact

of such rate changes on the fair value of the interest rate swaps). Such potential increases or decreases are based on certain

simplifying assumptions, including a constant level of fixed-rate debt and an immediate, across-the-board increase or

decrease in the level of interest rates with no other subsequent changes for the remainder of the period.

Variable-rate Debt

As of December 31, 2012, TWC had no outstanding variable-rate debt. However, as discussed below, TWC has entered

into interest rate swaps to effectively convert a portion of its fixed-rate debt to variable-rate debt.

Interest Rate Derivative Transactions

The Company is exposed to the market risk of changes in interest rates. To manage the volatility relating to these

exposures, the Company’s policy is to maintain a mix of fixed-rate and variable-rate debt by entering into various interest

rate derivative transactions as described below to help achieve that mix. Using interest rate swaps, the Company agrees to

exchange, at specified intervals, the difference between fixed and variable interest amounts calculated by reference to an

agreed-upon notional principal amount.

The following table summarizes the terms of the Company’s existing fixed to variable interest rate swaps as of

December 31, 2012:

Maturities ................................................................................. 2013-2018

Notional amount (in millions) ..................................................................$ 7,750

Average pay rate (variable based on LIBOR plus variable margins) .................................... 4.35%

Average receive rate (fixed) ................................................................... 6.43%

Estimated fair value of interest rate swap assets, net (in millions) ......................................$ 294

The notional amounts of interest rate instruments, as presented in the above table, are used to measure interest to be paid or

received and do not represent the amount of exposure to credit loss. Interest rate swaps represent an integral part of the

Company’s interest rate risk management program and resulted in a decrease in interest expense, net, of $160 million in 2012.

Foreign Currency Exchange Risk

TWC is exposed to the market risks associated with fluctuations in the British pound sterling exchange rate as it relates

to its £1.275 billion aggregate principal amount of fixed-rate British pound sterling denominated debt outstanding. As

described further in Note 10 to the accompanying consolidated financial statements, the Company has entered into cross-

currency swaps to effectively convert the entire balance of its fixed-rate British pound sterling denominated debt, including

64