Time Warner Cable 2011 Annual Report Download - page 86

Download and view the complete annual report

Please find page 86 of the 2011 Time Warner Cable annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

|

|

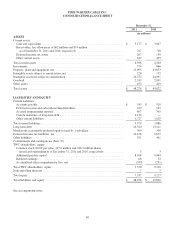

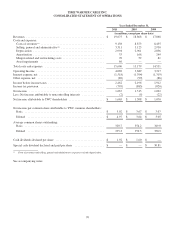

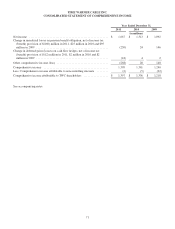

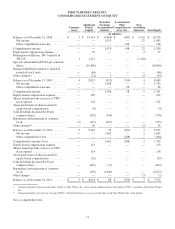

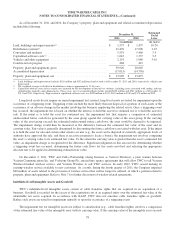

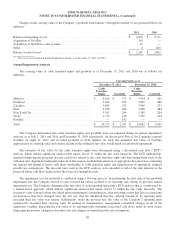

TIME WARNER CABLE INC.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS—(Continued)

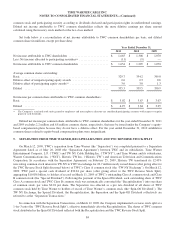

As of December 31, 2011 and 2010, the Company’s property, plant and equipment and related accumulated depreciation

included the following:

December 31, Estimated

Useful

Lives2011 2010

(in millions) (in years)

Land, buildings and improvements(a) ................................. $ 1,557 $ 1,457 10-20

Distribution systems(b) ............................................ 19,470 17,996 3-25

Converters and modems .......................................... 5,591 5,460 3-5

Capitalized software costs(c) ........................................ 1,643 1,337 3-5

Vehicles and other equipment ...................................... 2,191 1,980 3-10

Construction in progress .......................................... 468 419

Property, plant and equipment, gross ................................ 30,920 28,649

Accumulated depreciation ......................................... (17,015) (14,776)

Property, plant and equipment, net .................................. $ 13,905 $ 13,873

(a) Land, buildings and improvements includes $158 million and $152 million related to land as of December 31, 2011 and 2010, respectively, which is not

depreciated.

(b) The weighted-average useful life for distribution systems is approximately 12.44 years.

(c) Capitalized software costs reflect certain costs incurred for the development of internal use software, including costs associated with coding, software

configuration, upgrades and enhancements. These costs, net of accumulated depreciation, totaled $658 million and $581 million as of December 31,

2011 and 2010, respectively. Depreciation of capitalized software costs was $209 million in 2011, $185 million in 2010 and $174 million in 2009.

Long-lived assets do not require an annual impairment test; instead, long-lived assets are tested for impairment upon the

occurrence of a triggering event. Triggering events include the more likely than not disposal of a portion of such assets or the

occurrence of an adverse change in the market involving the business employing the related assets. Once a triggering event

has occurred, the impairment test is based on whether the intent is to hold the asset for continued use or to hold the asset for

sale. If the intent is to hold the asset for continued use, the impairment test first requires a comparison of estimated

undiscounted future cash flows generated by the asset group against the carrying value of the asset group. If the carrying

value of the asset group exceeds the estimated undiscounted future cash flows, the asset would be deemed to be impaired.

The impairment charge would then be measured as the difference between the estimated fair value of the asset and its

carrying value. Fair value is generally determined by discounting the future cash flows associated with that asset. If the intent

is to hold the asset for sale and certain other criteria are met (e.g., the asset can be disposed of currently, appropriate levels of

authority have approved the sale, and there is an active program to locate a buyer), the impairment test involves comparing

the asset’s carrying value to its estimated fair value. To the extent the carrying value is greater than the asset’s estimated fair

value, an impairment charge is recognized for the difference. Significant judgments in this area involve determining whether

a triggering event has occurred, determining the future cash flows for the assets involved and selecting the appropriate

discount rate to be applied in determining estimated fair value.

On December 2, 2011, TWC and Cellco Partnership (doing business as Verizon Wireless), a joint venture between

Verizon Communications Inc. and Vodafone Group Plc, entered into agency agreements that will allow TWC to sell Verizon

Wireless-branded wireless service, and Verizon Wireless to sell TWC services. In early 2012, TWC ceased making its

existing wireless service available to new customers. As a result, during the fourth quarter of 2011, the Company impaired

$60 million of assets related to the provision of wireless service that will no longer be utilized, of which a portion related to

property, plant and equipment. Refer to Note 7 for further discussion of wireless-related agreements.

Indefinite-lived Intangible Assets and Goodwill

TWC’s indefinite-lived intangible assets consist of cable franchise rights that are acquired in an acquisition of a

business. Goodwill is recorded for the excess of the acquisition cost of an acquired entity over the estimated fair value of the

identifiable net assets acquired. In accordance with GAAP, TWC does not amortize cable franchise rights or goodwill.

Rather, such assets are tested for impairment annually or upon the occurrence of a triggering event.

The impairment test for intangible assets not subject to amortization (e.g., cable franchise rights) involves a comparison

of the estimated fair value of the intangible asset with its carrying value. If the carrying value of the intangible asset exceeds

78