Time Warner Cable 2011 Annual Report Download - page 101

Download and view the complete annual report

Please find page 101 of the 2011 Time Warner Cable annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

|

|

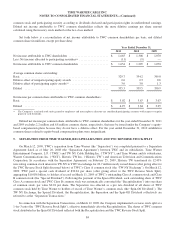

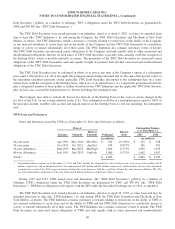

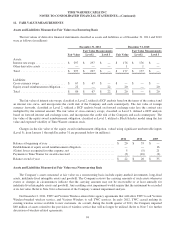

TIME WARNER CABLE INC.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS—(Continued)

is required to make semi-annual interest payments at variable rates, without exchange of the underlying principal amount.

Such contracts are designated as fair value hedges. The Company recognizes no gain or loss related to its interest rate swaps

because the changes in the fair values of such instruments are completely offset by the changes in the fair values of the

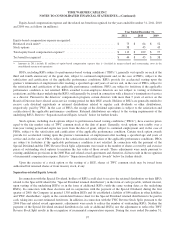

hedged fixed-rate debt. The following table summarizes the terms of the Company’s existing fixed to variable interest rate

swaps as of December 31, 2011 and 2010:

2011 2010

Maturities ..................................................................... 2012-2017 2012-2017

Notional amount (in millions) ..................................................... $ 7,850 $ 6,250

Average pay rate (variable based on LIBOR plus variable margins) ....................... 4.34% 4.33%

Average receive rate (fixed) ...................................................... 6.34% 6.47%

Estimated fair value of asset, net (in millions) ........................................ $ 297 $ 176

The notional amounts of interest rate instruments, as presented in the above table, are used to measure interest to be paid

or received and do not represent the amount of exposure to credit loss. Interest rate swaps represent an integral part of the

Company’s interest rate risk management program and resulted in a decrease in interest expense, net, of $163 million in

2011, $117 million in 2010 and $30 million in 2009.

Cash Flow Hedges

The Company uses cross-currency swaps to manage foreign exchange risk related to foreign currency denominated debt

by effectively converting foreign currency denominated debt, including annual interest payments and the payment of

principal at maturity, to U.S. dollar denominated debt. Such contracts are designated as cash flow hedges. During the second

quarter of 2011, the Company entered into cross-currency swaps to effectively convert the entire balance of its fixed-rate

British pound sterling denominated debt, including annual interest payments and the payment of principal at maturity, to

fixed-rate U.S. dollar denominated debt. The cross-currency swaps have maturities extending through June 2031. As of

December 31, 2011, the fair value of cross-currency swaps was $67 million, which is recorded in other liabilities, with an

offset to accumulated other comprehensive loss, net. During the year ended December 31, 2011, the Company reclassified

$41 million from accumulated other comprehensive loss, net, into other expense, net, to offset the $41 million

re-measurement gain on the British pound sterling denominated debt. Any ineffectiveness related to the Company’s cash

flow hedges has been and is expected to be immaterial.

Equity Award Reimbursement Obligation

Upon the exercise of Time Warner stock options held by TWC employees, TWC is obligated to reimburse Time Warner

for the excess of the market price of Time Warner common stock on the day of exercise over the option exercise price (the

“intrinsic” value of the award). The Company records the equity award reimbursement obligation at fair value in other

current liabilities in the consolidated balance sheet, which is estimated using the Black-Scholes model. The change in the

equity award reimbursement obligation fluctuates primarily with the fair value and expected volatility of Time Warner

common stock and changes in fair value are recorded in other expense, net, in the period of change. As of December 31,

2011, the weighted-average remaining contractual term of outstanding Time Warner stock options held by TWC employees

was 1.30 years. Changes in the fair value of the equity award reimbursement obligation are discussed in Note 12 below.

93