The Hartford 2012 Annual Report Download - page 67

Download and view the complete annual report

Please find page 67 of the 2012 The Hartford annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

|

|

Table of Contents

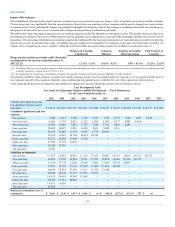

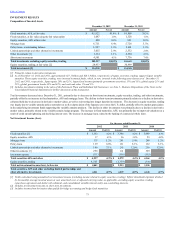

As of December 31, 2012, a 25 basis point increase/decrease in the discount rate would decrease/increase the pension and other postretirement obligations by

$179 and $6, respectively.

The Company determines the expected long-term rate of return assumption based on an analysis of the Plan portfolio’s historical compound rates of return

since 1979 (the earliest date for which comparable portfolio data is available) and over 5 year and 10 year periods. The Company selected these periods, as

well as shorter durations, to assess the portfolio’s volatility, duration and total returns as they relate to pension obligation characteristics, which are influenced

by the Company’s workforce demographics. In addition, the Company also applies long-term market return assumptions to an investment mix that generally

anticipates 60% fixed income securities, 20% equity securities and 20% alternative assets to derive an expected long-term rate of return. Based upon these

analyses, the Company decreased the expected long term rate of return assumption to 7.10% to determine the Company’s 2013 expense. The long-term rate of

return assumption at December 31, 2011 and 2010 that was used to determine the Company’s 2012 and 2011 expense, was 7.30%.

The Company uses a five-year averaging method to determine the market-related value of Plan assets, which is used to determine the expected return

component of pension expense. Under this methodology, asset gains/losses that result from returns that differ from the Company’s long-term rate of return

assumption are recognized in the market-related value of assets on a level basis over a five year period. The difference between actual asset returns for the plans

of $381 and $613 for the years ended December 31, 2012 and 2011, respectively, as compared to expected returns of $312 and $298 for the years ended

December 31, 2012 and 2011, respectively, will be fully reflected in the market-related value of plan assets over the next five years using the methodology

described above. The level of actuarial net loss continues to exceed the allowable amortization corridor. Based on the 4.00% discount rate selected as of

December 31, 2012 and taking into account estimated future minimum funding, the difference between actual and expected performance in 2012 will decrease

annual pension expense in future years. The decrease in pension expense will be approximately $1 in 2013 and will increase ratably to a decrease of

approximately $8 in 2018.

Effective December 31, 2012, the Company amended the Plan to freeze participation and benefit accruals. As a result, employees will not accrue further

benefits under the cash balance formula of the plan, although interest will continue to accrue to existing account balances. Compensation earned by employees

up to December 31, 2012 will be used for purposes of calculating benefits under the Plan but there will be no future benefit accruals after that date.

Participants as of December 31, 2012 will continue to earn vesting credit with respect to their frozen accrued benefits as they continue to work. The freeze also

applies to The Hartford Excess Pension Plan II, the Company's non-qualified excess benefit plan for certain highly compensated employees, effective December

31, 2012. The Company announced these changes in April 2012.

Pension expense reflected in the Company’s results was $242, $213 and $186 in 2012, 2011 and 2010, respectively. The Company estimates its 2013

pension income will be approximately $20, based on current assumptions. The income in 2013 is a result of the expected return on plan assets more than

offsetting the lower expenses due to the announced plan freeze. Lower expenses are primarily due to a change in the amortization period resulting in lower

actuarial losses. To illustrate the impact of these assumptions on annual pension expense for 2013 and going forward, a 25 basis point decrease/increase in the

discount rate will increase/decrease pension expense by approximately $2 and a 25 basis point change in the long-term asset return assumption will

increase/decrease pension expense by approximately $11.

Also, in April 2012 changes to the Company's other postretirement medical, dental and life insurance coverage plans ("other postretirement plans") were

approved to no longer provide subsidized coverage for current employees who retire on or after January 1, 2014. The Company announced these changes in

April 2012.

Other postretirement plans (income) expense reflected in the Company's results was $(2), $10 and $15 in 2012, 2011 and 2010, respectively. The Company

estimates its 2013 other postretirement plans income will be approximately $9 based on the updated assumptions. The income in 2013 is a result of the

expected return on plan assets more than offsetting the lower expenses due to the announced plan freeze.

66