The Hartford 2012 Annual Report Download - page 44

Download and view the complete annual report

Please find page 44 of the 2012 The Hartford annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

|

|

Table of Contents

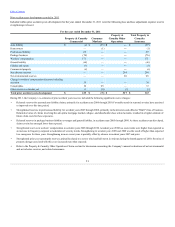

How reserves are set

Reserves are set by line of business within the various segments. A single line of business may be written in more than one segment. Case reserves are

established by a claims handler on each individual claim and are adjusted as new information becomes known during the course of handling the claim. Lines

of business for which loss data (e.g., paid losses and case reserves) emerge (i.e., is reported) over a long period of time are referred to as long-tail lines of

business. Lines of business for which loss data emerge more quickly are referred to as short-tail lines of business. The Company’s shortest-tail lines of

business are property and auto physical damage. The longest tail lines of business include workers’ compensation, general liability, professional liability and

assumed reinsurance. For short-tail lines of business, emergence of paid loss and case reserves is credible and likely indicative of ultimate losses. For long-tail

lines of business, emergence of paid losses and case reserves is less credible in the early periods and, accordingly, may not be indicative of ultimate losses.

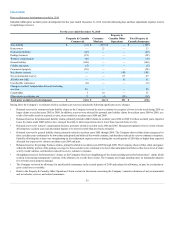

The Company’s reserving actuaries, who are independent of the business units, regularly review reserves for both current and prior accident years using the

most current claim data. For most lines of business, these reserve reviews incorporate a variety of actuarial methods and judgments and involve rigorous

analysis. These selections incorporate input, as judged by the reserving actuaries to be appropriate, from claims personnel, pricing actuaries and operating

management on reported loss cost trends and other factors that could affect the reserve estimates. Most reserves are reviewed fully each quarter, including loss

and loss adjustment expense reserves for property, auto physical damage, auto liability, package business, workers’ compensation, most general liability,

professional liability and fidelity and surety. Other reserves are reviewed semi-annually (twice per year) or annually. These include, but are not limited to,

reserves for losses incurred in accident years older than twelve and twenty years, for Consumer Markets and Property & Casualty Commercial, respectively,

assumed reinsurance, latent exposures, such as construction defects and unallocated loss adjustment expense. For reserves that are reviewed semi-annually or

annually, management monitors the emergence of paid and reported losses in the intervening quarters to either confirm that the estimate of ultimate losses

should not change or, if necessary, perform a reserve review to determine whether the reserve estimate should change.

An expected loss ratio is used in initially recording the reserves for both short-tail and long-tail lines of business. This expected loss ratio is determined through

a review of prior accident years’ loss ratios and expected changes to earned pricing, loss costs, mix of business, ceded reinsurance and other factors that are

expected to impact the loss ratio for the current accident year. For short-tail lines, IBNR for the current accident year is initially recorded as the product of the

expected loss ratio for the period, earned premium for the period and the proportion of losses expected to be reported in future calendar periods for the current

accident period. For long-tailed lines, IBNR reserves for the current accident year are initially recorded as the product of the expected loss ratio for the period

and the earned premium for the period, less reported losses for the period.

In addition to the expected loss ratio, the actuarial techniques or methods used primarily include paid and reported loss development and frequency / severity

techniques as well as the Bornhuetter-Ferguson method (a combination of the expected loss ratio and paid development or reported development method).

Within any one line of business, the methods that are given more influence vary based primarily on the maturity of the accident year, the mix of business and

the particular internal and external influences impacting the claims experience or the methods. The output of the reserve reviews are reserve estimates that are

referred to herein as the “actuarial indication”.

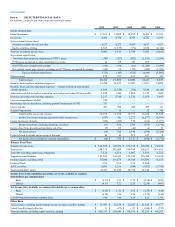

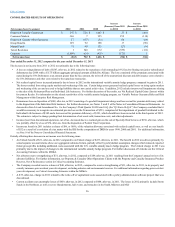

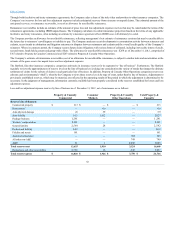

As of December 31, 2012 and 2011, net property and casualty insurance product reserves for losses and loss adjustment expenses reported under accounting

principles generally accepted in the United States of America (“U.S. GAAP”) were approximately equal to net reserves reported on a statutory basis. Under

U.S. GAAP, liabilities for unpaid losses for permanently disabled workers’ compensation claimants are discounted at rates that are no higher than risk-free

interest rates and which generally exceed the statutory discount rates set by regulators, such that workers’ compensation reserves for statutory reporting are

higher than the net reserves for U.S. GAAP reporting. Largely offsetting the effect of the difference in discounting is that a portion of the U.S. GAAP provision

for uncollectible reinsurance is not recognized under statutory accounting. Most of the Company’s property and casualty insurance product reserves are not

discounted. However, the Company has discounted liabilities funded through structured settlements and has discounted certain reserves for indemnity

payments due to permanently disabled claimants under workers’ compensation policies.

Provided below is a general discussion of which methods are preferred by line of business. Because the actuarial estimates are generated at a much finer level

of detail than line of business (e.g., by distribution channel, coverage, accident period), this description should not be assumed to apply to each coverage and

accident year within a line of business. Also, as circumstances change, the methods that are given more influence will change.

43