The Hartford 2012 Annual Report Download - page 179

Download and view the complete annual report

Please find page 179 of the 2012 The Hartford annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

169 -

170

170 -

171

171 -

172

172 -

173

173 -

174

174 -

175

175 -

176

176 -

177

177 -

178

178 -

179

179 -

180

180 -

181

181 -

182

182 -

183

183 -

184

184 -

185

185 -

186

186 -

187

187 -

188

188 -

189

189 -

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

|

|

Table of Contents

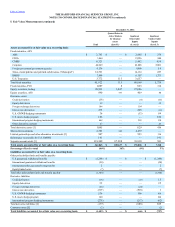

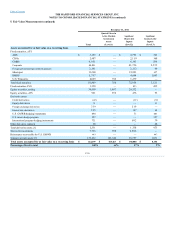

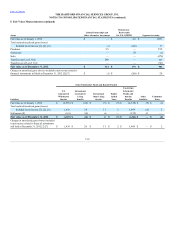

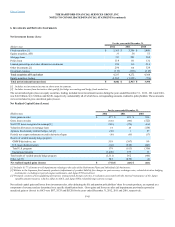

Separate Account Assets

Separate account assets are primarily invested in mutual funds. Other separate account assets include fixed maturities, limited partnerships, equity securities,

short-term investments and derivatives that are valued in the same manner, and using the same pricing sources and inputs, as those investments held by the

Company. Separate account assets classified as Level 3 primarily include limited partnerships in which fair value represents the separate account's share of

the fair value of the equity in the investment ("net asset value") and are classified in level 3 based on the Company's ability to redeem its investments.

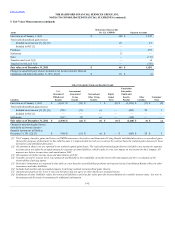

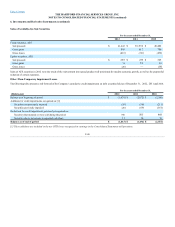

Living Benefits Required to be Fair Valued (in Other Policyholder Funds and Benefits Payable)

Living benefits required to be fair valued include U.S. GMWB, international GMWB and international other guaranteed living benefits.

Fair values for GMWB and guaranteed minimum accumulation benefit (“GMAB”) contracts are calculated using the income approach based upon internally developed models

because active, observable markets do not exist for those items. The fair value of the Company’s guaranteed benefit liabilities, classified as embedded derivatives, and the related

reinsurance and customized freestanding derivatives is calculated as an aggregation of the following components: Best Estimate Claim Payments; Credit Standing Adjustment; and

Margins. The resulting aggregation is reconciled or calibrated, if necessary, to market information that is, or may be, available to the Company, but may not be observable by

other market participants, including reinsurance discussions and transactions. The Company believes the aggregation of these components, as necessary and as reconciled or

calibrated to the market information available to the Company, results in an amount that the Company would be required to transfer or receive, for an asset, to or from market

participants in an active liquid market, if one existed, for those market participants to assume the risks associated with the guaranteed minimum benefits and the related

reinsurance and customized derivatives. The fair value is likely to materially diverge from the ultimate settlement of the liability as the Company believes settlement will be based on

our best estimate assumptions rather than those best estimate assumptions plus risk margins. In the absence of any transfer of the guaranteed benefit liability to a third party, the

release of risk margins is likely to be reflected as realized gains in future periods’ net income. Each component described below is unobservable in the marketplace and require

subjectivity by the Company in determining their value.

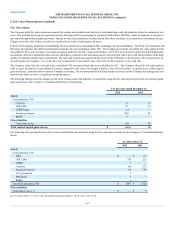

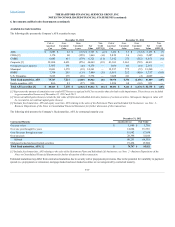

Oversight of the Company's valuation policies and processes for product and U.S. GMWB reinsurance derivatives is performed by a multidisciplinary group

comprised of finance, actuarial and risk management professionals. This multidisciplinary group reviews and approves changes and enhancements to the

Company's valuation model as well as associated controls.

Best Estimate

Claim Payments

The Best Estimate Claim Payments is calculated based on actuarial and capital market assumptions related to projected cash flows, including the present value of benefits and

related contract charges, over the lives of the contracts, incorporating expectations concerning policyholder behavior such as lapses, fund selection, resets and withdrawal

utilization. For the customized derivatives, policyholder behavior is prescribed in the derivative contract. Because of the dynamic and complex nature of these cash flows, best

estimate assumptions and a Monte Carlo stochastic process is used in valuation. The Monte Carlo stochastic process involves the generation of thousands of scenarios that assume

risk neutral returns consistent with swap rates and a blend of observable implied index volatility levels. Estimating these cash flows involves numerous estimates and subjective

judgments regarding a number of variables —including expected market rates of return, market volatility, correlations of market index returns to funds, fund performance,

discount rates and assumptions about policyholder behavior which emerge over time.

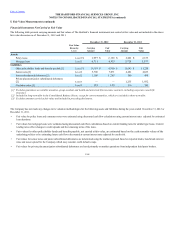

At each valuation date, the Company assumes expected returns based on:

•risk-free rates as represented by the euro dollar futures, LIBOR deposits and swap rates to derive forward curve rates;

•market implied volatility assumptions for each underlying index based primarily on a blend of observed market “implied volatility” data;

•correlations of historical returns across underlying well known market indices based on actual observed returns over the ten years preceding the valuation date; and

•three years of history for fund indexes compared to separate account fund regression.

On a daily basis, the Company updates capital market assumptions used in the GMWB liability model such as interest rates, equity indices and the blend of implied equity index

volatilities. The Company monitors various aspects of policyholder behavior and may modify certain of its assumptions, including living benefit lapses and withdrawal rates, if

credible emerging data indicates that changes are warranted. In addition, the Company will continue to evaluate policyholder behavior assumptions as we begin to

implement initiatives to reduce the size of the variable annuity business. At a minimum, all policyholder behavior assumptions are reviewed and updated, as appropriate,

in conjunction with the completion of the Company’s comprehensive study to refine its estimate of future gross profits during the third quarter of each year.

F-37