Shaw 2010 Annual Report Download - page 37

Download and view the complete annual report

Please find page 37 of the 2010 Shaw annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

|

|

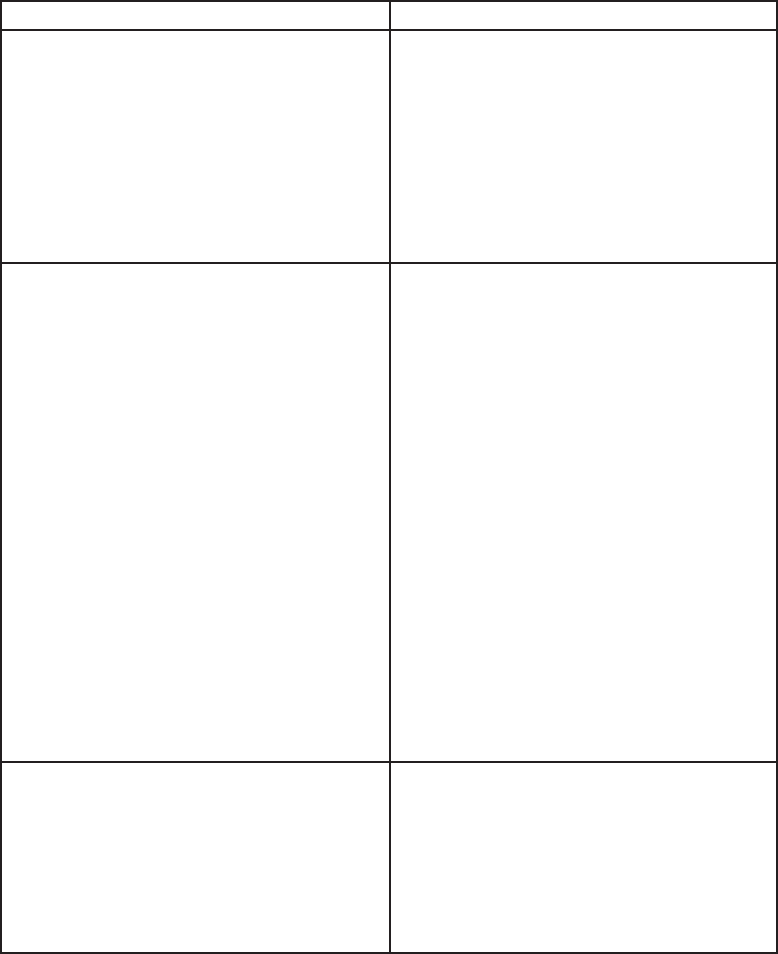

The following policies will be adopted in future years:

i) International Financial Reporting Standards (IFRS)

In February 2008, the CICA Accounting Standards Board (AScB) confirmed that Canadian publicly

accountable enterprises will be required to adopt International Financial Reporting Standards

(IFRS), as issued by the International Accounting Standards Board (IASB), for fiscal periods

beginning on or after January 1, 2011. These standards require the Company to begin reporting

under IFRS in the first quarter of fiscal 2012 with comparative data for the prior year. The table

below outlines the phases involved in the changeover to IFRS.

Phase Description and status

Impact assessment and planning This phase includes establishment of a project

team and high-level review to determine

potential significant differences under IFRS as

compared to Canadian GAAP. This phase has

been completed and as a result, the Company

has developed a transition plan and a preliminary

timeline to comply with the changeover date while

recognizing that project activities and timelines

may change as a result of unexpected

developments.

Design and development – key elements This phase includes (i) an in-depth review to

identify and assess accounting and reporting

differences, (ii) evaluation and selection of

accounting policies, (iii) assessment of impact

on information systems, internal controls, and

business activities, and (iv) training and

communication with key stakeholders.

During 2009, the Company completed its

preliminary identification and assessment of

accounting and reporting differences. In

addition, training was provided to certain key

employees involved in or directly impacted by

the conversion process.

During the current year, the assessment of the

impact on information systems and design phase

of system changes have been completed and the

implementation phase has commenced. The

Company has completed further in-depth

evaluations of those areas initially identified as

being potential accounting and reporting

differences, as well as the evaluation of IFRS 1

elections/exemptions which are discussed below.

Implementation This phase includes integration of solutions into

processes and financial systems that are required

for the conversion to IFRS and parallel reporting

during the year prior to transition including

proforma financial statements and note

disclosures. Process solutions will incorporate

required revisions to internal controls during the

changeover and on an on-going basis.

33

Shaw Communications Inc.

MANAGEMENT’S DISCUSSION AND ANALYSIS

August 31, 2010