Shaw 2010 Annual Report Download - page 114

Download and view the complete annual report

Please find page 114 of the 2010 Shaw annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

-

126

|

|

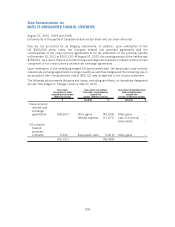

components of its US dollar denominated debt. The Company utilized cross-currency swaps, where

appropriate, to hedge its exposures on US dollar denominated debenture indebtedness. During the

year the Company redeemed all of its outstanding US dollar denominated debt.

In addition, some of the Company’s capital expenditures are incurred in US dollars, while its

revenue is primarily denominated in Canadian dollars. Decreases in the value of the Canadian dollar

relative to the US dollar could have an adverse effect on the Company’s cash flows. To mitigate some

of the uncertainty in respect to capital expenditures, the Company regularly enters into forward

contracts in respect of US dollar commitments. With respect to 2010, the Company entered into

forward contracts to purchase US $84,000 over a period of 12 months commencing in September

2009 at an average exchange rate of 1.1089 Cdn. In addition, the Company had in place long-term

forward contracts to purchase US $6,972 during 2010 at an average rate 1.4078. At August 31,

2010 the Company had forward contracts to purchase US $200,000 in October 2010 at an average

exchange rate of 1.0172 Cdn in respect of the closing of the Canwest acquisition.

Interest rate risk

Due to the capital-intensive nature of its operations, the Company utilizes long-term financing

extensively in its capital structure. The primary components of this structure are banking facilities

and various Canadian and US denominated senior notes and debentures with varying maturities

issued in the public markets as more fully described in note 9.

Interest on the Company’s banking facilities is based on floating rates, while the senior notes and

debentures are fixed-rate obligations. The Company utilizes its credit facility to finance day-to-day

operations and, depending on market conditions, periodically converts the bank loans to fixed-rate

instruments through public market debt issues. As at August 31, 2010, 100% of the Company’s

consolidated long-term debt was fixed with respect to interest rates.

Market risk

Net income and other comprehensive income for 2010 could have varied if the Canadian dollar to

US dollar foreign exchange rates or market interest rates varied by reasonably possible amounts.

The sensitivity to currency risk has been determined based on a hypothetical change in Canadian

dollar to US dollar foreign exchange rates of 10%. The financial instruments impacted by this

hypothetical change include foreign exchange forward contracts and cross-currency interest rate

exchange agreements and would have changed net income by $3,759 net of tax (2009 – $nil) and

other comprehensive income by $18,378 net of tax (2009 – $17,092). A portion of the Company’s

accounts receivables and accounts payable and accrued liabilities is denominated in US dollars;

however, due to their short-term nature, there is no significant market risk arising from fluctuations

in foreign exchange rates.

The sensitivity to interest rate risk has been determined based on a hypothetical change of one

percentage or 100 basis points. The financial instruments impacted by this hypothetical change

include foreign exchange forward contracts and cross-currency interest rate exchange agreements

and would have changed net income by $200 net of tax (2009 – $nil) and other comprehensive

income by $51 net of tax (2009 – $5,691). Interest on the Company’s banking facilities is based on

floating rates and there is no significant market risk arising from fluctuations in interest rates.

110

Shaw Communications Inc.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

August 31, 2010, 2009 and 2008

[all amounts in thousands of Canadian dollars except share and per share amounts]