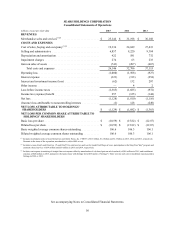

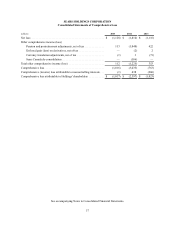

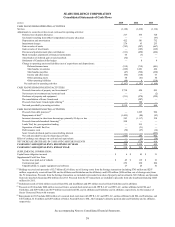

Sears 2015 Annual Report Download - page 65

Download and view the complete annual report

Please find page 65 of the 2015 Sears annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

|

|

factors could have a significant impact on the recoverability of these assets and could have a material impact on our

consolidated financial statements.

Goodwill Impairment Assessments

Our goodwill balance relates to our Home Services business. The goodwill impairment test involves a two-

step process. The first step is a comparison of the reporting unit's fair value to its carrying value. We estimate fair

value using the best information available, using a discounted cash flow model, commonly referred to as the income

approach. The income approach uses the reporting unit's projection of estimated operating results and cash flows

that is discounted using a weighted-average cost of capital that reflects current market conditions appropriate for the

reporting unit. The projection uses management's best estimates of economic and market conditions over the

projected period, including growth rates in sales, costs, estimates of future expected changes in operating margins

and cash expenditures. Other significant estimates and assumptions include terminal value growth rates, future

estimates of capital expenditures and changes in future working capital requirements. We were unable to use a

market approach due to there being no market comparables.

If the carrying value of the reporting unit is higher than its fair value, there is an indication that impairment

may exist and the second step must be performed to measure the amount of impairment loss, if any. The amount of

impairment is determined by comparing the implied fair value of reporting unit goodwill to the carrying value of the

goodwill in the same manner as if the reporting unit was being acquired in a business combination. See Note 12 for

further information.

Intangible Asset Impairment Assessments

We consider the income approach when testing intangible assets with indefinite lives for impairment on an

annual basis. We utilize the income approach, specifically the relief from royalty method, for analyzing our

indefinite-lived assets. This method is based on the assumption that, in lieu of ownership, a firm would be willing to

pay a royalty in order to exploit the related benefits of this asset class. The relief from royalty method involves two

steps: (1)€estimation of reasonable royalty rates for the assets and (2)€the application of these royalty rates to a net

sales stream and discounting the resulting cash flows to determine a value. We multiplied the selected royalty rate by

the forecasted net sales stream to calculate the cost savings (relief from royalty payment) associated with the assets.

The cash flows are then discounted to present value by the selected discount rate and compared to the carrying value

of the assets.

In our quarterly reports on Form 10-Q filed during 2015, the Company disclosed that if its results continued to

decline it could result in revisions in management's estimates of the fair value of the Company's trade names and

may result in impairment charges. As a result of continued declines in revenue experienced in the fourth quarter at

Sears Domestic, our analysis indicated that the fair value of the Sears trade name was less than its carrying value.

Accordingly, we recorded impairment related to the Sears trade name of $180 million, which reduced the carrying

value to $812 million. See Note 12 for further information.

Fair Value of Financial Instruments

We determine the fair value of financial instruments in accordance with standards pertaining to fair value

measurements. Such standards define fair value and establish a framework for measuring fair value in GAAP. Under

fair value measurement accounting standards, fair value is considered to be the exchange price in an orderly

transaction between market participants to sell an asset or transfer a liability at the measurement date. We report the

fair value of financial assets and liabilities based on the fair value hierarchy prescribed by accounting standards for

fair value measurements, which prioritizes the inputs to valuation techniques used to measure fair value into three

levels.

Financial instruments that potentially subject the Company to concentration of credit risk consist principally of

temporary cash investments, accounts receivable. We place our cash and cash equivalents in investment-grade,

short-term instruments with high quality financial institutions and, by policy, limit the amount of credit exposure in

any one financial instrument.

SEARS HOLDINGS CORPORATION

Notes to Consolidated Financial Statements—(Continued)

65