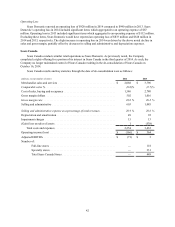

Sears 2015 Annual Report Download - page 52

Download and view the complete annual report

Please find page 52 of the 2015 Sears annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

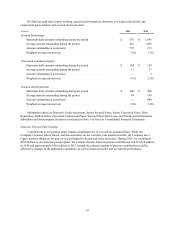

|

|

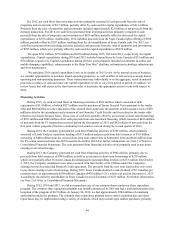

flows, or the estimated fair value of the reporting unit's tangible and intangible assets and liabilities, could

significantly increase or decrease the estimated fair value of the reporting unit or its net assets. At the 2015 annual

impairment test date, the conclusion that no indication of goodwill impairment existed for the reporting unit would

not have changed had the test been conducted assuming: (1)€a 100€basis point increase in the discount rate used to

discount the aggregate estimated cash flows of the reporting unit to its net present value in determining their

estimated fair values and/or (2)€a 100 basis point decrease in the estimated sales growth rate and/or terminal period

growth rate.

Based on our sensitivity analysis, we do not believe that the remaining recorded goodwill balance is at risk of

impairment at the reporting unit at the end of the year because the fair value is in excess of the carrying value and

not at risk of failing step one. However, goodwill impairment charges may be recognized in future periods in the

reporting unit to the extent changes in factors or circumstances occur, including deterioration in the macroeconomic

environment, retail industry or in the equity markets, which includes the market value of our common shares,

deterioration in our performance or our future projections, or changes in our plans for the reporting unit.

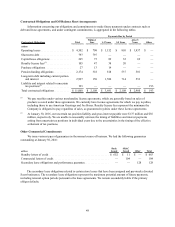

Intangible Asset Impairment Assessments

The majority of our indefinite-lived intangible assets relate to the Sears, Kenmore®, Craftsman® and DieHard®

trade names. In 2015, we recorded impairment related to the Sears trade name of $180 million, which reduced the

carrying value to $812 million. We did not record any intangible asset impairment charges in 2014 or 2013.

The use of different assumptions, estimates or judgments in our intangible asset impairment testing process,

such as the estimated future cash flows of assets and the discount rate used to discount such cash flows, could

significantly increase or decrease the estimated fair value of an asset, and therefore, impact the related impairment

charge. At the 2015 annual impairment test date, the above-noted conclusion that no indication of intangible asset

impairment existed at the test date for the Kenmore®, Craftsman® and DieHard® trade names would have changed

had the test been conducted assuming: (1)€a 100€basis point increase in the discount rate used to discount the

aggregate estimated cash flows of our assets to their net present value in determining their estimated fair values

(without any change in the aggregate estimated cash flows of our intangibles), (2)€a 100 basis point decrease in the

terminal period growth rate, (3) a 1,000 basis point decrease in the revenue growth rate for fiscal year 2016, or (4) a

10 basis point decrease in the royalty rate applied to the forecasted net sales stream of our assets and would have

resulted in a potential impairment of up to $157 million under any combination of those scenarios. Also, the above-

noted impairment related to the Sears trade name would have changed under any combination of those scenarios and

would have resulted in potential incremental impairment of up to $200 million.

We believe the impairment charge of $180 million is appropriate based on the judgments and estimates used in

our analysis. We do not believe that the other indefinite-lived intangible balances are impaired at the end of the year

because the fair values are in excess of the carrying values based on our analysis. However, further indefinite-lived

intangible impairment charges may be recognized in future periods to the extent changes in factors or circumstances

occur, including deterioration in the macroeconomic environment, retail industry, deterioration in our performance

or our future projections, if actual results are not consistent with our estimates and assumptions used in the analysis,

or changes in our plans for one or more indefinite-lived intangible asset. We will continue to monitor for such

changes in facts or circumstances, which may be indicators of potential impairment triggers, and may result in

impairment charges in the future, which could be material to our results of operations.

Impairment of Long-Lived Assets

In accordance with accounting standards governing the impairment or disposal of long-lived assets, the

carrying value of long-lived assets, including property and equipment and definite-lived intangible assets, is

evaluated whenever events or changes in circumstances indicate that a potential impairment has occurred relative to

a given asset or assets. Our accounting policies related to long-lived asset impairment assessments are further

described in Note 1 of Notes to Consolidated Financial Statements. As a result of this impairment testing, the

Company recorded impairment charges of $94 million, $34 million and $220 million during 2015, 2014 and 2013,

respectively. Our impairment testing includes uncertainty because it requires management to make assumptions and

to apply judgment to estimate future cash flows and asset fair values. If actual results are not consistent with our

52