Sears 2015 Annual Report Download - page 49

Download and view the complete annual report

Please find page 49 of the 2015 Sears annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

|

|

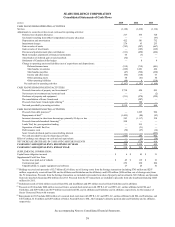

Application of Critical Accounting Policies and Estimates

In preparing the financial statements, certain accounting policies require considerable judgment to select the

appropriate assumptions to calculate financial estimates. These estimates are complex and subject to an inherent

degree of uncertainty. We base our estimates on historical experience, terms of existing contracts, evaluation of

trends and other assumptions that we believe to be reasonable under the circumstances. We continually evaluate the

information used to make these estimates as our business and the economic environment change. Although the use

of estimates is pervasive throughout the financial statements, we consider an accounting estimate to be critical if:

• it requires assumptions to be made about matters that were highly uncertain at the time the estimate was

made, and

• changes in the estimate that are reasonably likely to occur from period to period or different estimates

that could have been selected would have a material effect on our financial condition, cash flows or

results of operations.

Management believes the current assumptions and other considerations used to estimate amounts reflected in

the financial statements are appropriate. However, if actual experience differs from the assumptions and the

considerations used in estimating amounts, the resulting changes could have a material adverse effect on our

consolidated results of operations, and in certain situations, could have a material adverse effect on our financial

condition.

Management has discussed the development and selection of these critical accounting estimates with the Audit

Committee of our Board of Directors and the Audit Committee has reviewed the disclosure presented below relating

to the selection of these estimates.

The following is a summary of our most critical policies and estimates. See Note 1 of Notes to Consolidated

Financial Statements for a listing of our other significant accounting policies.

Valuation of Inventory

Our inventory is valued at the lower of cost or market determined primarily using the retail inventory method

("RIM"). RIM is an averaging method that is commonly used in the retail industry. To determine inventory cost

under RIM, inventory at its retail selling value is segregated into groupings of merchandise having similar

characteristics, which are then converted to a cost basis by applying specific average cost factors for each grouping

of merchandise. Cost factors represent the average cost-to-retail ratio for each merchandise group based upon the

year purchasing activity for each store location. Accordingly, a significant assumption under the retail method is that

inventory in each group is similar in terms of its cost-to-retail relationship and has similar turnover rates.

Management monitors the content of merchandise in these groupings to prevent distortions that would have a

material effect on inventory valuation.

RIM inherently requires management judgment and certain estimates that may significantly affect the ending

inventory valuation, as well as gross margin. Among others, two significant estimates used in inventory valuation

are the level and timing of permanent markdowns (clearance markdowns used to clear unproductive or slow-moving

inventory) and shrinkage. Amounts are charged to cost of sales, buying and occupancy at the time the retail value of

inventory is reduced through the use of permanent markdowns.

Factors considered in the determination of permanent markdowns include current and anticipated demand,

customer preferences, age of the merchandise, fashion trends and weather conditions. In addition, inventory is also

evaluated against corporate pre-determined historical markdown cadences. When a decision is made to permanently

markdown merchandise, the resulting gross margin reduction is recognized in the period the markdown is recorded.

The timing of the decision, particularly surrounding the balance sheet date, can have a significant effect on the

results of operations.

Shrinkage is estimated as a percentage of sales for the period from the date of the last physical inventory to the

end of the year. Physical inventories are taken annually for all stores and inventory records are adjusted accordingly.

The shrinkage rate from the most recent physical inventory, in combination with historical experience, is used as the

basis for the shrinkage accrual following the physical inventory.

49