Sears 2014 Annual Report Download - page 77

Download and view the complete annual report

Please find page 77 of the 2014 Sears annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

|

|

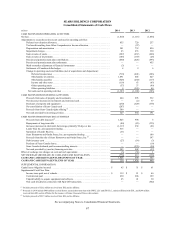

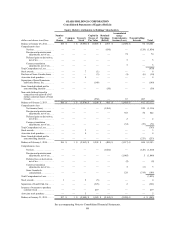

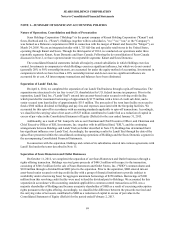

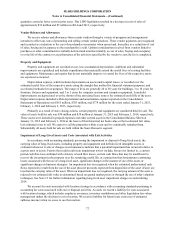

SEARS HOLDINGS CORPORATION

Notes to Consolidated Financial Statements—(Continued)

77

Income tax expense or benefit from continuing operations is generally determined without regard to other

categories of earnings, such as discontinued operations and other comprehensive income ("OCI"). An exception is

provided in the authoritative accounting guidance when there is income from categories other than continuing

operations and a loss from continuing operations in the current year. In this case, the tax benefit allocated to

continuing operations is the amount by which the loss from continuing operations reduces the tax expense recorded

with respect to the other categories of earnings, even when a valuation allowance has been established against the

deferred tax assets. In instances where a valuation allowance is established against current year losses, income from

other sources, including gain from pension and other postretirement benefits recorded as a component of OCI or the

creation of a deferred tax liability through additional paid-in capital for the book to tax difference for the original

issue discount relating to the $625 million 8% senior unsecured notes due 2019, is considered when determining

whether sufficient future taxable income exists to realize the deferred tax assets.

Stock-based Compensation

We account for stock-based compensation arrangements in accordance with accounting standards pertaining to

share-based payment transactions, which requires us to both recognize as expense the fair value of all stock-based

compensation awards (which includes stock options, although there were no options outstanding in 2014) and to

classify excess tax benefits associated with share-based compensation deductions as cash from financing activities

rather than cash from operating activities. We recognize compensation expense as awards vest on a straight-line

basis over the requisite service period of the award.

Earnings Per Common Share

Basic earnings per common share is calculated by dividing net income attributable to Holdings' shareholders

by the weighted average number of common shares outstanding for each period. Diluted earnings per common share

also includes the dilutive effect of potential common shares, exercise of stock options, warrants and the effect of

restricted stock when dilutive.

New Accounting Pronouncements

Consolidation

In February 2015, the Financial Accounting Standards Board ("FASB") issued an accounting standards update

which revises the consolidation model. Specifically, the amendments modify the evaluation of whether limited

partnerships and similar legal entities are variable interest entities (VIEs) or voting interest entities, eliminate the

presumption that a general partner should consolidate a limited partnership, affect the consolidation analysis of

reporting entities that are involved with VIEs, particularly those that have fee arrangements and related party

relationships, and provide a scope exception from consolidation guidance for reporting entities with interests in legal

entities that are required to comply with or operate in accordance with requirements that are similar to those in Rule

2a-7 of the Investment Company Act of 1940 for registered money market funds. This update will be effective for

the Company in the first quarter of 2015. The adoption of the new standard is not expected to have a material impact

on the Company’s consolidated financial position, results of operations, cash flows or disclosures.

Extraordinary and Unusual Items

In January 2015, the FASB issued an accounting standards update which eliminates the concept of an

extraordinary item. Extraordinary items are events and transactions that are distinguished by their unusual nature

and by the infrequency of their occurrence. Eliminating the extraordinary classification simplifies income statement

presentation by altogether removing the concept of extraordinary items from consideration. This update will be

effective for the Company in the first quarter of 2015. The adoption of the new standard is not expected to have a

material impact on the Company’s consolidated financial position, results of operations, cash flows or disclosures.