Sears 2013 Annual Report Download - page 61

Download and view the complete annual report

Please find page 61 of the 2013 Sears annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

|

|

61

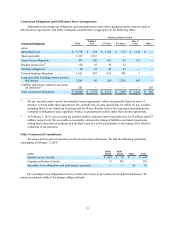

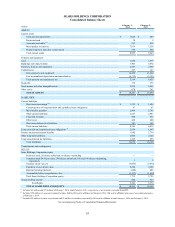

Item 7A. Quantitative and Qualitative Disclosures about Market Risk

We face market risk exposure in the form of interest rate risk and foreign currency risk. These market risks arise

from our derivative financial instruments and debt obligations.

Interest Rate Risk

We manage interest rate risk through the use of fixed and variable-rate funding. All debt securities are

considered non-trading. At February 1, 2014, 55% of our debt portfolio was variable rate. Based on the size of this

variable rate debt portfolio at February 1, 2014, which totaled approximately $2.3 billion, an immediate 100 basis

point change in interest rates would have affected annual pretax funding costs by $23 million. These estimates do

not take into account the effect on income resulting from invested cash or the returns on assets being funded. These

estimates also assume that the variable rate funding portfolio remains constant for an annual period and that the

interest rate change occurs at the beginning of the period.

Foreign Currency Risk

At February 1, 2014, we had a foreign currency forward contract outstanding, totaling $43 million Canadian

notional value and with a remaining life of 0.1 years, designed to hedge our net investment in Sears Canada against

adverse changes in exchange rates. The aggregate fair value of the forward contract at February 1, 2014 was $2

million. A hypothetical 1% adverse movement in the level of the Canadian exchange rate relative to the U.S. dollar

at February 1, 2014, with all other variables held constant, would have resulted in a fair value of this contract of

approximately $1 million at February 1, 2014, a decrease of $1 million. Certain of our currency forward contracts

require collateral be posted in the event our liability under such contracts reaches a predetermined threshold. Cash

collateral posted under these contracts is recorded as part of our accounts receivable balance. We had no cash

collateral posted under our contracts at February 1, 2014.

Sears Canada reduces its foreign exchange risk with respect to U.S. dollar denominated assets and liabilities and

purchases of goods or services by entering into foreign exchange forward contracts. At February 1, 2014, these

contracts had a notional value of $90 million. The fair value of the forward contracts at February 1, 2014 was

approximately $6 million. A hypothetical 1% adverse movement in the level of the Canadian exchange rate relative

to the U.S. dollar at February 1, 2014, with all other variables held constant, would have resulted in a fair value for

these contracts of approximately $5 million at February 1, 2014, a decrease of $1 million.

Counterparty Credit Risk

We actively manage the risk of nonpayment by our derivative counterparties by limiting our exposure to

individual counterparties based on credit ratings, value at risk and maturities. The counterparties to these instruments

are major financial institutions with investment grade credit ratings or better at February 1, 2014. We had no

derivative instruments at February 2, 2013.