Sears 2013 Annual Report Download - page 28

Download and view the complete annual report

Please find page 28 of the 2013 Sears annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

|

|

28

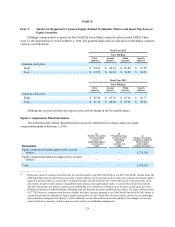

These other significant items included in Adjusted EBITDA are further explained as follows:

• Impairment charges – Accounting standards require the Company to evaluate the carrying value of fixed

assets, goodwill and intangible assets for impairment. As a result of the Company’s analysis, we have

recorded impairment charges related to certain fixed asset and goodwill balances.

• Pension settlements – The Company amended its domestic pension plan and offered a one-time voluntary

lump sum payment option in an effort to reduce its long-term pension obligations and ongoing annual

pension expense. The pension settlements were funded from existing pension plan assets. In connection

with this transaction, the Company incurred a charge to operations as a result of the requirement to expense

the unrealized actuarial losses. The charge had no effect on equity because the unrealized actuarial losses

are already recognized in accumulated other comprehensive income/(loss). Accordingly, the effect on

retained earnings was offset by a corresponding reduction in accumulated other comprehensive loss.

• Closed store reserve and severance – We are transforming our Company to a less asset-intensive business

model. Throughout this transformation, we continue to make choices related to our stores, which could

result in sales, closures, lease terminations or a variety of other decisions.

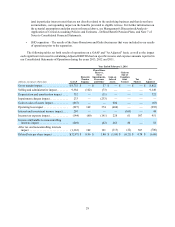

• Domestic pension expense – Contributions to our pension plans remain a significant use of our cash on an

annual basis. Cash contributions to our pension and postretirement plans are separately disclosed on the

cash flow statement. While the Company's pension plan is frozen, and thus associates do not currently earn

pension benefits, we have a legacy pension obligation for past service performed by Kmart and Sears

associates. The annual pension expense included in our statement of operations related to these legacy

domestic pension plans was relatively minimal in years prior to 2009. However, due to the severe decline in

the capital markets that occurred in the latter part of 2008, our domestic pension expense was $162 million

in 2013, $165 million in 2012 and $74 million in 2011. Pension expense is comprised of interest cost,

expected return on plan assets and amortization of experience losses. This adjustment eliminates the entire

pension expense from the statement of operations to improve comparability. Pension expense is included in

the determination of Net Income. The components of the adjustments to EBITDA related to domestic

pension expense were as follows:

millions 2013 2012 2011

Components of net periodic expense:

Interest cost. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $ 219 $ 291 $ 313

Expected return on plan assets . . . . . . . . . . . . . . . . . . . . . . . . . . . . (224)(291)(302)

Amortization of experience losses . . . . . . . . . . . . . . . . . . . . . . . . . 167 165 63

Net periodic expense. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $ 162 $ 165 $ 74

In accordance with U.S. GAAP, we recognize on the balance sheet actuarial gains and losses for

defined benefit pension plans annually in the fourth quarter of each fiscal year and whenever a plan is

determined to qualify for a remeasurement during a fiscal year. For income statement purposes, these

actuarial gains and losses are recognized throughout the year through an amortization process. The

Company recognizes in its results of operations, as a corridor adjustment, any unrecognized actuarial net

gains or losses that exceed 10% of the larger of projected benefit obligations or plan assets. Accumulated

gains/losses that are inside the 10% corridor are not recognized, while accumulated actuarial gains/losses

that are outside the 10% corridor are amortized over the "average future service" of the population and are

included in the amortization of experience losses line item above.

Actuarial gains and losses occur when actual experience differs from the estimates used to allocate

the change in value of pension plans to expense throughout the year or when assumptions change, as they

may each year. Significant factors that can contribute to the recognition of actuarial gains and losses

include changes in discount rates used to remeasure pension obligations on an annual basis or upon a

qualifying remeasurement, differences between actual and expected returns on plan assets and other

changes in actuarial assumptions. Management believes these actuarial gains and losses are primarily

financing activities that are more reflective of changes in current conditions in global financial markets