Sears 2013 Annual Report Download - page 56

Download and view the complete annual report

Please find page 56 of the 2013 Sears annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

|

|

56

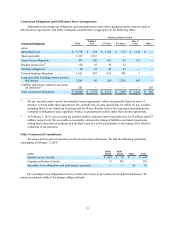

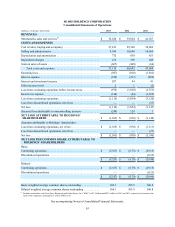

For purposes of determining the periodic expense of our defined benefit plan, we use the fair value of plan

assets as the market related value. A one-percentage-point change in the assumed discount rate would have the

following effects on the pension liability:

millions 1 percentage-point

Increase 1 percentage-point

Decrease

Effect on interest cost component . . . . . . . . . . . . . . . . . . . . . . . . . . . $ 28 $ (36)

Effect on pension benefit obligation . . . . . . . . . . . . . . . . . . . . . . . . . $ (596) $ 713

For 2014 and beyond, the domestic weighted-average health care cost trend rates used in measuring the

postretirement benefit expense are a 8.0% trend rate in 2014 to an ultimate trend rate of 6.0% in 2018. A one-

percentage-point change in the assumed health care cost trend rate would have the following effects on the

postretirement liability:

millions 1 percentage-point

Increase 1 percentage-point

Decrease

Effect on total service and interest cost components. . . . . . . . . . . . . $ 1 $ (1)

Effect on postretirement benefit obligation . . . . . . . . . . . . . . . . . . . . $ 17 $ (15)

Income Taxes

We account for income taxes according to accounting standards for such taxes. Deferred tax assets and

liabilities are recognized for the future tax consequences attributable to differences between the book basis and tax

basis of assets and liabilities. Deferred tax assets and liabilities are measured using enacted tax rates expected to

apply to taxable income in the years in which those temporary differences are expected to be recovered or settled. If

future utilization of deferred tax assets is uncertain, the Company may record a valuation allowance against certain

deferred tax assets. In evaluating our ability to recover our deferred tax assets within the jurisdiction from which

they arise, we consider all available positive and negative evidence, including scheduled reversals of deferred tax

liabilities, projected future taxable income, tax planning strategies, and results of recent operations. In projecting

future taxable income, we begin with historical results adjusted for the results of discontinued operations and

changes in accounting policies and incorporate assumptions including the amount of future state, federal and foreign

pre-tax operating income, the reversal of temporary differences, and the implementation of feasible and prudent tax

planning strategies. In evaluating the objective evidence that historical results provide, we consider cumulative

operating income (loss) over the past several years. These assumptions require significant judgment about the

forecasts of future taxable income. After consideration of evidence regarding the ability to realize our deferred tax

assets, we established a valuation allowance against certain deferred income tax assets in 2013, 2012 and 2011. In

2013, the Company increased its valuation allowance by $623 million. Included in this $623 million valuation

allowance increase was $138 million for state separate entity deferred tax assets as Kmart Corporation incurred a

three-year cumulative loss in 2013. The Company continues to monitor its operating performance and evaluate the

likelihood of the future realization of these deferred tax assets.

Income tax expense or benefit from continuing operations is generally determined without regard to other

categories of earnings, such as discontinued operations and other comprehensive income ("OCI"). An exception is

provided in the authoritative accounting guidance when there is income from categories other than continuing

operations and a loss from continuing operations in the current year. In this case, the tax benefit allocated to

continuing operations is the amount by which the loss from continuing operations reduces the tax expense recorded

with respect to the other categories of earnings, even when a valuation allowance has been established against the

deferred tax assets. In instances where a valuation allowance is established against current year losses, income from

other sources, including gain from pension and other postretirement benefits recorded as a component of OCI, is

considered when determining whether sufficient future taxable income exists to realize the deferred tax assets. As a

result, for the year ended February 1, 2014, the Company recorded a tax expense of $97 million in OCI related to the

gain on pension and other postretirement benefits, and recorded a corresponding tax benefit of $97 million in

continuing operations.