Sara Lee 2011 Annual Report Download - page 91

Download and view the complete annual report

Please find page 91 of the 2011 Sara Lee annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

|

|

Variable Interest Entities The corporation consolidates variable

interest entities (“VIEs”) of which it is the primary beneficiary. Legal

entities with which the corporation becomes involved are assessed

to determine whether such entities are VIEs and, if so, whether or

not the corporation is the primary beneficiary. In general, the corpora-

tion determines whether it is the primary beneficiary of a VIE through

a qualitative analysis of risk, which identifies which variable interest

holder absorbs the majority of the financial risk or rewards and vari-

ability of the VIE. In performing this analysis, we consider all relevant

facts and circumstances, including: the design and activities of the

VIE, terms of VIE contracts, identification of other variable interest

holders, our explicit arrangements and our implicit variable interests.

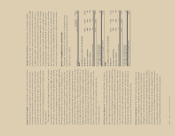

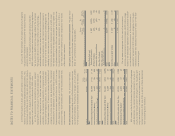

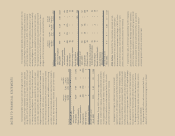

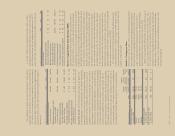

Note 3 – Intangible Assets and Goodwill

The primary components of the corporation’s intangible assets

reported in continuing operations and the related amortization

expense are as follows:

Accumulated Net Book

In millions Gross Amortization Value

2011

Intangible assets subject to amortization

Trademarks $231 $104 $127

Customer relationships 142 106 36

Computer software 411 313 98

Other contractual agreements 1055

$794 $528 $266

Trademarks and brand names

not subject to amortization 56

Net book value of intangible assets $322

2010

Intangible assets subject to amortization

Trademarks $160 $÷81 $÷79

Customer relationships 100 87 13

Computer software 352 258 94

Other contractual agreements 541

$617 $430 187

Trademarks and brand names

not subject to amortization 54

Net book value of intangible assets $241

Financial Instruments The corporation uses financial instruments,

including forward exchange, options, futures and swap contracts,

to manage its exposures to movements in interest rates, foreign

exchange rates and commodity prices. The use of these financial

instruments modifies the exposure of these risks with the intent

to reduce the risk or cost to the corporation. The corporation does

not use derivatives for trading purposes and is not a party to lever-

aged derivatives.

The corporation uses either hedge accounting or mark-to-market

accounting for its derivative instruments. Under hedge accounting,

the corporation formally documents its hedge relationships, including

identification of the hedging instruments and the hedged items, as

well as its risk management objectives and strategies for undertaking

the hedge transaction. This process includes linking derivatives

that are designated as hedges of specific assets, liabilities, firm

commitments or forecasted transactions. The corporation also for-

mally assesses, both at inception and at least quarterly thereafter,

whether the derivatives that are used in hedging transactions are

highly effective in offsetting changes in either the fair value or cash

flows of the hedged item. If it is determined that a derivative ceases

to be a highly effective hedge, or if the anticipated transaction is no

longer likely to occur, the corporation discontinues hedge accounting

and any deferred gains or losses are recorded in the “Selling, general

and administrative expenses” line in the Consolidated Statements

of Income. Derivatives are recorded in the Consolidated Balance

Sheets at fair value in other assets and other liabilities. For more

information about accounting for derivatives see Note 15,

“Financial Instruments.”

Self-Insurance Reserves The corporation purchases third-party

insurance for workers’ compensation, automobile and product and

general liability claims that exceed a certain level. The corporation

is responsible for the payment of claims under these insured limits.

The undiscounted obligation associated with these claims is accrued

based on estimates obtained from consulting actuaries. Historical

loss development factors are utilized to project the future develop-

ment of incurred losses, and these amounts are adjusted based

upon actual claim experience and settlements. Accrued reserves,

excluding any amounts covered by insurance, were $86 million as

of July 2, 2011 and $76 million as of July 3, 2010.

Business Acquisitions With respect to business acquisitions, the

corporation is required to recognize and measure the identifiable

assets acquired, liabilities assumed, contractual contingencies,

contingent consideration and any noncontrolling interest in an

acquired business at fair value on the acquisition date. In addition,

the accounting guidance also requires expensing acquisition costs

when incurred, restructuring costs in periods subsequent to the

acquisition date, and any adjustments to deferred tax asset valua-

tion allowances and acquired uncertain tax positions after the

measurement period to be reflected in income tax expense.

88/89 Sara Lee Corporation and Subsidiaries